The Indian economy is delicately poised. Growth is picking up but a strong, durable and sustainable growth trajectory is missing as capital formation or what is commonly referred to as investment has not picked up, particularly in the private sector. Besides, inflation has continuously remained above the target average of 4 per cent.

Recognising that investment spending is predominantly guided by interest rates, the monetary policy has an accommodative stance coupled with no change in policy rate. The Centre has allocated higher capital expenditure in two consecutive Budgets (2021-22 and 2022-23) to enhance public investment, hoping it will be complementary to private investment.

Thus, in effect, we have a two-pronged approach that looks good: monetary policy through lower interest rate will help in the short run while fiscal policy will facilitate investment to help push long-term growth through enhanced capital stock.

Conceptually, investment links the present to the future by moving the economy to a higher growth trajectory through higher investment. As evidence suggests, private investment is an important component of aggregate demand that contributed more than 73 per cent to the total investment and accounted for around 22 per cent of the GDP during the period 2017-2020, as calculations based on data in the latest Economic Survey show.

Thus, private investment is the key to sustaining GDP growth momentum. The financial performance of the private corporate sector in Q2-FY-2022 suggests a steady growth in sales but investment indicators reflect subdued activity.

Growth connection

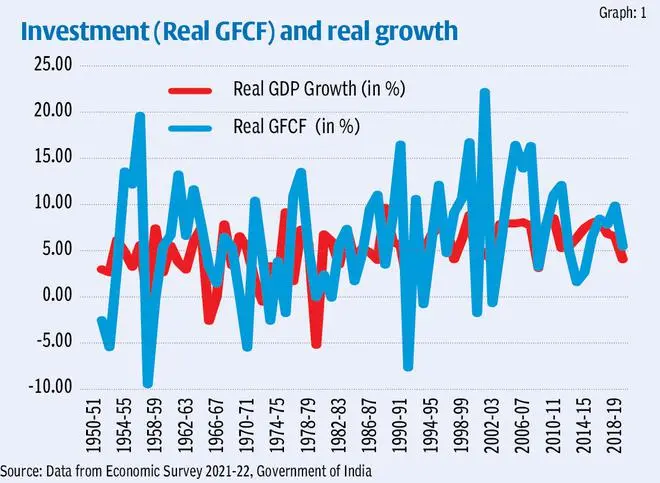

A historical view of data of real GDP and real investment represented by Gross Fixed Capital Formation (GFCF) for the period 1951-2020, reveals that there is a co-movement between these two (Graph 1).

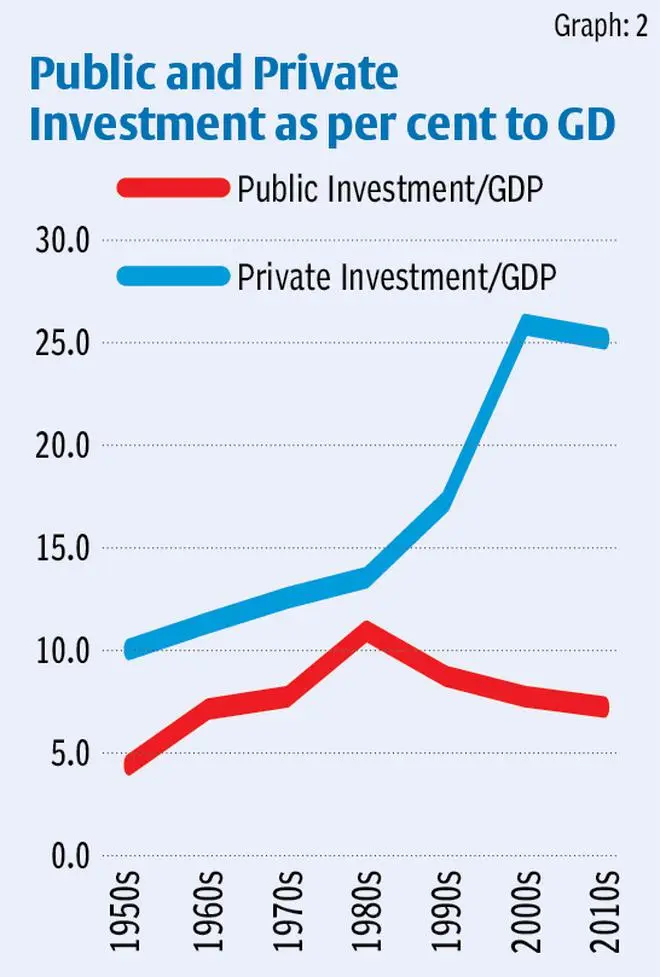

Further, during the same period, the share of private sector investment in GDP is higher than the share of public sector investment in GDP (Graph 2). This is because public investment is guided by budgetary resource allocation. During the pre-pandemic period, due to hard budget constraints and because of its discretionary nature there, has been a lower allocation of investment spending.

