The scathing report by Hindenburg Research on the Adani Group has put the spotlight on short selling, a practice nearly as old as the stock market. Regulators around the world, the courts, investing masses...everybody has once again started taking notice of short sellers aka the misfits in the investing world.

Why? Because, in the conventional investing world, the buy-and-hold philosophy is heavily marketed as the cure for all investment maladies, and everybody expects asset prices to only rise. So, swimming against the tide by selling something first, contrary to buying first, does bring its share of the limelight, and controversies. This is probably why short sellers are seen as outcasts as they bet on asset prices going down!

But for every Warren Buffett, or Rakesh Jhunjhunwala in the long-only investment world, there would be a Jim Chanos or George Soros — like a true bear smacking its lips — as they seek out yet another security whose shares they believe to be overvalued, whether by exuberance or fraud or simply based on technicals. Here is a lowdown on short selling, how and why investors do it, the pros and cons, local and global perspective, and much more.

What it is

Short selling, or shorting, is a tricky concept primarily because we are not used to shorting in our day-to-day transactions. Be it groceries, apparel, real estate, eating out, travel etc., we buy it first. The current price, subconsciously, is held out to be right. So, buying first is a highly intuitive transaction. To generate profit in investments, buying first means the entry price has to be lower than the exit price. However, in a short sale, the transactions are carried out in the exact opposite direction i.e., to sell first and buy later. For instance, you first sell a security for ₹100 and then buy it for ₹80, pocketing ₹20 profit (pre-tax and charges).

