The Nifty auto index is touching all-time highs and the Nifty has also rebounded close to its peak seen in December 2022. However, there are still some pockets of opportunity left in the markets. The stock of Amara Raja Batteries (ARBL) is one such. At ₹625 now, it is at a 44.5 per cent discount to its all-time high touched in 2015. At 15 times trailing 12-month earnings, it is much cheaper than peer Exide Industries trading at about 20 times. ARBL has corrected since December 2022, where it touched one-year high of ₹668 alongside the broader market peak.

The electric vehicle (EV) narrative has been a big dampener for battery makers in the last few years as their core product, i.e. lead acid batteries for vehicles, will be replaced by lithium ion ones in EVs.

EV sales too have caught on in a big way since the pandemic, with FY23 seeing a 157 per cent growth in sale of registered EVs to about 11.8 lakh units. ARBL’s failure to qualify for PLI for the manufacture of ACC batteries has been another negative. However, the fear may be overdone. For one, EV sales constitute just 5.5 per cent of the conventional vehicle sales in FY23 and the path to reduce vehicular emissions is also surrounded by policy uncertainties.

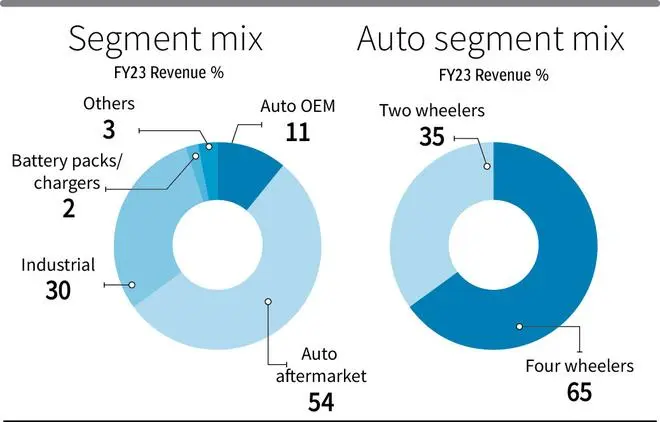

Secondly, battery makers are not dependent on new vehicle sales alone as there is a recurring replacement demand for batteries from existing vehicles. Thus, the existing population of on road vehicle needs to be serviced till end of life, even if some of the incremental new vehicle sales move to EVs. Three, ARBL is also investing in manufacturing lithium batteries with an initial 2Gwh cell capacity and 2Gwh pack capacity expected by FY25 and a peak cell capacity of 16Gwh expected by FY32. Four, industrial batteries (30 per cent of revenues) provide the needed diversification from the cyclical auto industry. In this segment, ARBL has a 60 per cent market share in telecom batteries, where volumes are being supported by the 5G rollout.

Considering these factors, investors with an appetite for risk and a long-term perspective can buy the shares.

Game plan

Currently, ARBL derives almost two-thirds of its revenues from automotive batteries (lead acid) and in that, predominantly from four-wheelers and the replacement markets (see chart). After two years of double-digit growth each, SIAM, the industry body, expects growth in new car sales volumes to moderate to 5-7 per cent year-on-year in FY24. However, robust new car sales in the last 2-3 years imply that the replacement demand for these vehicles would hold the fort for ARBL in the near to medium term, when cyclicality in new vehicle kicks in. Usually, companies also have good margins in the replacement segment. While sale to OEMs will moderate, the company still expects it to be in high single digits.

What holds promise for ARBL for the long term is its new energy business. In FY23, about ₹250 crore of revenues came from sale of packs and chargers under this business, predominantly to three-wheelers and the telecom segment. This business fetches 3-4 per cent EBIDTA margins now and the company is aiming to touch ₹750 crore revenues in FY24, having roped in two-wheeler OEMs for commercial supplies recently. For perspective, two-wheelers are the largest selling EVs in the country, constituting about 60 per cent of the total EV sales today. While there are some headwinds to electric 2-wheeler sales today from the subsidy cuts by the government, adoption is still expected to be faster here than other segments.

ARBL will hold the new energy business through 100 per cent subsidiaries. Amara Raja Advanced Cell Technologies will hold the upcoming Lithium battery capacities at Divitipally in Telangana and the battery packs. Amara Raja Power Systems, which manufactures chargers, was held by promoters and ARBL acquired it recently for a cash consideration of ₹133 crore. The company had ₹184 crore of revenues, EBITDA Margin of 11.12 per cent and PBT margin of 17.4 per cent in FY23. For lithium cell technology, in-house R&D as well as investments made in a few tech companies such as Log 9 are expected to provide support. Homologation process with customers is on the anvil. On the raw material side, a 25 per cent domestic value addition is expected initially. For these plans, a total of ₹1,300 crore capex is estimated over the next 2-2.5 years and will be financed with internal accruals as well as some leverage on ARBL. The debt-to-equity ratio for ARBL is now at a comfortable 0.03.

Financials

ARBL has seen double-digit sales and profit growth in the last few quarters, with reported profits in the latest quarter growing by 40 per cent year-on-year to ₹138 crore ( adjusted profits grew by 74 per cent to ₹171 crore). Sales in Q4 grew by 11.4 per cent to ₹2,429 crore. Operating margins compressed to 9.9 per cent in Q1, following the shooting up of lead prices as a result of the Russia-Ukraine war. While margins expanded to 13 and 15 per cent respectively in Q2 and Q3, it has again compressed a bit to 11.9 per cent in Q4, with lead prices hardening. The company expects lead prices to stabilise around the current $2,000 per tonne levels.

In September 2022, the company announced a backward integration plan with respect to plastic component for batteries, which would result in margin expansion of 75 to 100 bps for ARBL. That said, as the new energy business begins scaling up, margin pressures at the consolidated level could come into the picture until these operations achieve economies of scale.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.