HDFC Life rolled out a new term insurance policy in September this year. Called the HDFC Click2 Protect Super, this new cover comes with many added features apart from the plain-vanilla term policy option. Besides the usual riders and the return of premium option, the policy offers the choice of stepping up or reducing your sum insured over time. You could also bump up your cover with life-stage events such as marriage and childbirth.

Term and health insurance overs are critical for everyone with financial goals and earnings to protect.

Before you opt for the HDFC Click2 Protect Super policy, read on to know how the key features and add-ons work, which are the most suitable riders to take. The minimum age of entry is 18 years.

Flexibility in coverage

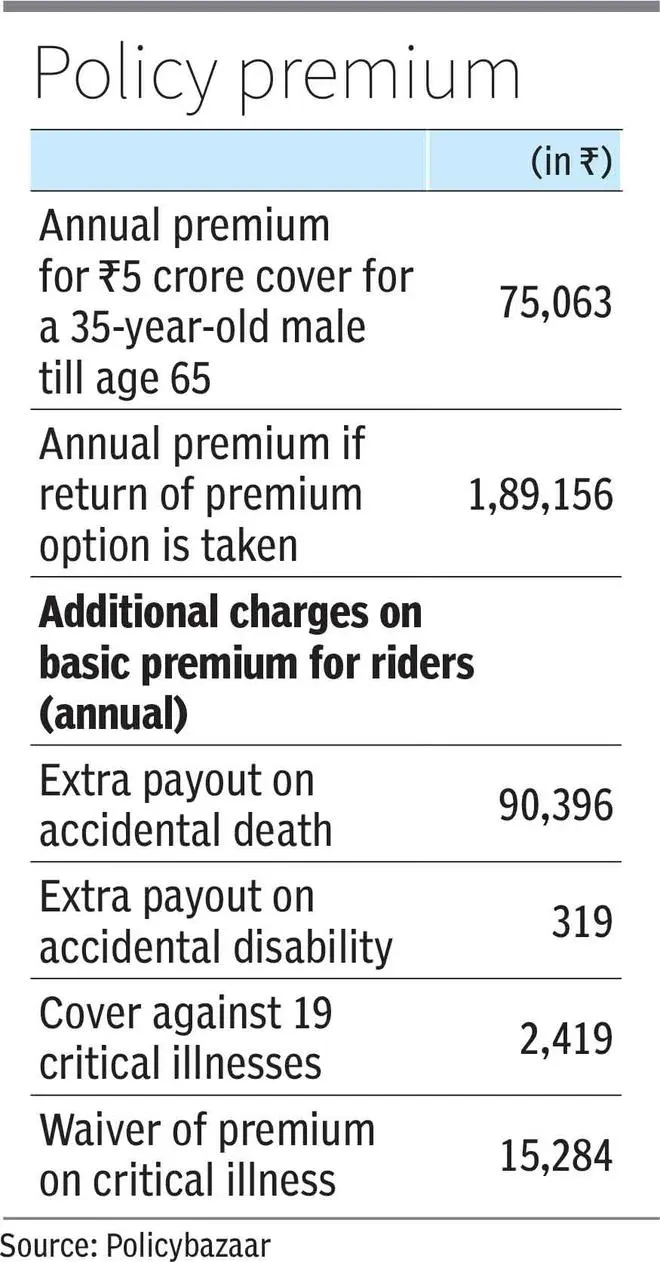

The basic product is like the usual plain term policy. So, you pay premiums periodically for a certain sum insured (say, ₹1 crore or ₹5 crore) and for a specified period — usually till your earning life or up to the time of your retirement — during which you are expected to have achieved all your financial goals and repaid all loans. After the policy period (from, say, age 35 to 65) the cover ceases. You do not get anything back if you survive till maturity. In case of an unfortunate event during the policy period, the sum assured is paid to your nominee (usually your spouse). The premium for a basic cover of ₹5 crore for a 35-year-old male till age 65 is ₹75,063, according to Policybazaar.

But HDFC Click2 Protect Super allows you to step up or step down your cover. If you feel that your current cover isn’t enough, you have the option of increasing it in two ways.

One, after the first five policy years, you can increase your cover by a simple rate of 10 per cent every five years. So, you would have 100 per cent coverage from years one through five, 110 per cent of sum assured from years 6-10 and so on. Of course, you are allowed to go up to a maximum of 200 per cent of the sum assured.

You can also increase your coverage at a simple rate of 5 per cent every year, starting from the second year of your policy. Therefore, you will have 100 per cent cover in the first year, 105 per cent of the sum assured in the second year, 110 per cent of the cover in the third year and so on.

Another life stage option allows you to increase your cover by up to ₹50 lakh after your first marriage and ₹25 lakh each upon the birth of the first and second child.

As your income increases and goals expand in monetary value, you may find these two options helpful.

Payouts on terminal illness and riders

When the policyholder is diagnosed with any terminal illness (multiple-organ failure, cancer, etc.), HDFC Click2 Protect Super gives the sum assured up to a maximum of ₹2 crore. The balance is paid to the nominee upon the death of the policyholder. Terminal illness must be certified by a couple of medical practitioners and must be regarded as an ailment that could lead to death within six months from diagnosis. This accelerated benefit will not be given if the policyholder crosses 80 years of age.

Then there are the riders. The return of premium is always an unnecessary option. It increases the premium by 2.5 times (see table). You can invest in the regular option and invest the balance amount in other productive avenues such as mutual funds, especially given the long policy periods, and derive much better returns and a higher corpus.

The premium for additional accidental death payout is quite high and is generally not needed as you anyway decide your sum assured after considering all your financial goals and loan liabilities.

Since there is a payout after diagnosis of critical illness, a waiver of premium after this diagnosis serves limited purpose.

Critical illness covers are best taken with medical insurance policies.

What should you do?

Premium data from Policybazaar indicates that HDFC Click2 Protect Super charges a much higher premium (to the tune of ₹12,000-₹14,000) for a ₹5-crore cover compared to ICICI Prudential iProtect Smart and Max Life Smart Secure Plus. But it may still be worthwhile for those without a term policy to consider it, and opt for the step-up option of increasing coverage by 5 per cent from the second year, especially if they start with a low sum insured. The other riders and options can be given a miss.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.