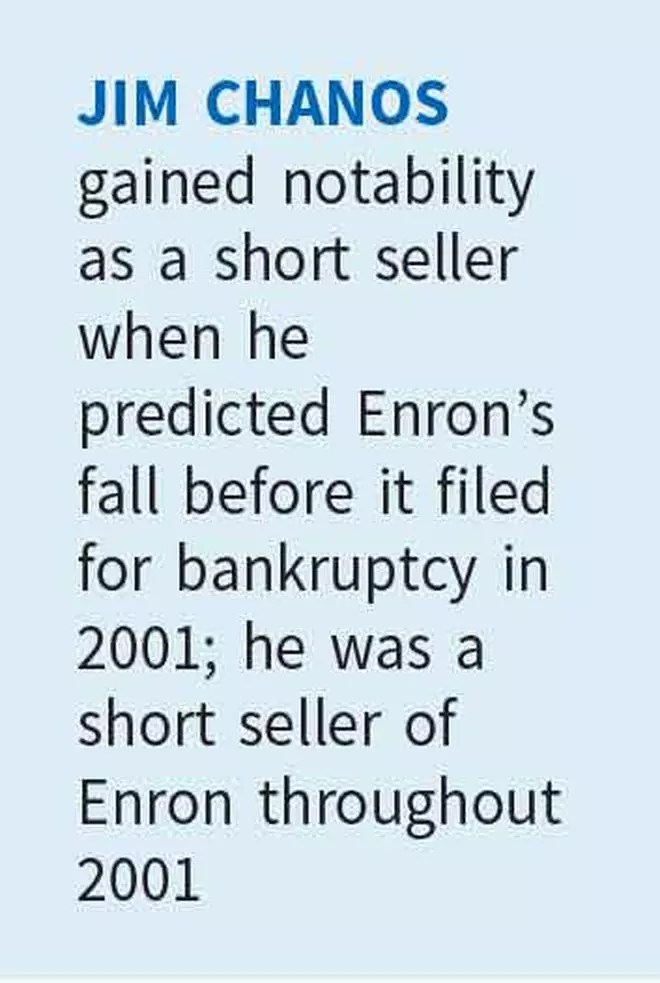

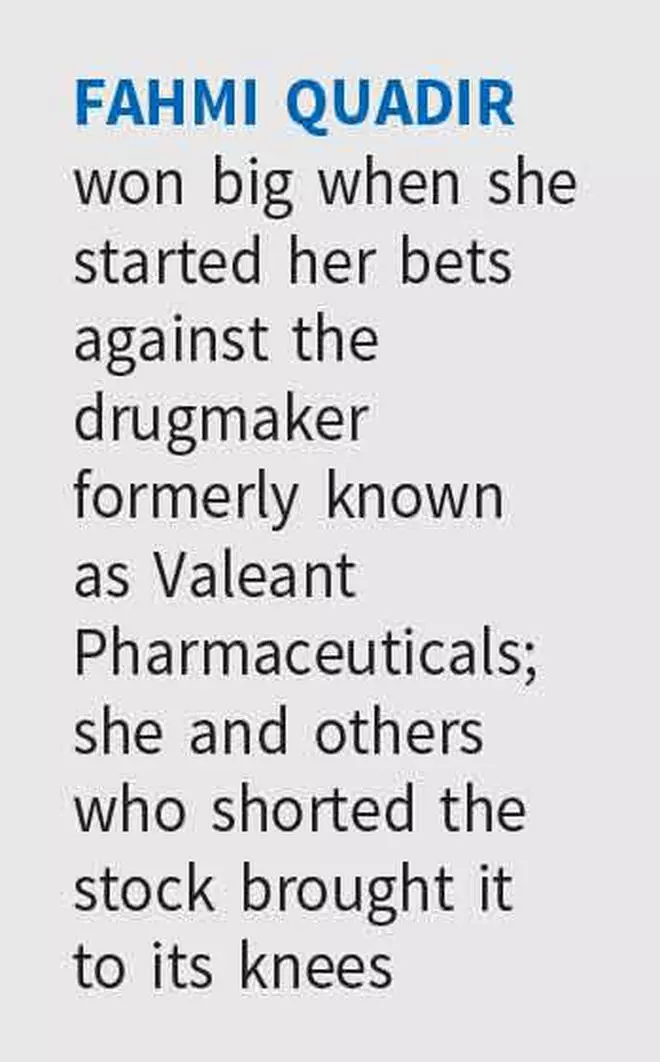

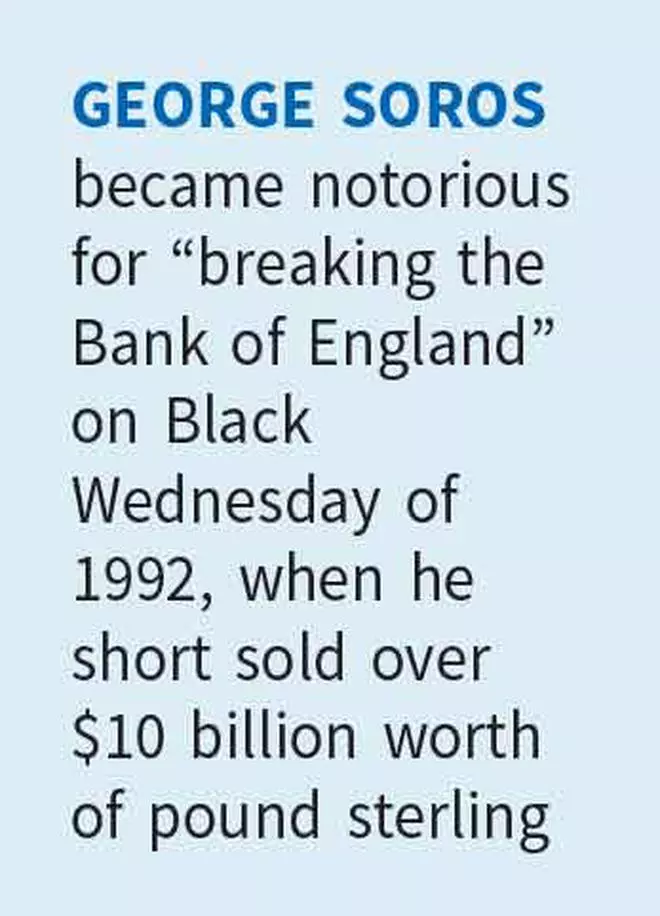

The earliest example of short selling was when Isaac le Maire, in the early 1600s, short-sold the stock of the Dutch East India Company. Over the years, Jacob Little in the 1800s, Soros in 1992 for ‘breaking the Bank of England’, Chanos for shorting Baldwin-United and Enron or Fahmi Quadir shorting Valeant — market personalities have reaped rewards that would dwarf those of many ‘long’ investors.

