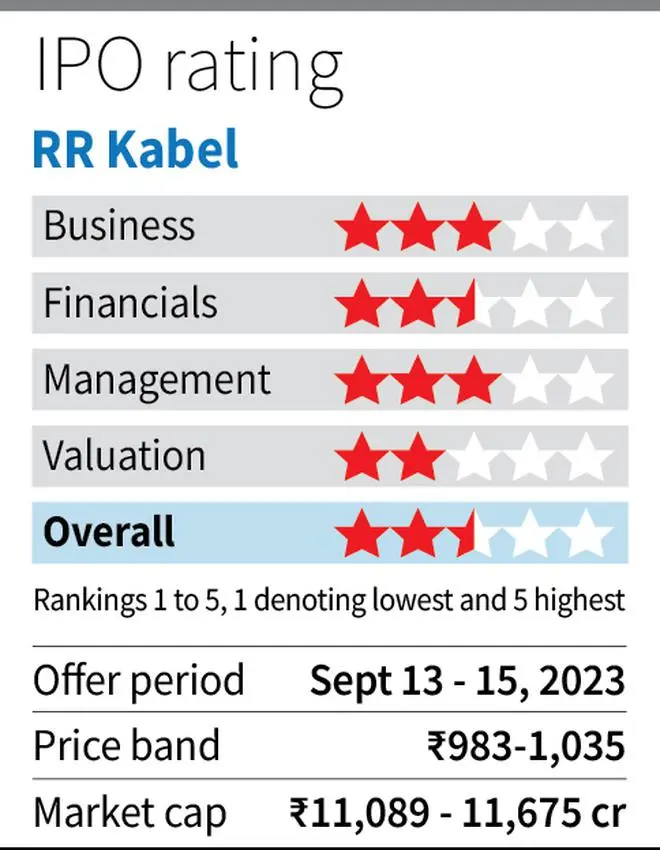

The initial public offering (IPO) of wire and cables manufacturing company RR Kabel opens for subscription today - September 13 - at a price band of ₹983-1035 and closes on September 15. The total offer is ₹1,964 crore, of which ₹180 crore is a fresh issue, while the rest is an offer-for-sale, wherein private equity firm TPG is selling stake. Of the ₹180 crore, ₹136 crore will be used for re/ pre-payment of debt, and the rest for general corporate purposes. Post-issue, the promoter’s shareholding will be around 62.8 per cent, from the current level of 66.4 per cent.

At the upper end of the price band, the company is valued at around ₹11,675 crore, which prices the RR Kabel stock at around 61 times its FY23 earnings. The company might be a play on the continuing shift to organised players, with increasing share of branded players, on account of the GST regime, as well as consumer awareness about safety and quality.

However, margin pressure, intense competition, and its pricey valuation call for a wait-and-watch approach. The shift to organised players has already played out with branded players accounting for a 72 per cent market share. Hence, investors need not subscribe to the issue now. An investment call can be taken later after assessing its performance as a listed company, and at better entry points.

Business

RR Kabel is involved in the business of selling consumer electrical products comprising wires and cables and fast moving electric goods (FMEG).

The wires and cables (W&C) segment contributes about 89 per cent of the company’s operating revenue. The segments include house wires, industrial wires, power cables and special cables. With a 72 per cent share of branded players in the segment, RR Kabel has market share of about 5 per cent. Under the FMEG segment (11 per cent of revenue), the company sells fans, lightings, switches and appliances. The customers comprise distributors, dealers, retailers, electricians, institutions, governmental authorities, and original equipment manufacturers.

The company’s customers are drawn from a range of industries such as real estate, infrastructure, automobiles, telecommunications, railways, textiles, pharmaceuticals, paints, cement and data centres. Further, the company earns nearly 10 per cent of its revenue through exports.

Typically, the company attempts to pass on a portion of changes in raw material price to customers. Copper, aluminium, galvanized iron, packing material, LS0H, master batch, solar compound, PVC compound and XLPE compound comprise the primary raw material. Of these, the company manufactures polyvinyl chloride compound, low-smoke zero halogen compound, cross-linked polythene compound and solar cable compound in-house. It purchases raw materials such as copper and aluminium (which account for an 82 per cent share of the total raw material cost) at market prices which are linked to prices on the London Metal Exchange, which are generally quoted in US dollars. The company hedges its foreign currency risk by entering into derivatives contracts. While the company doesn’t have a commodity hedging policy, it attempts to manage the risk by entering into agreements with suppliers, wherein they get a 30-45-day window to fix the price for the period, based on demand for their final products.

Financials and valuation

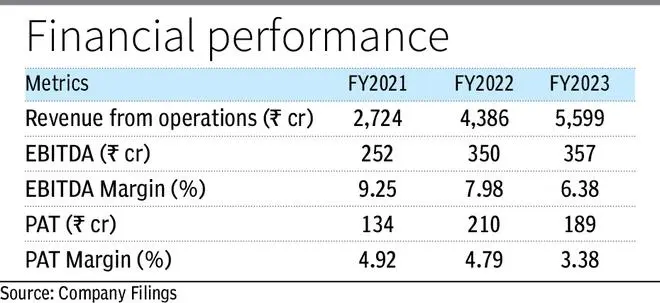

During FY21-23, RR Kabel has grown its operating revenue at a CAGR of around 40 per cent, which is higher than that of its peers, such as Polycab, Finolex Cables, Havells and KEI, which had a CAGR of around 27 per cent. Growth has been driven by higher sales volume in the W&C segment, inorganic growth in the FMEG segment, and improved realisations resulting from higher international prices of key raw materials such as copper and aluminum.

While revenue CAGR is on the higher side, it is not the same when EBITDA margins are considered. The company’s reported EBITDA has grown at a CAGR lower than revenue at around 19 per cent, and the EBITDA margin has fallen from around 9 per cent to 6.35 per cent, which is lower than that of a majority of its peers, who have been generating margins of 10-14 per cent. According to the management, this has been on account of lower capacities in the power cables space, higher marketing spends, and losses in its FMEG business due to increasing costs relating to setting up of distribution network.

Outlook

According to the management, the company has planned a capital expenditure of 500 crore combined for FY24 and FY25. Of this, around ₹475 crore will be used for capacity expansion of the W&C business, and the rest for the FMEG segment. As the capacity expansion takes place, the management expects better margins as economies of scale are realised.

According to a Technopak report, the market share of branded players in the W&C business has increased from about 60 per cent in FY2015 to 72 per cent in FY2023, which can further increase to 80 per cent by FY2027. While the share of branded players might increase, much of the penetration has already happened, and so the company’s growth will also depend on the the industry dynamics going forward.

Post-issue, the company’s valuation at P/E of around 61 times (FY23 earnings) appears high when compared to its peers who are present in the W&C business. Polycab, which is larger in terms of revenue, trades at a P/E of 62 times, while Finolex Cables, which is of a similar size as RR Kabel, trades at a P/E of 34 times. When compared to this, the IPO of RR Kabel is not priced attractively, especially considering its smaller size and lower margins. Further, while Havells trades at a PE of 82 times, its premium is due to its industry leadership, diversified business and superior margins.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.