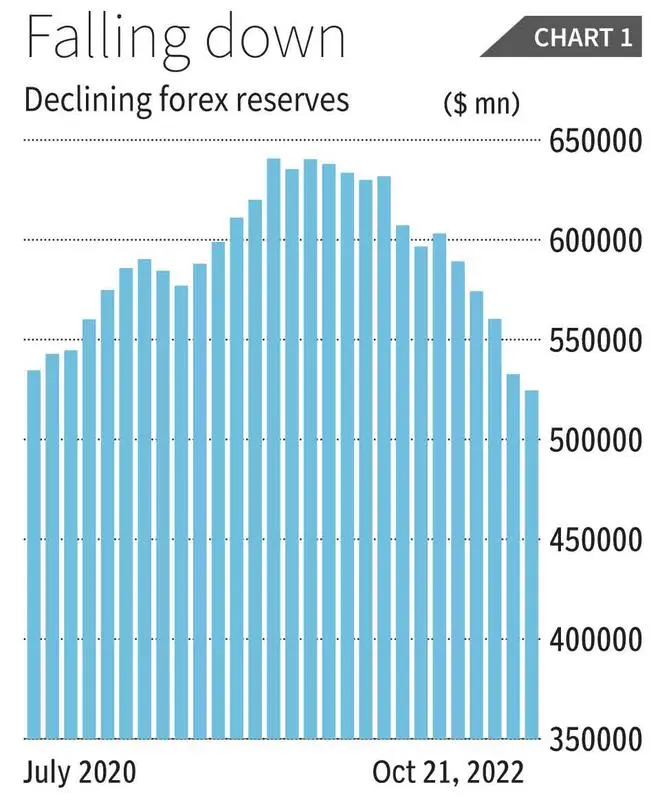

A sharp and rapid decline in the dollar value of the Reserve Bank of India’s foreign exchange reserves has caught the attention of interested observers. Reserves that had risen from around $543 billion in August 2020 to $641 billion in August 2021, have since been in decline (Chart 1). The reserve level touched $525 billion on October 21, 2022.

While the evidence of decline is clear, the explanation for the decline is not. The RBI has said that this is not a cause for worry since more than two-thirds of the fall in reserves in the current fiscal year was due to revaluation in the face of a stronger dollar. The dollar value of total reserves is affected by valuation shifts, as the exchange rate between the dollar and other hard currencies (such as the euro, pound or yen in which reserves are held) changes. The RBI, it appears, has been attempting to respond to this development. India’s investment in US treasury securities rose by $9.2 billion in August to $221.2 billion, which possibly points to realignment of its investment of foreign exchange reserves.

Yet the influence of valuation changes has been strong in recent months as the dollar has appreciated by a substantial margin vis-à-vis other currencies. While over April to June 2021, valuation changes had lifted the value of reserves by $2.2 billion, during April to June 2022 such changes had resulted in a fall in reserves to the tune of $22.7 billion. This is to an extent comforting, because it suggests that dollar appreciation rather than an actual depletion of reserves explain the trend.

But, since much of India’s imports are denominated in dollars, it is the dollar value of reserves that matter as a buffer for financing imports in a situation where foreign exchange earnings and/or inflows are low or negative. Moreover, despite net foreign direct inflows of $13.6 billion during April-June 2022, the change in reserves excluding the effects of valuation shifts had fallen to a positive $4.6 billion as compared with a much higher $31.9 billion during April-June 2021 when the inflow of foreign direct investment was a lower $11.6 billion.

