The stock of India’s most valued company, Reliance Industries (RIL), after a decade-long underperformance — from 2007 to 2017 — has managed to treble over the last six years.

However, when you look at the stock on a three-year basis, RIL with 11 per cent CAGR returns (including the value of demerged Jio Financial Services), has underperformed Nifty 50 which has delivered CAGR returns of a little over 14 per cent in the same time period. This however is nothing to fret about. The stock of RIL has typically tended to underperform whenever the company has been in a heavy investment phase, something that it has embarked on in its green energy ventures.

With the stock still leaving some money on the table at current levels, long-term investors can accumulate it on dips for four reasons — one, reasonable valuations; two, being at pole position in India’s high-growth digital and retail business; three, potential for large-scale value creation, similar to its digital and retail forays, in the renewable energy space (not reflected in current valuations); four, stable O2C business.

Growth engines

The launch of Jio’s data services in 2016, maturation of the retail business and subsequent stake sales in FY21 were the key catalysts that drove the stock’s outperformance in the last six years. Although there has already been a significant re-rating in valuation the markets have assigned to both businesses, scope for further outperformance from these businesses remains, given the opportunity ahead.

Reliance Jio: For one, with Reliance Jio emerging as the largest telecom services company in what is largely a duopolistic market (given survival issues at Vodafone Idea) in India, the growth potential remains strong as 5G will drive advances over the next few years and new 5G enabled use cases will create guzzling growth in data consumption, providing scope for higher ARPUs. Reliance Jio has offerings across the spectrum of wireless, wireline/broadband, enterprise/cloud services and allied retail/enterprise digital offerings that make its services sticky for customers.

In such a scenario, its dominant position in telecom along with second player Bharti Airtel is likely well entrenched for the foreseeable future in India’s digital ecosystem. These factors position it advantageously to sustain or increase its operating margins in a growing industry.

Reliance Retail Ventures: From a modest 1,691 stores in FY14, the retail business has grown to 18,040 stores (and over 66 million square feet of retail space) by FY23. Reliance Retail is the largest player in the country in the organised retail segment, operating brick-and-mortar, e-commerce, cash and carry, B2C, and B2B formats across the retail supply chain. With a low 3 per cent share of the market, there is scope for huge expansion from the combination of market share gains and/in a high-growth market where the consumption theme is picking steam, driven by growth in per capita income.

For example, in the US, organised retail giant Walmart today has a little over 10 per cent share of the retail industry. While how exactly things will pan out in the Indian retail industry is out in the open, this can provide a perspective on the potential growth for Reliance Retail.

In recent years, Reliance Retail business has witnessed solid growth with FY21-23 revenue and EBITDA CAGR of 38 and 50 per cent respectively fuelled by a combination of store additions, acquisitions (totalling to $1.2 billion) and its phygital model with acquisitions such as Netmeds, Clovia being digital brands. Besides apparel, grocery and electronics, the company, through acquisitions, has gained foothold in newer segments such as pharmacy (Netmeds), fashion (Zivame, Clovia) and D2C (Urban ladder), which will drive growth in the medium term.

With dominance in digital and retail ecosystem and scope to enhance synergies across these, Reliance is strategically positioned to garner a good share of the consumer spending which will happen over the next decades with its consumer facing businesses.

