Though the market sentiments were beaten down in the last week following yet another sharp interest rate hike in the US, the Sensex, remains flat year-to-date and has fared much better than key global indices in 2022. As the Federal Reserve began hiking rates earlier this year, the Sensex, from its near-term high of 60,611.74 points on April 4, did tank 15 per cent by the middle of June. But just when pundits had predicted the beginning of a bear market, Indian stocks roared back to life and rebounded from nadir. Today, despite last week’s fall, the gain for Sensex stands at a respectable 13 per cent from the lows.

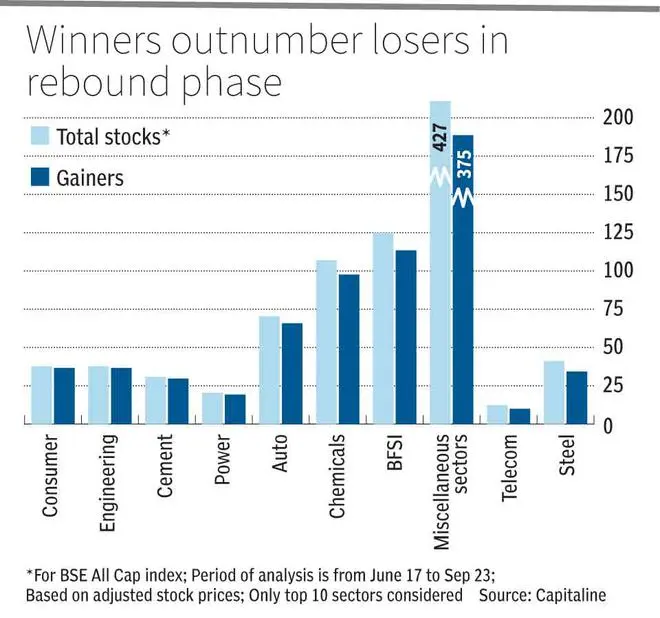

BFSI, Autos, Cement gain

Even as global markets have been on tenterhooks, investor wealth in listed Indian stocks, as measured by the combined market value of about 1,100 stocks that make the BSE Allcap index, is back above the Rs 260 lakh crore mark, a level at which it flirted with before the slide witnessed in April. This has been possible on account of a majority i.e. 87 per cent of stocks jumping from their near-term lows hit in June.

Multiple sectors have led this leg of upturn (from mid-June onwards) and the prominent ones among them are Auto, BFSI, Cement, Chemicals, Consumer, Engineering, Metals, Power, Steel and Trading. Many of these sectors were beaten down badly during the decline phase (April to June), with more than 90 per cent of stocks in BFSI, Cement, Metals, Telecom and Trading dropping in value. BFSI is extremely important sector in terms of index weights; it saw 91 per cent stocks getting sold off in the down period and then 92 per cent coming back to life when recovery picked up pace.

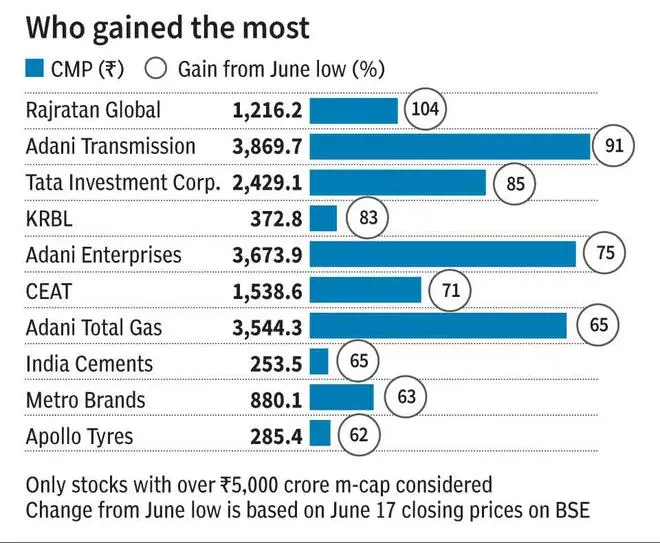

Among the biggest gainers from mid-June in these leading sectors are Repco Home Finance (up 98 per cent), DFM Foods (85 per cent), CEAT (71 per cent), Lumax Auto (70 per cent), India Cements (65 per cent), Parag Milk Foods (54 per cent), DCB Bank and RBI Bank (both up 51 per cent).

Over 85 per cent of stocks across large, mid and smallcap space joined the bull party from June lows, with Vinyl Chemicals TGV Sraac and Jyoti Resins topping the charts in smallcap space, while Metro Brands, Apollo Tyres and IDFC First Bank led the midcap rebound.

Domestic facing businesses have found greater currency with investors, as dark clouds hover around export-oriented companies amid a weak rupee and global macro uncertainties.

Low participation from IT, Pharma

IT, Pharma, Refineries and Energy sectors have participated less in the rebound phase. Interestingly, IT and Pharma had seen over 95 per cent stocks declining during the April-June period. For example, the tier-I of IT stocks fell between 18-36 per cent between April to June. Similarly, Sun Pharma, Divi’s and Cipla dropped 11-22 per cent. When the tide turned, investors did not come back in droves. In fact, the top 4 IT stocks have shed 2-7 per cent from June 17 to September 23. Similarly, 60 per cent of largest pharma stocks have underperformed the Sensex in the recovery period. Fears of a global slowdown has indeed impacted these sectors which derive their revenues from various geographies.

Outlook

Will last week be just an aberration and will the rally continue ? No one can answer this with certainty. But with growth prospects for India remaining robust, domestic facing companies may continue to be more resilient compared to export -oriented ones. However, with interest rates rising and more hikes expected from the RBI in its upcoming policy meet, companies with low debt and interest burden may be able to fare better.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.