The Indian mutual fund industry has been experiencing one of its best phases over the past several years, especially post-Covid. Among the obvious beneficiaries are asset management companies themselves that house these mutual funds.

Among India’s top-10 mutual fund companies, UTI Asset Management Company (UTI AMC) is one of the oldest players in the space, with a long track record running to several decades.

Apart from mutual funds, the company also runs a much larger PMS (portfolio management service) business (which includes the employee provident fund organisation: EPFO) and is a major player in the national pension system (NPS) space as well. It also has international and alternatives segments.

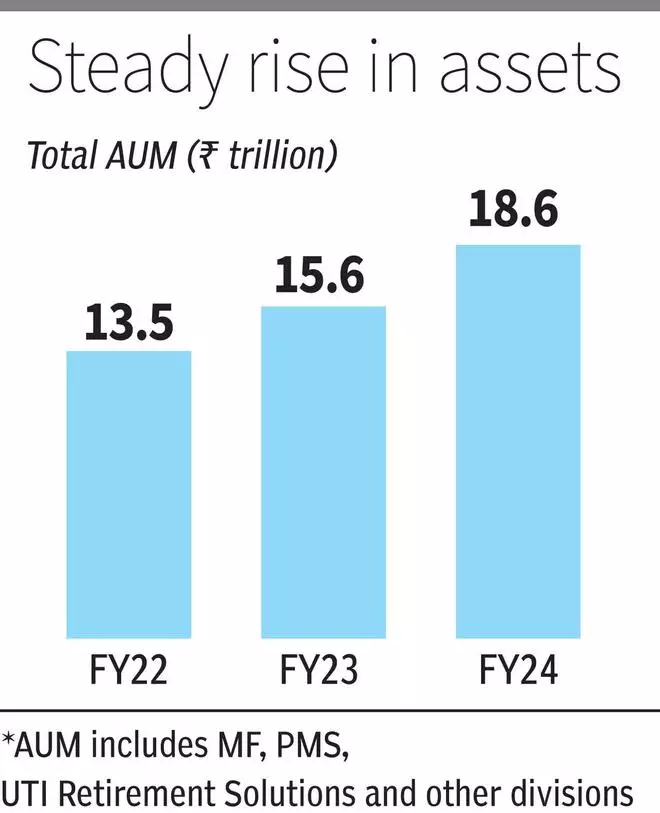

Collectively, UTI AMC manages ₹18.5 trillion as of March 2024.

Steady growth in mutual fund AUM, reasonable flows via the systematic investment plan (SIP) route and a healthy mix of asset classes spread across multiple avenues are key positives for the company.

In some segments such as hybrid and debt, the fund has done well, though many of the AMC’s equity funds have some catching up to do.

At ₹976, the stock trades at 16 times its per share earnings for FY24 and a little over 14 times its expected EPS for FY25. This is at a steep discount to HDFC AMC’s PE of 40 times and Nippon Life AMC’s 33 times based on FY24 earnings. When the market capitalisation to AUM ratio is taken, Nippon Life AMC’s figure is at about 7.1 per cent, and HDFC AMC’s is 13.1 per cent. When UTI AMC’s mutual fund AUM to its market capitalisation is taken, it is less than 4 per cent – it’s much lower if NPS and PMS assets are included.

UTI AMC’s valuations are thus at a steep discount to peers, even taking the company’s lower mutual fund AUM into account. Investors can buy the stock with a three-year perspective.

The company’s operating (EBIT) margins have always been comfortable at well in excess of 40 per cent.

There is also the added incentive of being a dividend yield stock at 2.3 per cent in FY24 (4 per cent if special dividend is considered).

In FY24, UTI AMC’s revenues rose 37 per cent over FY23 to ₹1,737 crore, while net profits increased 75 per cent to ₹766 crore. The figures include fair value changes, interest and dividend income and rental income. Excluding these, the revenue growth figure is 5 per cent, while the net profit growth is 8 per cent.

MFs, retirals and PMS

Market regulator SEBI has maintained a hawk’s eye on mutual fund expense ratios in recent years. Even so, many fund houses have still managed to expand their revenues and grow their assets strongly.

UTI AMC manages ₹2.9 trillion (up 21.8 per cent YoY) in mutual funds as of March 2024, with a market share of 5.37 per cent and it is the eighth largest fund house by AUM in India.

Its SIP assets have risen sharply by nearly 43 per cent from ₹21,509 crore in March 2023, to ₹30,747 crore as of March 2024. As much as 90 per cent of UTI AMC’s systematic investments book tends to stay for more than 10 years, and 95 per cent for more than five years. The industry average is less than 30 per cent.

UTI AMC has a large passive funds (ETFs and index funds) AUM. At ₹1.15 trillion as of March 2024, it is up 39.5 per cent YoY. It has a market share of 13.2 per cent, which places it among the top few in the industry.

The debt and hybrid fund categories have also grown at a healthy pace in the last one year.

The still low penetration of mutual funds in India compared to most other emerging and advanced nations, rapid digitisation resulting in ease of investments via online platforms and the rising incomes and financialisation of savings are factors that could give further thrust to asset growth.

Its PMS business, which includes EPFO, Coal mines provident fund, ESIC etc., manages a staggering ₹12.25 trillion as of March 2024, which is up nearly 17 per cent YoY.

With the thrust on employment creation, growth in EPFO enrolments and the increasing emphasis on investing in the markets for retiral funds to be able to cater to long-term needs of subscribers, this space is set for further expansion in the case of UTI AMC, as only a limited number is allowed and there is little competition.

Other growth areas

UTI Retirement Solutions, a subsidiary of the company, manages pension funds, notably the NPS. The division manages ₹3.02 trillion in assets as of March 2024 (up 25 per cent YoY). Since the public sector NPS is also managed by the subsidiary, it has a large 25.8 per cent share in NPS assets.

In view of the increasing thrust to NPS by the government, given the pension burden a defined pensions scheme imposes, there is ample scope for growth in the segment, which will benefit the company.

UTI International, another subsidiary, is a manager of offshore funds and has ₹27,645 crore in assets and is growing steadily.

Overall, UTI AMC has multiple growth areas outside the mutual funds business and is a resilient long-term player in the asset management and retiral businesses.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.