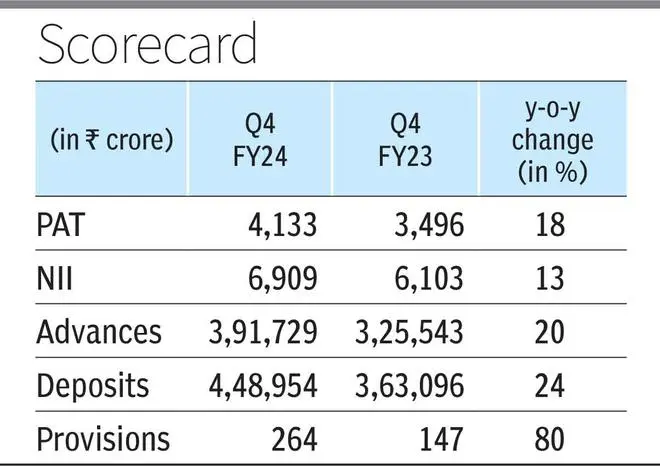

Kotak Mahindra Bank posted a net profit of ₹4,133 crore for Q4 FY24 — higher by 18 per cent on year and 38 per cent on quarter. Despite the healthy financials, the focus during the “earnings discussions was on the recent regulatory action against the bank”.

The central bank, on April 24, asked the private sector lender to stop onboarding new customers through online and mobile banking channels, and to stop issuing fresh credit cards.

MD and CEO Ashok Vaswani said the bank has been seeking guidance from RBI on how to build resilient systems, and is committed to mitigating the RBI action and getting back to pre-action growth levels.

Vaswani said the bank aims to utilise this period to focus on existing customers, enriching the customer experience and deepening customer relationships.

“If we are able to do that, in addition to fixing the tech and getting into expectations of RBI, we will come out stronger on both fronts,” he said, adding that he is more worried about the “reputational impact rather than the financial impact” which is expected to be relatively small in the overall scheme of things.

Vaswani said that the bank will put “far more” effort, money and resources into getting out of the regulatory action as fast as possible. Even so, the whole process including the external audit, could take a “couple of months”, he said, adding that operating costs are also expected to remain elevated going ahead as the bank invests more into technology upgradation.

Operating costs rose from ₹13,787 crore in FY23 to ₹16,679 crore in FY24, of which technology expenses comprised 10 per cent.

Financial metrics

Advances grew 20 per cent y-o-y and 5 per cent q-o-q to ₹3.9-lakh crore as of March 31. Unsecured retail advances, including retail microfinance, comprised 11.8 per cent of total assets as of March 2024 compared with 10 per cent a year ago.

The bank’s management said that while the cards business will be hit, the unsecured book will continue to grow as demand remains strong.

Net Interest Income (NII) for the reporting quarter increased 13 per cent y-o-y and 5 per cent q-o-q to ₹6,909 crore. Net Interest Margin (NIM) stood at 5.28 per cent, declining from 5.75 per cent a year ago.

During the quarter, the bank saw write-back of ₹157 crore of the AIF provisions of ₹190 crore made in Q3 FY24. Even so, net provisions at ₹264 crore were higher than ₹147 crore in the year ago period.

Gross NPA ratio improved to 1.39 per cent as of March 31 from 1.73 per cent a quarter agoand 1.78 per cent a year ago. Net NPA ratio at 0.34 per cent was unchanged sequentially but better than 0.37 per cent in the previous year.

Deposits grew 24 per cent on year to ₹4.5-lakh crore on the back of 35 per cent rise in term deposits to ₹2.2-lakh crore. ActivMoney, launched in Q1 FY24 and TD sweep balance grew 102 per cent on year to Rs 47,052 crore.

Average current account deposits were up 3 per cent and savings deposits by 5 per cent. CASA ratio fell to 45.5 per cent from 47.7 per cent a quarter ago and 52.8 per cent a year ago, with the bank guiding for a CD ratio of 86-87 per cent going ahead.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.