Buy high and sell higher is the mantra for investors following the momentum style of investing. But after delivering big-time in the last 10 years, recent months have seen this rockstar strategy turn turtle.

Two out of three stocks making up the momentum indices have lost value, with some more than halving. Rising interest rates have sapped investor risk appetite, causing the tide to turn against momentum strategies.

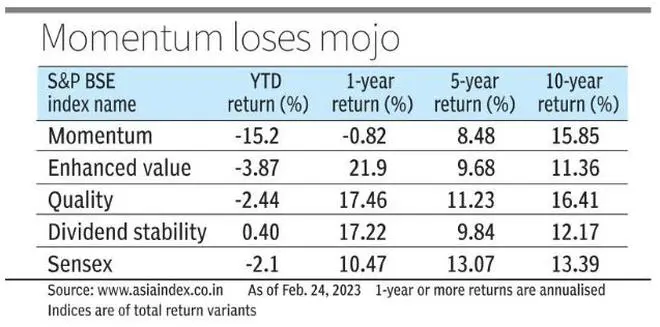

Popular strategy

The tendency of stock price trends to persist is called momentum. If market moves mimic waves in the ocean, a momentum investor sails up the crest of one, only to jump on to the next wave before the first wave crashes.

But a momentum strategy isn’t just about buying stocks that have risen. Typically, funds or portfolio management schemes that follow the momentum style use rule-based frameworks that single out stocks with high risk-adjusted momentum scores, within a time period, say, 12 months.

In the last 10 calendar years, from 2013 to 2022, barring 2018, the momentum strategy didn’t report a loss even in one year. Momentum benchmarks such as BSE Momentum more than tripled in this decade. Compared to 13.4 per cent and 13.7 per cent, the 10-year annualised returns for Sensex and BSE 100, respectively, the BSE Momentum index clocked a higher CAGR of 15.85 per cent. As a strategy, momentum has outpaced those like enhanced value (11.36 per cent) and dividend stability (12.17 per cent) indices.

Given the success of this style, asset managers and advisors were quick to roll out momentum-based investment products. But recent returns have been staid. Out of the eight momentum-based mutual funds in India that manage AUM of ₹2,200 crore, five have been launched in the last 6-7 months. In curated platforms like smallcase, dozens of portfolios based on the momentum style have been launched in the last one year.

While Sensex is down 3.3 per cent in the last three months, momentum strategy indices are down 10 per cent. About 20 of the 30 stocks that make up the S&P BSE Momentum Index have lost ground in the last three months. This number was 50-50 going by 6-month returns.

Momentum stock portfolios have recently been overweight on auto, metals, consumers, chemicals, power and capital goods. Consumer durables and power indices have corrected 8-28 per cent. Sectors such as oil and gas, and consumable fuels have also dipped by 13 per cent. While auto and capital goods have held up, banking has lost 7-8 per cent in the past three months.

“Like all strategies, momentum will take a break every once in a while, and we’ve talked about this in the peak of the momentum cycle (mid 2021) that markets will take a break. In the last one year, hardly anything has actually worked even to beat FD returns, and momentum is also going through a rough patch. These issues are in our view temporary and part of market cycles,” explained Deepak Shenoy, Founder and CEO, CapitalMind.

‘Adani’ effect

The concerted plunge in stocks linked to the Adani Group after the Hindenburg allegations has been one contributor to sub-par performance from momentum styled funds lately. Five Adani Group stocks, which are down 50-80 per cent in the last 3 months alone, are part of the BSE Momentum Index. The Nifty200 Momentum basket features Adani Enterprises, which withdrew its ₹20,000-crore FPO amid volatility after the Hindenburg allegations.

Stocks of banks such as SBI and Bank of Baroda, reported to have lent to the conglomerate, have also faced setbacks in recent times. These are also part of the BSE Momentum Index.

Other laggards

Beyond the Adani pack, stocks such as Page Industries, Escorts, Pidilite, and Titan have tumbled in recent times. In such cases, the decline seems attributable to investors shying away from high valuation stocks as rates rise and growth prospects slow. Select PSU stocks such as NHPC, BEL, HAL, Coal India and PowerGrid, which are part of momentum portfolios, have also corrected.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.