The year gone by has been a volatile year for the cement industry, which can be seen in its share price movement. The Union Budget of 2022 emphasised infrastructure bringing optimism to its prospects. The general expectation was that the demand for cement will grow and the companies will register growth on both top and bottom lines. However, the geopolitical tension in Europe gave rise to an energy crisis causing a spike in energy costs. Under normal conditions, the energy and logistics costs are generally 20-25 per cent revenue for most cement companies, and are highly sensitive to crude and coal price volatility.

Thus contrary to expectations at the start of the year, while overall demand of the industry was decent enough, which also translated into revenue growth, the input cost rise was mainly driven by the increase in the energy prices, depleted profit margins for the companies. The rise in cement prices during the year was insufficient to compensate for the rise in costs.

Outperformers amidst challenges

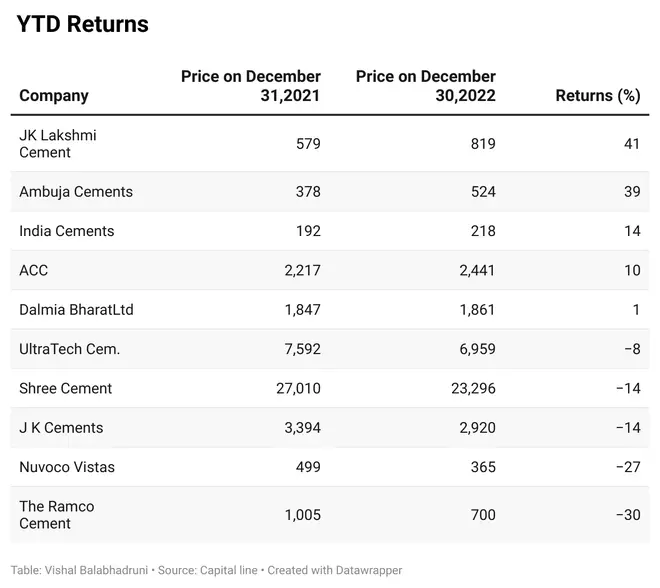

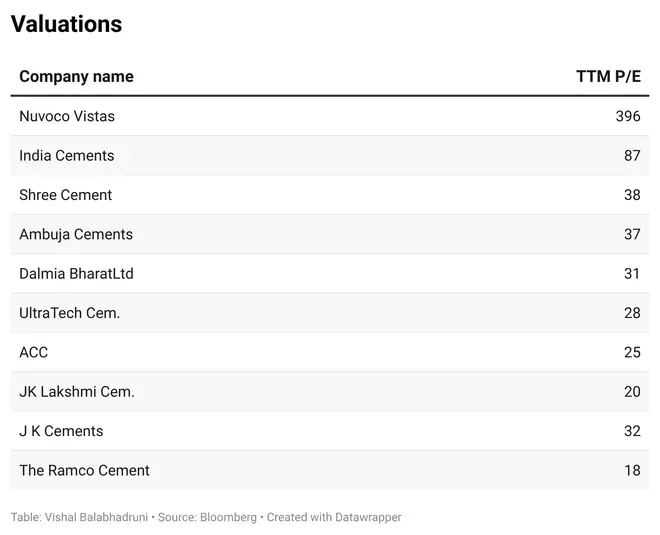

During 2022, most of the cement stocks delivered a negative or flat return, and the top 10 cement stocks (based on capacity) combined delivered average returns of -13.7 per cent. However, few companies bucked the trend. The stock of JK Lakshmi Cement outclassed all cement peers in 2022 with 41.43 per cent returns. The stock is currently trading at a TTM P/E of 19.68, while at the start of 2022, the TTM P/E was 15.72x. The positive performance in the stock seems to be due to better realisations aiding revenue growth, ongoing capex, and efforts like improving operating efficiency via more renewable energy/alternative fuel, as per a Anand Rathi report. Its cheaper valuation also made it a value stock within the cement sector at start of the 2022, a year in which value stocks outperformed.

The next best companies in terms of share price returns were Ambuja Cements and India Cements, which delivered 38.82 per cent and 14 per cent returns, respectively in 2022. During the year, Ambuja Cements and ACC were acquired from the Swiss major Holcim group by Adani in May 2022. Further, on September 16, 2022, Ambuja Cements announced plans to issue 47.47 crore warrants at ₹418.87 each to Harmonia Trade and Investment Limited (an Adani group entity) and raise ₹20,000 crore upon conversion of these warrants at a future date. Ambuja is currently trading at a TTM P/E of 37.49x.

India Cements delivered a YTD return of 13.66 per cent, the company slipped into losses in June 2022 and September 2022 quarters, majorly due to the spike in input cost. However, the stock recovered from its low of the year in the expectation of a turnaround, as indicated by the consensus estimates of its forward EPS.

Underperformers

The big boys of the industry - Ultratech cement, Shree cement delivered -8.34 per cent and -13.75 per cent returns, respectively, in 2022. They are now trading at a trailing twelve-month (TTM) P/E of 28.07x and 37.53x.

Ramco Cements had the weakest share price performance and delivered a YTD return of -30.33 per cent as on December 30, 2022, and is currently trading at a TTM P/E of 18.45x. The company faced cost pressures in Q2FY23 onwards, and it recorded an 84 per cent decline in net profit in H1 FY23 YoY. The power and fuel cost rose 135 per cent in H1 FY23 YoY and the logistics cost rose 34 per cent in H1 FY23 YoY.

Nuvoco Vistas has delivered a -26.88 per cent negative return YTD. In H1 FY23, the company managed to grow revenue by 28 per cent but reported a net loss of ₹72.83 crore against a net profit of ₹113.32 crore in H1 FY22. The power and fuel cost rose 166 per cent in H1 FY23 over H1 FY22 and logistics cost rose nearly 123 per cent.

JK Cements delivered a -13.96 per cent YTD return and is currently trading at a TTM P/E of 32x. In the H1 FY23, its net profit was reduced by 21 per cent Y-o-Y.

What lies ahead?

Energy prices are a major concern for the industry at present. However, off late, energy prices seem to be cooling off. According to a recent Emkay report, South African coal is currently trading in the range of $250-$300 per tonne, whereas in August-September 2022, it was trading at $350-$400 per tonne. The cost of imported petcoke has also come down to $180 per tonne from the recent high of around $200. This trend is positive for the industry as this can bring it back to better profitability. The upcoming Union budget will also be an important factor to watch out for, as it will impact the industry’s prospects over the next year. If the cooling off in raw material prices sustains, and the budget maintains the thrust on the infra sector, cement stocks may be in for better times in 2023. The only risk to watch out for would be the risk of any severe recession in the western world, which can put pressure on stock valuations.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.