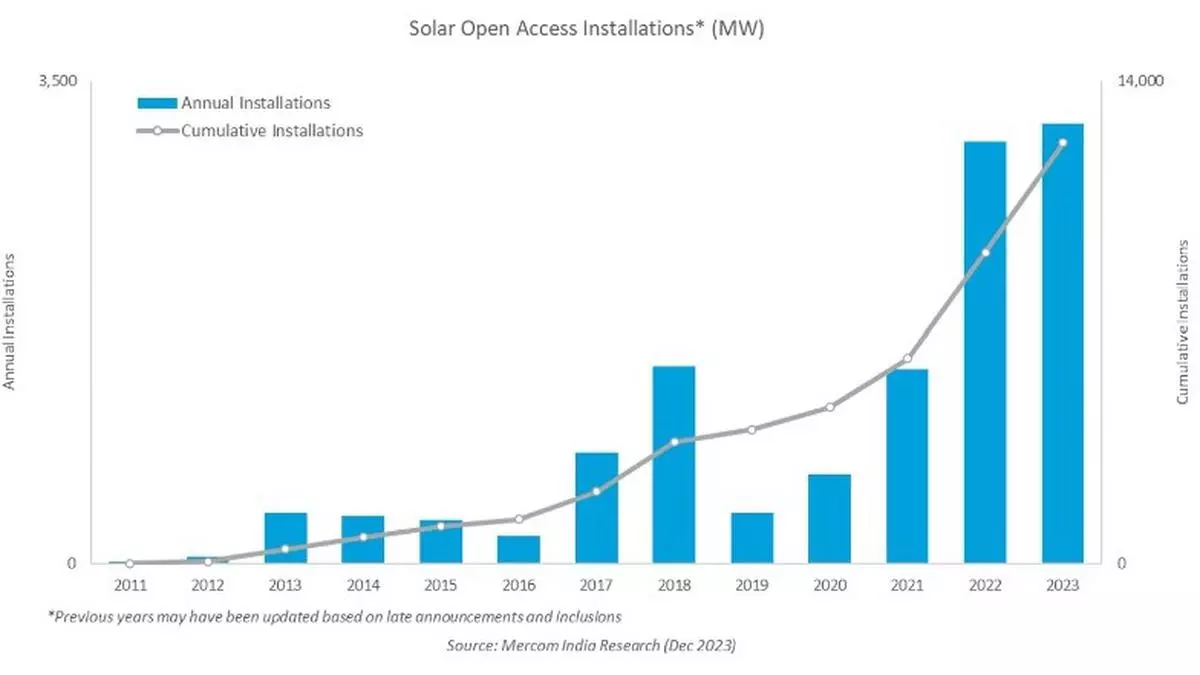

The calendar year 2023 saw the Indian solar open market sustain its growth as the segment added India added a record 3.2 GW of capacity, an increase of about 6 per cent over the 2022 capacity addition of 3 GW.

The 3.2 GW addition was the highest open-access solar capacity addition in a calendar year. Karnataka led all states, contributing 27.9 per cent of new open-access solar capacity in 2023.

Cumulative installed solar capacity in the open access segment stood at 12.2 GW as of December 2023.

Karnataka remained the leader in cumulative installations, accounting for 33.1 per cent of the country’s installations, followed by Maharashtra (13.5 per cent) and Tamil Nadu (11.4 per cent). The top five states contributed 72.2 per cent to the country’s cumulative open-access solar installations as of December 2023.

The extension of the Approved List of Models and Manufacturers (ALMM) order until March 2024 and falling module prices drove commercial and industrial (C&I) consumers to commission pending projects and sign new PPAs. Factors such as declining system costs, favourable policies and the green energy open access Rules in several states fueled solar installations through the open access market in 2023.

“Open access solar is one of the bright spots in India’s solar market, attracting commercial enterprises and industrial units to shift towards solar and other clean energy sources. The potential cost savings for businesses are hard to ignore, especially as solar costs continue to decrease while retail electricity prices rise,” said Raj Prabhu, CEO of Mercom Capital Group.

India added 831.2 MW of open access solar in Q4 2023, down about 23 per cent quarter-over-quarter basis, but up 6.2 per cent year-over-year when compared with 782.5 MW in Q4 2022.

In the December 2023 quarter, Tamil Nadu led all states, accounting for one-fourth (24.8 per cent) of total open-access solar installations. Rajasthan ranked second and Karnataka third with 23.3 per cent and 15.8 per cent share of total capacity additions in Q4, respectively. The top five states accounted for 83.6 per cent of solar open-access installations in Q4 2023.

While lower PPA prices resulted in higher capacity additions y-o-y, installations dropped q-o-q as several developers completed their projects in Q3 and signed new PPAs in Q4, which are expected to increase capacity additions in the upcoming quarters.

India had 13.9 GW of projects under development and in the pre-construction phase at the end of Q4 2023. With a strong pipeline, the outlook is very promising for this market segment and this segment is expected to sustain strong growth in this calendar year.

Also read: Gujarat to buy solar power from NLC at ₹2.70 a kWhr

“Other than the larger conglomerates and international brands with a presence in India, the domestic industries are also seriously considering green energy open access. Sustainability initiatives across sectors have been adding to the demand for green power in a larger scale,” pointed out Priya Sanjay, Managing Director at Mercom India.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.