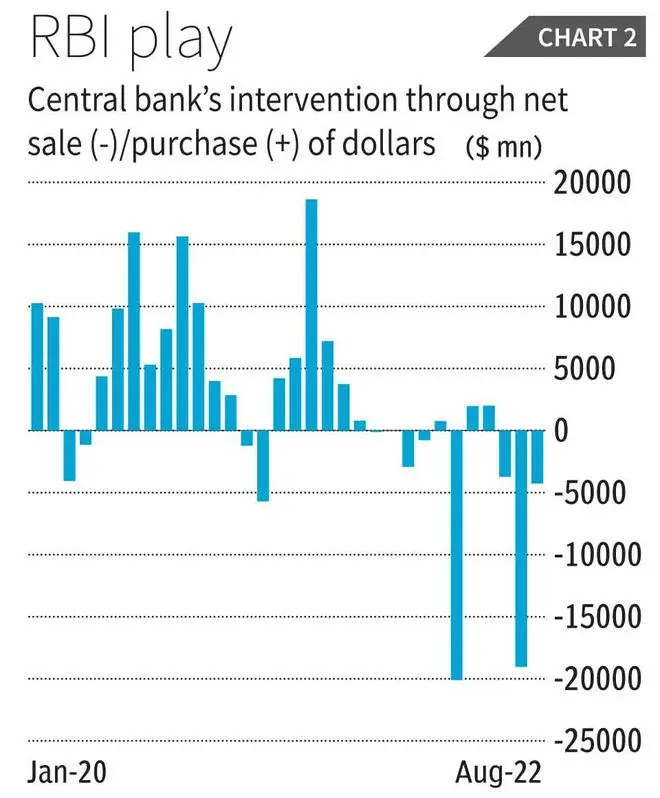

Moreover, the numbers on valuation changes do not tell the whole story. Rather, figures on RBI’s intervention in foreign exchange markets show that the central bank, which was a net purchaser of foreign exchange through much of 2020 and the first nine months of 2022, has turned net seller subsequently, selling around $20 billion worth of foreign currencies during each of the months of March and May 2022 (Chart 2).

The central bank’s open market operations are principally meant to stabilise the rupee vis-à-vis other currencies, with purchases made when large inflows of foreign exchange lead to significant rupee appreciation and sales undertaken when outflows under various heads rise and the value of the rupee depreciates. When the RBI deploys its holdings of foreign exchange to stall depreciation, it depletes a part of its reserves.

Rupee stress

The rupee has been under stress for some time now, for two reasons. First, with central banks in the US and other advanced countries resorting to monetary tightening and a hike of interest rates, foreign institutional investors (FIIs) have been withdrawing from the Indian market. FII outflows during April to June 2022 amounted to $14.6 billion, as compared with an inflow of $0.4 billion during the same period of the previous year.

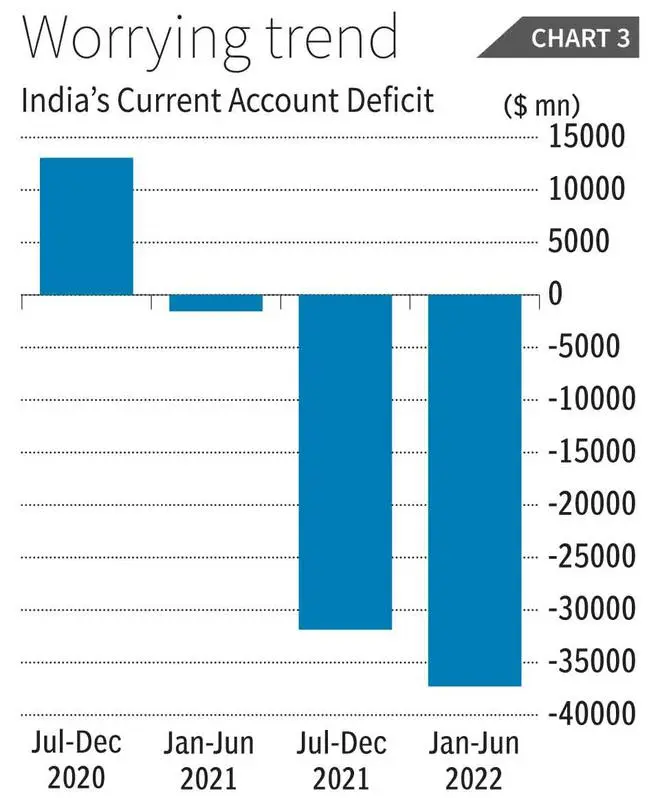

Secondly, India’s trade and current account deficits have been widening. India recorded a current account surplus of $13.1 billion during July to December 2020 and a small deficit of $1.6 billion during January to June 2021. Compared with that, the deficit stood at $31.9 billion during July to December 2021 and $37.3 billion during January to June 2022 (Chart 3).

