Dr. Lal PathLabs (DLPL) is amongst the earliest organised players in the field of diagnostic labs. Owing to lower capital requirement for expansion, unorganised to organised shift, strong margin profile and increasing healthcare consumption, diagnostics players and hence, DLPL have traded at a premium, even before Covid. DLPL traded at 40 times one year forward earnings from July-2017 to February-2020. But since Covid, from a peak valuation of 86 times in September-2021 (192 per cent gain in stock price from February-2020) the stock now trades at 51 times after a 50 per cent price decline from the peak. This is still at a premium to earlier range. DLPL can sustain a mid-teens growth in top and bottom line, but current high valuation would require an 18-20 per cent growth. Incremental negatives such as heightened competition and post-Covid normalisation in operations can pressure the premium going forward as well. We recommend investors to stay away from the stock even after the sharp correction, till valuation moderates to 35-40 times earnings.

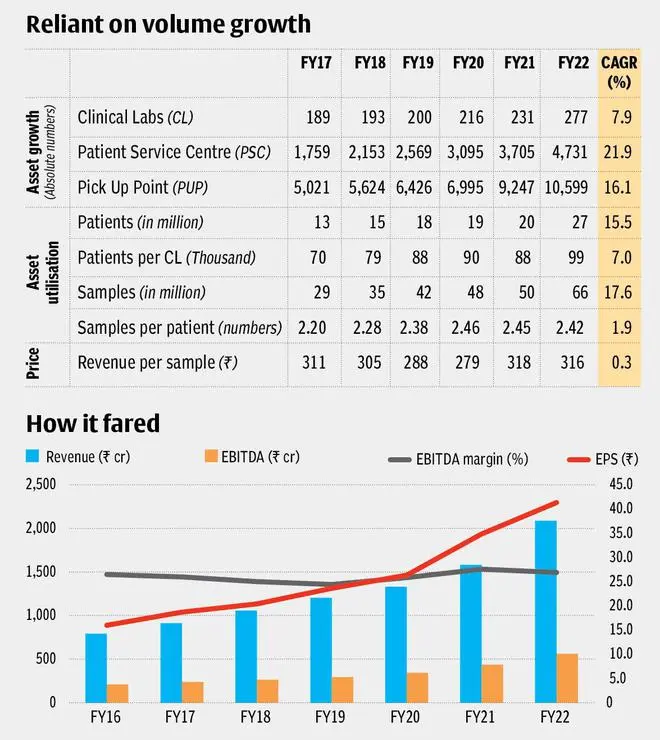

DLPL provides pathology and radiology tests for diagnostic purposes. The company’s hub and spoke model, common among all organised players, provides easy access to customers and adds new geographies to the company at a faster rate. The central labs (CL) (277 as on March 31, 2022) serve large volumes collected at smaller Patient Service Centres (PSCs numbering 4,731). They attend to regular tests and forward others to the CL along with even smaller PUPs - pick up points (10,599). Geographically, DLPL draws 34 per cent revenue from Delhi-NCR region alone with remaining contribution coming from rest of North 28 per cent, East 15 per cent, West 14 per cent and South India 7 per cent as of FY22.

Covid tail

Covid testing accounted for 20 per cent of revenues in the last two years. In the most recent fourth quarter, the contribution decreased to 16 per cent. While the general outlook is for complete halt as the virus recedes, the timeline is difficult to estimate. The labs can expect a longer tail contribution from travel, hospital, institutional and diagnostic Covid testing. But these revenues will be on a declining trend as testing mandates ease along with the severity of the pandemic.

Covid provided a strong bump up to pricing, which otherwise has been on secular decline in the industry. The overall average realisation for DLPL increased by 10 per cent because of Covid testing in FY22. As Covid volumes declines, the better pricing and the operational leverage from the large volumes will also recede. The spotlight will be back on non-covid tests which implies a declining realisation trend from the high base of last two years.

Base business

Diagnostics industry must rely on volumes for growth as pricing acts as one of the main product differentiators, the others being branding and convenience.

One of the levers of growth for DLPL has been the asset utilisation, measured by the patients per central labs or by the sample per patient. These two factors have had subpar growth in the last six years, as asset utilisation can have an upper limit on growth. DLPL is pitching its own, online sales channel and also tying up with other aggregators to increase utilisations.

With unorganised and organised market share at 50 and 17 per cent, scope for further organised expansion is abundant. DLPL is now eyeing franchisee-based expansion as well, but this may imply a trade-off between growth and value captured by the company. But its own physical expansion is now veered towards West and South, having achieved optimal presence in North and continuing to expand in East. DLPL made a ₹970 crore acquisition of Suburban Diagnostics, a Mumbai-centred brand with 38 labs and 177 collection centres. The southern expansion will not be a low hanging fruit for DLPL though, with fair presence of semi-organised locally active players.

Intense competition

The intense pricing competition in the sector was seemingly easing before the Covid, but the large pandemic opportunity has brought in more players with deeper pockets which should imply a longer period before a price hike can be considered. Organised diagnostics industry always had faced intense competition. New players like Tata 1mg, PharmEasy (through the acquisition of Thyrocare), Lupin Diagnostics have joined existing hospital and standalone operators. They are operating in market which is still largely dominated by unorganised players and hence will offer price and other differentiators to capture the market. But operating on price disruption, the impact will be similar for all players.

Valuation

DLPL reported revenue and earnings growth of 18 and 17 per cent in the last five years with flat EBITDA margins of 26 per cent. The last two years witnessed a hit on non-covid business, but covid contribution of 20 per cent more than made up on the revenue and also on realisations and operating leverage. DLPL has a strong balance sheet with net cash position.

Consensus estimates place earnings growth of 10 per cent in FY22-24 following Covid base of the last two years. In the longer term, even as DLPL exceeds historical growth in central labs (8 per cent CAGR in FY17-22) the lack of a pricing lever for growth will limit earnings growth to mid-teens at the higher end. With tougher regions, South and West, remaining for expansion, a high base and intense competition, the current valuation may not be justified even for this high growth diagnostic leader DLPL.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.