However, during the pandemic, the Union Budget has enhanced the capital expenditure allocations substantially to boost public investment at the cost of higher fiscal deficit and debt relative to GDP. These higher allocations could facilitate private investment as it will play a complementary role to private investment.

Private sector investment relative to GDP has been decelerating and has remained mostly stagnant during the decades of 2010s, for example, at 22 per cent of GDP in the period 2017-2020. This could be attributed to weak business sentiment.

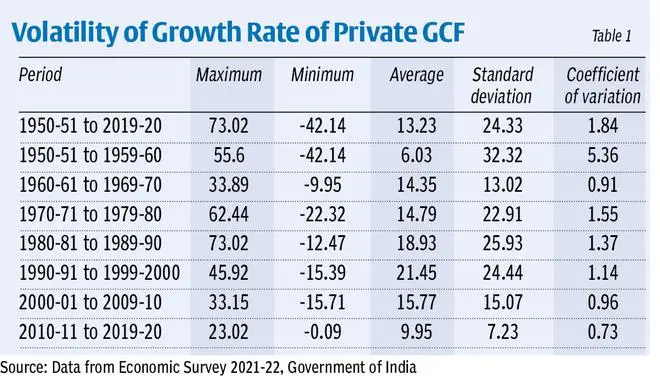

We also see volatility in private sector investment, as shown in Table 1, where technical analysis on fluctuations in private sector business investment is set out as a measure of volatility. As it may be seen, private sector investment is highly volatile and this development questions the reliability of private investment.

During the pandemic, the situation further deteriorated. According to an RBI study (published in September 2021 issue of the RBI bulletin), there has been a noticeable drop in the number of new projects sanctioned and also slower progress on projects already in the pipeline.

The RBI study further stated that data on the phasing plan (when the project plans are documented, the project deliverables and requirements are defined and the project schedule is created) for 2021-22 point to persisting near-term risks to the investment outlook.

More importantly, during 2021-22, there was a decline in resources raised through international bond market by around 59 per cent, which remained positive in the previous three years, according to the RBI study under reference. Thus, the capex of the private sector overall presents a dismal picture.

The forward-looking survey on industrial outlook published by the RBI (February 2022 RBI bulletin) revealed that in 2020-21, there has been a negative sentiment on industrial outlook measured in terms of 60 per cent of the net response. Furthermore, business assessment taking into account the overall business situation, production, order books, inventory of raw material and finished goods, and profit margin as per the RBI study remained in the contraction zone and business expectation declined.

Capacity utilisation

A key factor influencing the private investment in the manufacturing sectors is the level of capacity utilisation (CU). Conceptually, CU is ratio of actual output to potential output. Potential output capacity critically depends upon available capital and labour to produce maximum output.

The order books, inventories and capacity utilisation survey (OBICUS) of RBI presents the level of CU. Higher CU, accompanied by order book growth, signals robust demand conditions in the economy. According to the RBI of February 2022: “at the aggregate level, CU for the manufacturing sector recovered to 68.3 per cent in Q2:2021-22 after the waning of the second wave of Covid-19 pandemic in the country, which had caused plummeting of CU to 60.0 per cent in the previous quarter.”

Thus, capacity utilisation is at a lower level than the pre-pandemic level of around 75 per cent. CU functioning below the long-term average reflects both demand and supply constraints.

It is true that the private sector makes business decisions for investment to earn profits. It is important to note that capital goods have a long gestation lag. Investment decisions critically hinge on (a) level of output produced by new investment, (b) taxation system, (c) cost of credit reflected in lower interest rate regime, (d) timely delivery of credit and (e) business expectations of the domestic and global economy.

One moot question is: How to translate the volatile private investment to a more reliable one? What is sorely missing with the private sector is the “animal spirits”, implying a “spontaneous urge to action rather than inaction and not as the outcome of a weighted average of quantitative benefits multiplied by quantitative probabilities” as propounded by Keynes.

Thus, a positive sentiment is warranted to boost investment which should be guided by “spontaneous optimism rather than mathematical expectation.” But if this optimism is lacking, what does it tell us about our nation, our policies and our direction?

The writer is a former central banker and a faculty member at SPJIMR. Views expressed are personal. (Through The Billion Press)

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.