Following the successful listing of Flair Writing Industries which now trades at a premium of 27 per cent to its IPO price, the IPO of DOMS Industries is open for subscription from December 13-15. Capital base expansion, established presence in pencils market and a wide distribution channel are positives for DOMS. But valuation seems to be a bit of a dampener. DOMS is coming at a valuation similar to Flair now.

However, Flair has an edge in margins and revenue growth prospects. We hence recommend that investors can wait for better entry points to take exposure to DOMS.

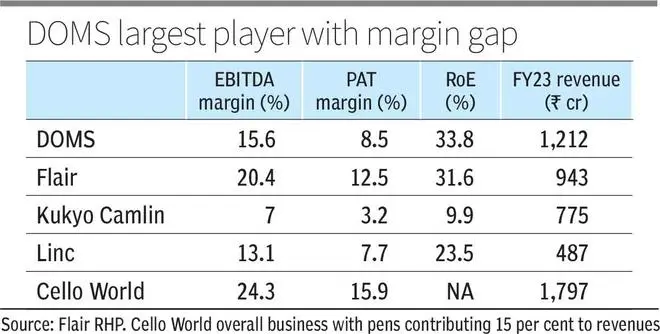

Strong established base

The company started operations in 1973 with manufacture of pencils and crayons. It was in 2005 that the DOMS brand of pencils were first marketed. Later in 2012, the company tied up with Italy-based listed MNC, F.I.L.A which was into manufacture of pencils, crayons and art works internationally. F.I.L.A is now a promoter entity along with the original promoter group. FILA owns 51 per cent prior to the issue and will retain 31 per cent shareholding post-issue as well, following the OFS (offer for sale) led by FILA stake sale. The company gained exposure in international markets with help from the strategic partnership with F.I.L.A. The company generated 19 per cent of H1FY24 revenues from exports, of which exports to FILA accounted for 11 per cent; 8 per cent were branded exports from DOMS.

The company now operates across segments with scholastic stationery, art materials and paper segments accounting for 46/26/10 per cent of H1FY24 revenues. Going by products across segments, DOMS has a leading market share in pencils which contribute 36 per cent to H1FY24 revenues and compass boxes (5 per cent).

Along with product breadth, the company also has a wide distribution reach. The company largely operates through exclusive super-stockist model with a minimum purchase quantity. The DOMS portfolio reaches 1.2 lakh retail touch points across 3,500 cities and towns.

Expansion plan

DOMS has a ₹450-crore expansion plan for fresh issue portion of the IPO proceeds. The current capacity is optimally utilised ranging from 85-98 per cent utilisation for top products in FY23, according to the RHP. The land for capital expansion, near the existing facilities, has been secured at a cost of ₹73 crore in FY23. Out of ₹350 crore from fresh issue, ₹280 crore will be used for expansion and the rest will be funded internally according to the company. The facility can be expected to contribute to revenues from FY26.

Comparison

On the margin front, Flair has a higher gross and EBITDA margin of 46/20 per cent in FY23 compared with DOMS’ 37/15 per cent. We assume specific product mix within the companies could be accounting for the difference. The higher margins could lend a margin of safety to Flair’s operations in any market volatility and provide a better return experience for investors over a long run.

Distribution reach is comparatively similar for both companies. The sales growth of 75 per cent CAGR for the two entities in the last two years, both owing to a Covid base, further strengthens the similar end market rationale. This should imply a similar growth runway for the two.

On the expansion front, DOMS is committing a higher capital to expansion compared with Flair, even adjusted for difference in toplines. With a similar asset turnover ratio of 3.5 times, DOMS’ ₹450-crore addition should be expected to double the topline by FY27 compared with 50 per cent addition to Flair’s topline expected by FY25. But Flair, with 65 per cent of new output (water bottles) committed to a OEM customer, has a higher revenue visibility comparatively. DOMS is expanding in writing instruments including pens which faces higher competition and higher branding costs.

At the time of the IPO, Flair was valued at 27 times and is now trading at 32 times, post the gains. DOMS is now valued at 32 times, but Flair gains a bit of an edge on financials.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.