The outflow of FII capital in itself should not have led to any substantial decline in reserves, because during the April-June 2022 period foreign direct investment inflows amounted to $13.6 billion. So, the net outflow of investment was only around $1 billion. In addition, the April-June 2022 period saw a relatively high net inflow of short-term credit to the tune of $8.8 billion as compared with $1.9 billion a year earlier.

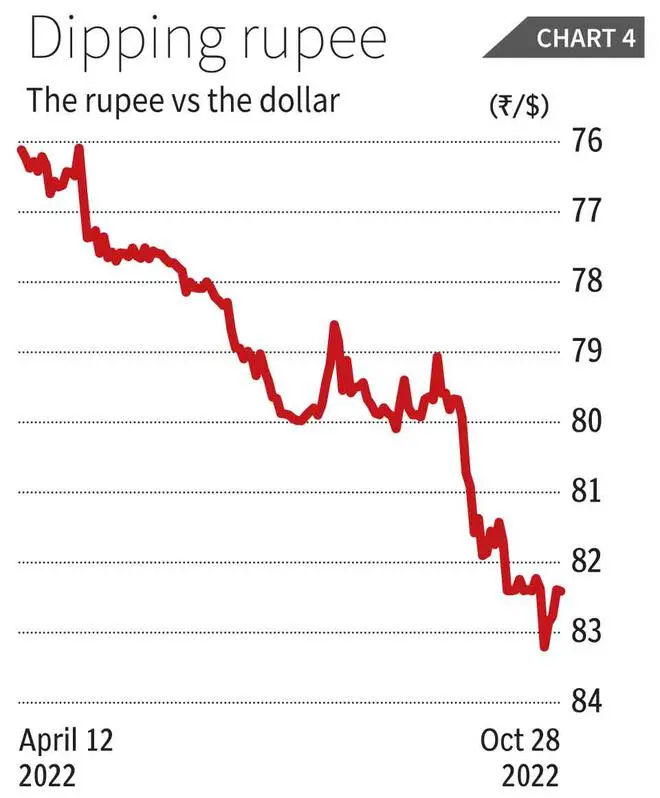

The RBI’s operations involving sale of foreign exchange have been geared to stall rupee depreciation resulting from such pressures. What is of concern is that despite the RBI’s actions, the decline in the rupee has persisted. From around ₹76 to the dollar at the beginning of the fiscal year, the RBI’s rupee reference exchange rate had depreciated by around 8 per cent to ₹82 to the dollar by the end of October (Chart 4).

It is indeed true that the rupee is not the only currency that has depreciated against the dollar, as that currency was strengthened by a combination of the flight of capital to safe dollar-denominated assets as well as the recent hikes in interest rates that has reduced the differential of US rates from that in other countries.

But, as noted, weaknesses in India’s external payments situation have had a major role to play in driving depreciation and its intensity. This possibly explains why the RBI’s efforts have not yielded the results it expected, and rupee depreciation has persisted.

One factor precluding alarm with respect to the decline in reserves is the high level of the dollar value of the reserve that had been accumulated, which peaked at more than $640 billion before the decline began. On the other hand, the pace of decline is disconcerting, with erosion to the tune of $116 billion in a matter of 14 months. This is of significance because unlike in the case of a country like China, where current account surpluses played a role in building reserves, India has almost consistently recorded deficits in its current account. It is because net inflows on the capital account in the form of investment and credit have far exceeded current account financing needs that reserves were built up.

That is, India’s reserves have as their counterpart accumulated liabilities. This makes the country prone to loss of confidence in the currency that could result in destabilising depreciation that not only contributes to domestic inflation but also to adverse effects on the balance sheet of firms and institutions that have borrowed in foreign currency.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.