Holding a bearish opinion and acting upon it are two very different things. Sans the adrenalin and thrill of going short, as a practice, short selling is a very difficult way of investing. Short-selling returns are capped (since price can only go as low as zero) while the potential losses could be unlimited. This means it is truly for those with a very high risk-acceptance mentality. Short selling aids the efficiency of price discovery and is generally good for markets.

Why short, when to do it

Equity short sellers typically use one or more of the following approaches to identify targets they feel trade at higher prices than they should.

Fundamental analysis: Analysing a company’s financials helps them determine if its stock may be a candidate for a decline in price. An impactful change in fundamentals warrants such a stance.

Technical analysis: Patterns in a stock’s price movement help determine if the stock is on the cusp of a downtrend. Technical-based shorting is practised every day by traders in the spot market or by using derivative instruments. Typically, technical short sellers use scenarios such as selling a pullback in a downtrend, entering within a trading range and waiting for a breakdown, or selling into an active decline.

Thematic research: This approach involves betting against companies whose business models or technologies are outdated and thus face implosion. A popular example here is the large institutional short selling of the shares of GameStop, which backfired in 2021.

Forensic short selling: Spotting cooked-up balance sheets or outright frauds comes under this category. Some of the world’s most astonishing frauds have come to light, thanks to such short sellers. Such frauds usually took place in companies involved in the prevalent hottest sectors of those times.

Market-neutral strategies: In this form of investing, the purchase of undervalued securities is combined with the short sale of overvalued securities in such a way as to make money, irrespective of market direction. The aim here is to neutralise the direction of the overall market. This strategy is also referred to as zero beta. Sophisticated hedge funds and high net-worth investors use long-short strategy, where they take a long position in under-priced stocks while selling short overpriced shares.

Regulated short selling is a legal practice. Securities market regulators in most countries, and in particular, in all developed securities markets, recognise it. The International Organisation of Securities Commissions (IOSCO) has also reviewed short selling and recommended transparency of short selling, rather than prohibiting it.

Short selling can be effective under a few scenarios but do bear in mind the sword can cut both ways and be counterproductive too.

Low float: Stocks with low float i.e., a smaller number of shares available for trading, are susceptible to wilder price swings on either side based on a comparatively smaller trade volume. Short selling such a stock could mean that only a few such orders from other market participants can bring the counter to its knees, and thus drive the price down — which means profit from a short seller’s perspective. In the Hindenburg-Adani saga, certain Adani group stocks, such as Adani Green and Adani Total Gas, hit lower circuits almost every day because these stocks were relatively low-float. However, such low-float counters are also notorious for short squeeze as just a bit of buying can lift up the stock.

High promoter pledges, margin calls: When the promoter of a company has pledged a high amount of stock ownership and the stock begins to fall, there is a high possibility of margin calls. A margin call occurs when the value of securities pledged in a brokerage account/lender falls below a certain level. This requires the account holder to deposit additional cash or securities to meet the margin call. If margin calls are not met by the promoter, then the lender offloads the equity in the open market, thus driving down price sharply. For a short seller, this is a good scenario because large supply of shares and falling price means good tidings.

Recall how, in 2019, the Anil Ambani-led ADAG Group reached an in-principle standstill understanding with more than 90 per cent of the lenders at the promoter group level, after L&T Finance and Edelweiss Group had dumped group company shares, causing the unprecedented fall in share prices.

How it is done, risks

Here is how one usually shorts stocks in the Indian market.

