Hindalco’s current valuation does leave investors with value on table, despite the stock being valued at 8.3 times EV/EBITDA. This is a 17 per cent premium to its historical range. Novelis, the wholly-owned US subsidiary of Hindalco, is in the midst of a $4.9-billion expansion plan and followed it up with an IPO announcement in US markets. We recommend that investors accumulate the stock on dips as the expansion progresses and macro-economic factors improve from the current state.

Novelis: Capital outlay and IPO

Novelis is the world’s largest aluminium producer based in the US that Hindalco acquired for $6 billion in 2007. The backward integrated producer uses 63 per cent recycled content to supply to beverage cans (47 per cent in FY24), automobiles (24 per cent) and speciality (25 per cent). The segment reported 12 per cent revenue decline in FY24 owing to high inventory at clients and lower realisations (9 per cent lower YoY).

But Novelis reported a 3 per cent EBITDA growth as EBITDA per tonne improved 7 per cent YoY. This, owing to a higher recycled content (200 bps improvement), lower cost of production and operating efficiency.

Novelis aims to expand facilities with $4.9-billion worth projects under construction. The central project is a $4.1-billion greenfield fully integrated plant in Bay Minette, US, that is expected to add 600 kt capacity (16 per cent addition) by FY27. Additionally, a $365-million automotive recycling centre in the US and $350-million debottlenecking projects in the US, Brazil and Asia are also planned.

The company management sees scope for growth in US markets. According to US official data, the US imported 5.5 million tonnes of aluminium (largely unwrought) in 2023, of which Canada accounts for half the amount, withChina, India and Russia also contributing significantly. In April, the US banned Russian-origin aluminium, which has driven prices of aluminium to $2,500 pertonne from $2,200 per tonne in early 2024. Considering the domestic import substitution, ESG-compliant status of Novelis’s new facility and a high recyclable sourcing, the incremental supply should find demand for Novelis.

China has ended 2023 with a deficit in aluminium supply despite weakness in construction and automobiles owing to excessive power costs. The rest of the world has witnessed weak demand and 3 per cent excess supply owing to slow recovery in global growth. Facing FMCG, auto and consumers, aluminium demand will pick up following any recovery in growth or any movement in interest rate softening.

Novelis IPO has been announced with a price band of $18-21 in the US, which values this Hindalco subsidiary at an enterprise value of $16.3 billion at the higher end. Hindalco, by divesting 8.6 per cent of shareholding (including possible oversubscription), should gather $9,000 crore from the IPO. At the current IPO price, Novelis’s existing business and expansion plans are valued at 8.72 times EV/EBITDA.

India business

Hindalco’s India business consists of aluminium (upstream and downstream) and copper segments. The aluminium business faced revenue decline of 2.5 per cent YoY in FY24 as realisations declined by 5 per cent but shipments increased by 2.5 per cent YoY. Similar to Novelis, EBITDA increased by 7.8 per cent YoY despite lower revenues owing to lower cost of production. The copper segment, driven by higher shipments (up 12 per cent YoY) and realisations (up 4 per cent YoY), is in the midst of demand revival.

Hindalco capital outlay for India targets a new alumina facility, power linkages and downstream value-added portfolio. In Phase-I, ₹6,000 crore will be invested in a 1,000 kt (50 per cent incremental capacity) in Odisha with agreement with State government for long-term supply of the requisite bauxite. A 150 MW power plant is also planned in the same facility.

Aluminium demand in India is expected to grow at a CAGR of 6-7 per cent in the next decade. Hindalco has a strong balance sheet with consolidated net debt to EBITDA at 1.2 times and India business at net cash position of ₹3,500 crore in March 2024. With IPO fund flows to Hindalco, the balance sheet is set to get even stronger to capture the growing demand. On the energy front, Chakla coal mine and Meenakshi coal mine, which are being developed, will add to the energy security of Hindalco’s India business. The company has reiterated that with growing energy security, including renewable energy, Hindalco will target more value-added downstream projects in the long run.

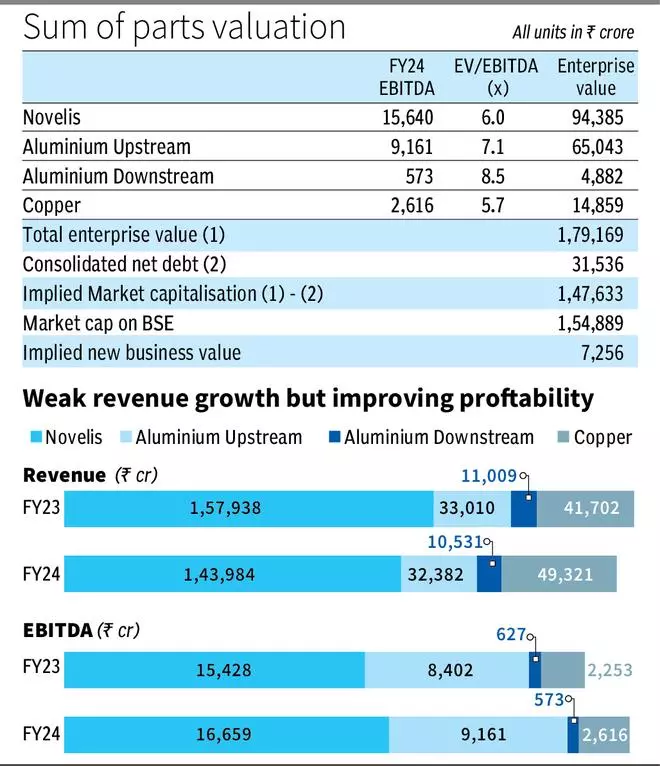

Sum of the parts

Hindalco (consolidated) is currently valued at ₹1.55 lakh crore. SOTP indicates that value of operating businesses is well captured in the current market capitalisation (see table). So any incremental value creation for Hindalco shareholders lies in potential for value creation from the ongoing $5 billion expansion plans for Novelis and in India business. Successful execution of these investment plans can add to shareholder value, which doesn’t appear to be adequately captured in the current market cap.

In the last decade, and through economic cycles, Hindalco traded at an average 7.1 times EV/EBITDA. Novelis valued at 6 times EV/EBITDA (adjusted for 15 per cent Holdco discount), aluminium downstream at 20 per cent premium for future growth, copper at 20 per cent discount for peak cycle discount and aluminium upstream in line — implies an EV of ₹1.8 lakh crore. Adjusted for net debt of ₹31,500 crore implies a market cap of ₹1.47 lakh crore with the difference being assigned to value of new ventures to the tune of ₹7,200 crore or less than $1 billion.

As the Bay Minnette projects near completion and global macros improve, the incremental value is likely to reflect in the stock price. Considering the scope for volatility related to elections in India and even in the US, and global trade wars, investors can build a margin of safety and accumulate the stock on dips.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.