The general insurance industry has ended the fiscal FY24 with 13 per cent growth. But, FY24 growth is lower than when compared with 16 per cent achieved in the previous year.

However, the industry has maintained its double-digit growth trend over the last few years.

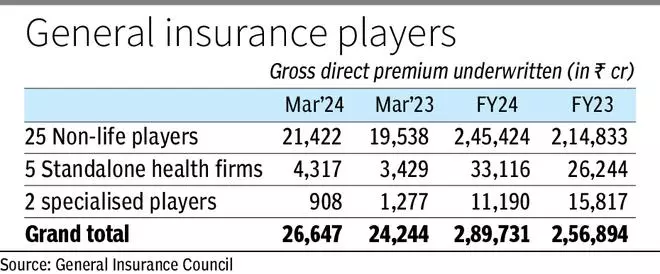

The gross direct premium for all non-life companies in 2023-24 increased to ₹.2,89,731 crore from ₹.2,56,894 crore in 2022-23, according to the data of the General Insurance Council.

The gross premium of 25 non-life insurance companies grew about 14 per cent at ₹.2,45,424 crore FY24 when compared with ₹2,14,833 crore in FY23, while for the five standalone health insurers, gross direct premium grew 26 per cent at ₹33,116 crore as against ₹26,244 crore.

Two specialised insurers – Agriculture Insurance Co of India Ltd and ECGC – reported a decline of 29 per cent in their combined gross premium at ₹11,190 crore in FY24 (₹15,817 crore in FY23).

The non-life industry continues to be driven primarily by the health and motor insurance segments though it was marginally subdued in FY24 due to a fall in liability, crop insurance and marine cargo, while fire and credit guarantee segments reported subdued growth numbers compared to last year, according to a recent report of CareEdge Ratings.

Non-life segment

PSU player New India, top player in the non-life segment, reported a decline in its market share to 12.78 per cent in FY24 from 13.42 per cent in FY23 amid single-digit growth in its gross direct premium at ₹37,035 crore (₹34,483 crore in FY23). Oriental Insurance Company Ltd has managed to grow its share to 6.31 per cent from 6.08 per cent while United India Insurance Company reported a marginal decline in its share to 6.85 per cent from 6.87 per cent. National Insurance Company also reported a fall in it share to 5.24 per cent from 5.90 per cent as its premium was flat in FY24.

ICICI Lombard, the second largest player in the non-life segment and the top player in the private segment, managed to grow its share from 8.18 per cent to 8.55 per cent, supported by 18 per cent rise in premium. The second big player in the private segment HDFC Ergo reported a decline in its share to 6.41 per cent from 6.48 per cent.

In the standalone health space, Star Health maintained its top position and its gross premium income stood at ₹15,251 crore in FY24 when compared with ₹12,952 crore in FY23, an increase of 18 per cent. Star Health’s market share increased to 5.26 per cent in the overall non-life segment, up from 5.04 per cent in FY23. In the standalone health category, its market share was 46 per cent in FY24, down from 49 per cent in FY23.

“The Indian non-life insurance market will grow at 13-15 per cent in the medium term. The industry’s growth will be primarily driven by the health and motor insurance segments, supported by increasing disposable income levels and a rise across other segments,” said CareEdge.

![]() Comments

Comments