Shorting stocks in the spot market:Here you sell ordinary shares you think will fall in value. While institutional investors are mandated to disclose upfront at the time of placement of order whether the transaction is a short sale, retail investors in India are permitted to make a similar disclosure by the end of the trading hours on the transaction day. Brokerage firms lend stock to customers who engage in short sales. As with buying stock on margin, short sellers are subject to the margin rules and other fees and charges. Margin account route to short selling is extremely popular in developed markets such as the US.

But if you are unable to present shares you short sold because of reasons such as illiquidity or stock hitting the upper circuit, it will be considered as default. In India, the exchange conducts an auction to deliver the short quantities from other sellers, and you could pay 20 per cent extra, plus other statutory penalties.

As a short seller, you should be wary of short squeeze, which occurs when a stock moves higher and short sellers decide to cover their ‘shorts’ or are forced to do so via margin calls. As these short sellers buy the stock to close trade, the stock price rises, creating a situation in which more shorts have to be covered.

You cannot carry forward the short position in the spot market for multiple days. Thus, shorting in the spot market is mostly an intraday affair in India, unless you can borrow shares.

Shorting stocks in the futures market: In this route, there are no restrictions like shorting the stock in the spot market. Short sales are one of the reasons why trading in futures is so popular in India.

When traders are bearish about a stock, they initiate a short position on its futures and hold on to the position for longer periods. Similar to depositing a margin while initiating a long position, the short position also requires a margin deposit.

Note that be it spot trade or futures trade, the stop loss in short selling is always higher than the price at which one has shorted.

In India, you can do short sales by selling a futures contract for a stock or an index. There are roughly 200 stocks eligible for F&O trading.

You can extend your futures position by rolling over the contract every month if you are ready to absorb the mark-to-market losses (in case of adverse movements) when you roll over and absorb an in-built small margin relative to the spot price.

Risk management

Many think short selling capitalises on the mechanics of when a market transitions from higher to lower prices. But short selling strategies can be profitable through uptrends and downtrends as long as strict risk management rules are followed and timing is carefully managed.

If not careful, short sellers get targeted relentlessly and often get trapped in violent short squeezes that blow out the even the most diligently placed stop-losses. Recall how in January 2021, a short squeeze of the stock of the American video game retailer GameStop and other securities took place, causing major financial consequences for certain hedge funds and large losses for short sellers.

Compared to ‘long’ ideas that have the luxury of time to bloom since you own the stocks, short ideas are always on the hook as you have borrowed the shares (or trading on margin money in case of futures) and it comes with a cost.

Many newbies sell a stock short at new highs, but this is a potential recipe for disaster as uptrends can persist longer than predicted by technical or fundamental analysis. A large supply of weak-handed short sellers in strong uptrends provides rocket fuel for driving stock prices even higher.

Risk management strategies for short sellers could include shorting the weakest sectors, not the strongest, avoiding bullish seasonality trends and shorting during confused and conflicted markets.

Under short attack?

While we have so far discussed the many methods of short selling and the potent force it is, long-term investors who have bought a stock may panic when under short attack. But don’t do anything under panic.

It is necessary to understand that when share prices tumble, it may not be a reflection of a change in fundamentals. When a stock falls, immediately the market capitalisation of the company falls but the investor wealth loss reported by media is mostly notional for many investors. If you haven’t sold shares that have been shorted, your loss is purely notional. Whether the large short seller is right or not will be revealed over a period of time. However, if you are a long-term fundamental investor and have done your ground work before buying the shares, a large short seller threat over a stock should not worry you. Remember that stock prices may return to their equilibrium once the storm blows over.

Of course, if the short seller is right, then there may be permanent loss in your investments. So, if you are not sure about your research, it may be a good time to do some scrutiny. Try and gain knowledge about the event and talk to your advisor on what is your expectation from the stock. Decide to stay or exit based on these inputs.

The tendency to stay biased is high if you are already invested in a stock. and there is action around it. You must be careful to ensure the bias does not cause losses for you.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.