As the ruling NDA seeks its third term in office, the rapid strides made in digitising payments and the entire financial services ecosystem have been among its main achievements. The last 10 years have seen the country emerging as a major global innovator and driver of e-commerce, digital payments and financial services.

While measures such as UIDAI were being rolled out even before 2014, for the NDA government, one of its key legacies will be the implementation of an integrated digital ecosystem, orchestrated on the shoulders of the National Payments Corporation of India (NPCI).

From the introduction of Unified Payments Interface (UPI) and FasTag in 2016 to positioning RuPay to challenge the duopoly of Visa and Mastercard, and more recently taking UPI international, there’s been no looking back.

While demonetisation and the Covid-19 pandemic acted as catalysts to accelerate the pace of digital adoption in the country, the government pushed people to get onboarded onto public digital infrastructure through timely initiatives such as mandating Aadhar, introduction of GST, and the push for JAM (Jandhan Yojana, Aadhar, and Mobile) trinity.

This not only brought more people into the fold, but also helped support the agenda of financial inclusion through ease of access and better internet connectivity.

Volume of mobile transactions increased 38 per cent to 6,295 crore in H2 CY23 whereas the value of transactions rose 31 per cent to ₹152.33 lakh crore. Between January and December 2023, the volume of transactions was up 34 per cent whereas value was up 33 per cent.

This also encouraged the growth of a whole new industry of financial technology companies or fintechs, which have significantly altered Indians’ relationship with money.

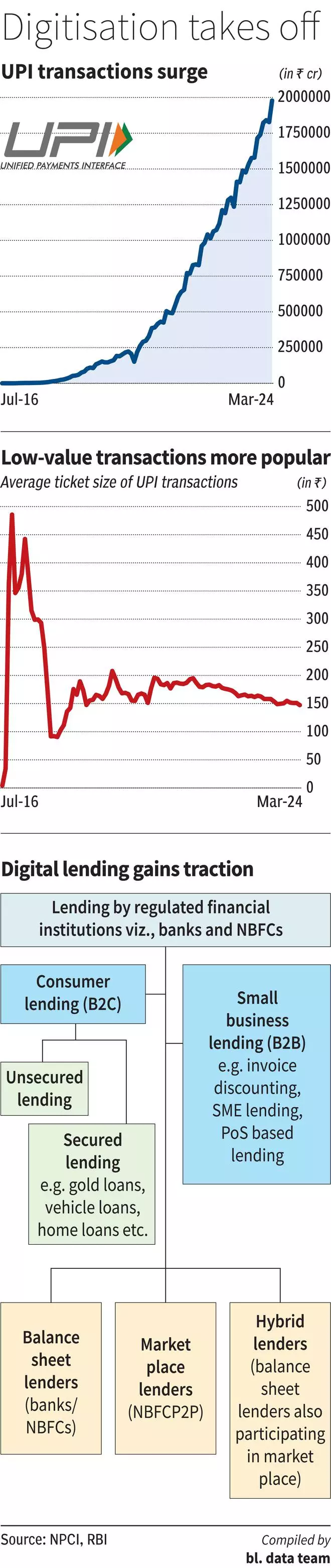

UPI-based payments

The most visible fintech innovation has so far been in UPI-based payments due to its customer facing nature, with the sector seeing huge investments from both foreign and domestic institutions. The UPI network saw record transactions worth ₹19.78 lakh crore in March 2024, 40 per cent higher on year. The number of transactions rose 55 per cent to 1,344 crore during the month, also a record high. In FY24, UPI processed 13,115 transactions aggregating to ₹199.29 lakh crore compared with 8,376 crore transactions worth ₹139 lakh crore in FY23. It is expected to breach 100 crore transactions per day by FY27, as per a report by PwC India, which projects UPI to account for 90 per cent of retail digital payments volume over the next few years. While payments in itself is not a monetarily lucrative business, it heralded a culture of ‘super apps’ from both BFSI and other companies alike, largely due to their potential in paving the way for converting data points and insights into targeted and customised offerings.

Further, the government push for back-end or B2B digitalisation has helped improve data collection, availability of data and access to data, resulting in great insights into consumer requirements, spends and credit behaviour, cash flow or bank statements, credit history, and repayment capabilities.

QR codes

UPI QR codes grew 57 per cent from July 2022 to 31.7 crore as of December 2023, and Bharat QR codes grew 32 per cent to 59.6 lakh, as per a recent Worldline India report. Point of Sale (PoS) terminals expanded 26 per cent between July 2022 and December 2023 to reach 85.6 lakh. Private sector banks dominated the space with a market share of 73 per cent. The number of toll tags issued grew 45 per cent to 8.12 crore as of December 2023. The volume of transactions through FasTags were 13 per cent higher at 189 crore and the value was up 20 per cent to ₹31,948 crore.

Combined with increased customer convenience and fintech development, data sourced from these customer touchpoints has proved to be the guardrails for innovation in digital lending, investments, wealth management, stock broking, cards, banking services, insurance distribution, toll collection, and bill payments.

As per an Experian report, currently 60 per cent of travel, 40 per cent non-grocery retail, 30 per cent education, 25 per cent food and beverages services and 6 per cent of pharma/grocery transactions are done through digital channels. India is projected to be a $800 billion digital consumer economy by 2030, a ten-fold growth from $90 billion in 2020. Further, the share of digital lending is seen rising from 15 per cent in 2020 to 40 per cent by 2027.

Huge investments

The last decade has seen financial companies investing huge sums of money into product innovation, technology upgradation, strengthening the digital infrastructure, research and development, cyber security, top class digital distribution channels and customer touch points, and more recently AI & ML.

However, this rapid growth has brought with it several concerns on corporate governance, cyber security, frauds, data storage and breaches, mis-selling and the growth of unregistered entities. RBI, while being relatively proactive, has in several instances left trying to catch up with the initial pace of development in the sector.

The second half of the decade then also saw the introduction of several licences and frameworks, aimed at allowing for their growth while bringing them into the fold of the formal banking system. The categorisation of different fintech, their use cases and the digital lending guidelines introduced in 2022, were some key landmarks in this regard, bringing a semblance of sanity to a previously chaotic fintech landscape.

The fintech ecosystem is still in nascent stages and continues to evolve, and so do the regulations around it. While there is still distance to cover in terms of complete financial inclusion and digital adoption, the last 10 years have been nothing short of a case study on the digital transformation and the role of fintechs in nudging India into the next phase of development.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.