O2C & E&P

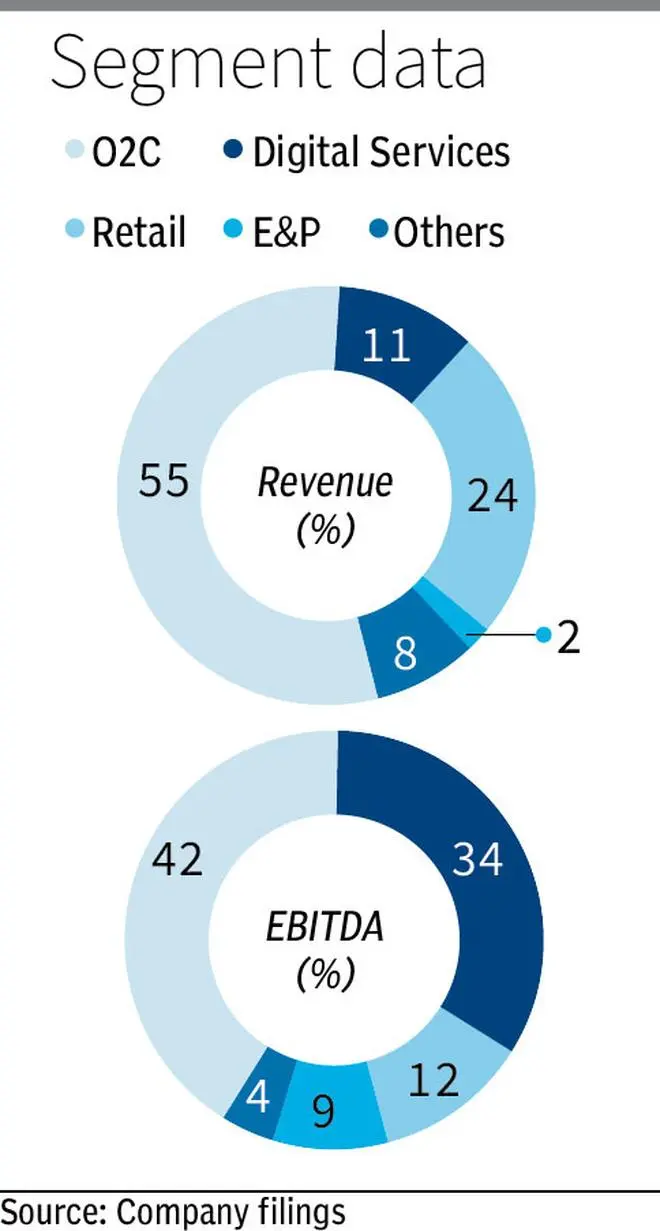

RIL’s traditional businesses — O2C and exploration (E&P) — still account for 45-50 per cent of RIL’s consolidated EBITDA.

Spanning expansive refining and petrochemicals business, the O2C business performance can be volatile depending on trends in crude oil prices and refining margins. In times of high crude oil prices, higher refining and petchem margins have helped the overall profitability. Similarly, there have been times when, due to falling crude prices, refining and petchem cracker have been on a falling spree, thereby adding to the pressure on the overall profit performance. Reliance’s O2C business has best-in-class margins and may not be comparable to Indian refiners, given the scale of operations, efficiencies and export focus.

Overall, while it remains a significant part of the company’s business, it will not get the same high valuation like RIL’s consumer facing businesses. In fact, based on value assigned to this segment by analysts, its overall contribution to RIL’s valuation has not changed much from around the $75 billion it was estimated to be valued at when stake sale talks with Saudi Aramco were ongoing in 2019. Scope for increase in value in the medium term can arise from the company’s expansion in the petrochemicals business.

The E&P business is small relative to overall size of Reliance. Analyst estimates for its value accounts for less than 10 per cent of overall RIL value.

Next big thing

Historically any business that RIL has put its weight behind has ended up being one of the largest players in the field and also managed to create a lot of shareholder wealth.

On these lines, RIL has identified green energy as its next growth opportunity. As the world moves away from conventional fossil-based energy sources, towards cleaner and sustainable energy sources, the company is looking to capitalise on the huge demand potential for renewable power anticipated over the next few decades.

The company has committed a whopping ₹75,000 crore investment into building a comprehensive green energy and green material ecosystem. At Jamnagar, it is building a green energy complex spread over 5,000 acres of land which, according to the company, will be among the largest integrated renewable energy manufacturing facilities globally. This will cost it ₹60,000 crore, while the balance ₹15,000 crore is being invested in partnerships, building future technologies, value chain to be able to build an integrated renewable energy ecosystem. The company has already made several investments in companies that are working on green energy technologies — such as battery technologies, solar cells/panels, clean mobility solutions, software tools for solar energy, etc.

While it’s up in the air as to whether green energy investments will reap same dividends as RIL’s telecom and retail forays, the good thing for investors is that market is hardly assigning any value to this business at current levels. Hence, there is scope for significant upside down the years from this business if the company repeats the success it has had in its other businesses.

Valuation

Reliance Industries currently trades at 24 times its trailing twelve-month earnings. While this is above RIL’s pre-Covid three-year average valuation of around 20 times, given growth delivered by telecom and retail businesses post Covid, there is scope for further re-rating.

SOTP: Reliance Retail Ventures, which is the flagship company, is currently valued at about $100 billion (₹8.3 lakh crore), based on recent transactions. RIL has an 83 per cent stake in it.

Reliance Jio, which is the other important segment of Reliance’s business, was valued at $63 billion back in 2020. Market assigned value is $80–90 billion range - 10 to 11x one-year forward EBITDA, which is not expensive. RIL has 67 per cent stake in it.

Adding the value of RIL’s stake in the above businesses and around $75 billion (conservative and assumes no change in value in last 5 years) for its O2C business, the enterprise value for Reliance works out to around $214 billion. This excludes value of its E&P business and its media businesses and some value in its monetisable real estate. This also assigns zero value for its green energy business. RIL has net debt of around $15 billion. Adjusted for debt, its valuation is around $200 billion, which matches its current market cap. Adding value of E&P, and high potential for large-scale value creation from green energy business, there is some money left on the table for long-term investors who can accumulate the stock on dips.

At a time when small and mid-cap stock valuations are trading at dizzying valuations, large caps like RIL may be safer bets for the long term.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.