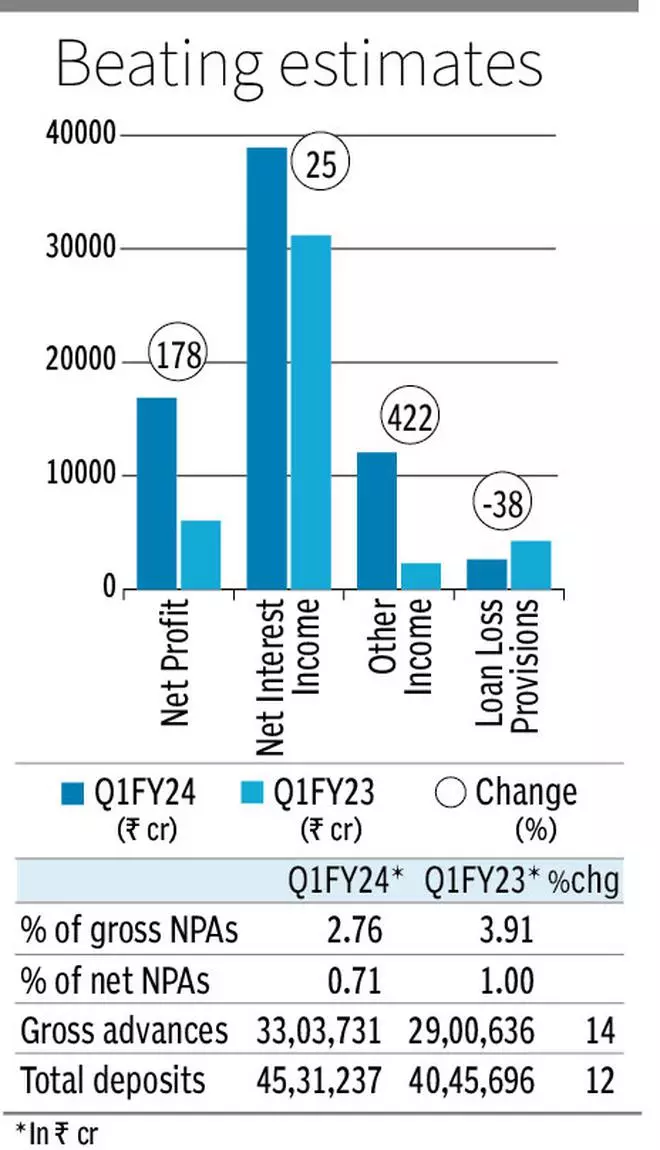

State Bank of India’s first quarter (Q1FY24) standalone net profit soared 178 per cent year-on-year (yoy) in the first quarter to ₹16,884 crore, buoyed by a five-fold increase in other income, robust net interest income, and a decline in loan loss provisions.

The Q1FY24 net profit is SBI’s highest ever net profit for the fourth quarter in succession. The bottomline surpassed broking firms estimates’, which ranged from ₹13,200 crore to ₹16,500 crore.

India’s largest bank reported a net profit of ₹6,068 crore in the year-ago quarter.

Net interest income (NII) rose 25 per cent yoy to ₹38,905 crore (₹31,196 crore).

Other income zoomed 422 per cent YoY to ₹12,063 crore (₹2,312 crore) on the back of treasury gains, growth in fee income, cross-selling, and recovery from advance under the collection account.

Credit demand

SBI Chairman Dinesh Kumar Khara said NII increased on the back of improvements in yields and continuing credit offtake. Other income was supported by Treasury gains.

As demand for credit continues, Khara expects credit to grow 14–15 per cent in FY24, with deposits growing around 13 per cent. The Bank has a corporate credit sanction pipeline of ₹3.5 lakh crore.

In the reporting quarter, global advances grew 13.90 per cent YoY to ₹33,03,731 crore, with domestic and foreign advances rising 15 per cent and 7 per cent, respectively.

The SBI chief emphasised that the Bank is well capitalised (capital adequacy ratio (CAR): 14.56 per cent) to support normal business growth. This level of CAR can support further loan growth of ₹7 lakh crore.

Total deposits were up 12 per cent yoy to ₹45,31,237 crore, with domestic deposits rising 12.60 per cent to ₹43,52,227 crore and foreign office deposits increasing by 22.74 per cent to ₹1,79,010 crore.

Whole Bank net interest margin increased to 3.33 per cent from 3.02 per cent in the year-ago quarter.

Non performing assets

Gross non-performing assets (GNPAs) improved a shade to 2.76 per cent of gross advances as of June-end 2023 from 2.78 per cent as of March-end 2023. Net NPAs edged up marginally to 0.71 per cent of net advances from 0.67 per cent. The Bank sees net NPAs at 0.50 per cent by March-end 2024.

Loan loss provisions declined 38 per cent to ₹2,652 crore (₹4,268 crore).

Special mention advances rose to ₹7,221 crore as of June-end 2023 from ₹3,260 crore as at March-end 2023.

Khara underscored that the Bank was able to pull back ₹1,500 crore in July from the aforementioned advances.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.