Public sector banks’ lending to the micro, small and medium enterprises (MSME) sector has galloped in the last 2-3 years.

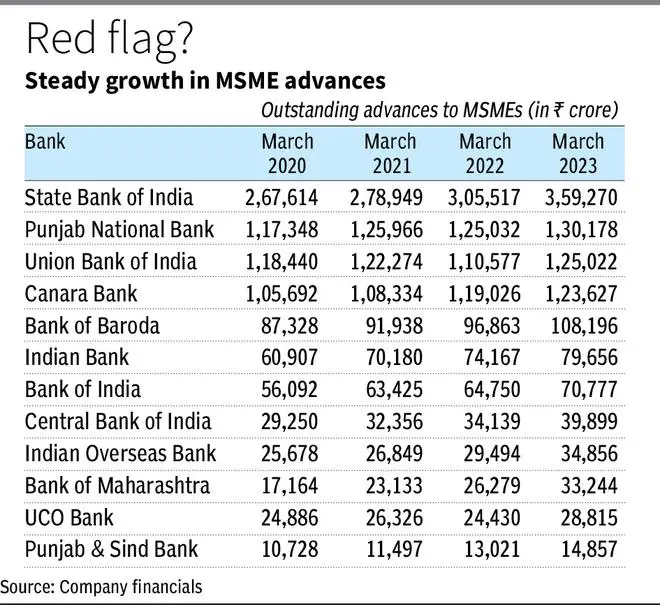

According to a businessline analysis of the 12 public sector banks, the outstanding MSME advances have jumped from ₹9.21-lakh crore at the end of FY20 to ₹11.48-lakh crore as of FY23. The growth in this loan book was 12 per cent in FY23.

Bad loans in the MSME book of PSBs is also growing in tandem as smaller businesses get impacted by slowing exports, withdrawal of dispensations provided during Covid and rising interest rates.

The country’s largest lender, State Bank of India, has the highest exposure to MSMEs with an outstanding loan book of ₹3.59-lakh crore as of March 2023. Punjab National Bank comes next with an outstanding MSME loan book of ₹1.30-lakh crore, followed by Union Bank of India (₹1.25-lakh crore).

Also read: Bank of Maharashtra’s advances to grow 1.5 times the banking industry average in FY24: Chief Rajeev

Within PSU banks, IOB has the highest share in total advances to MSMEs, at 20 per cent. The share of MSME advances for other PSBs is in the 13-19 per cent range.

NPA concern

While the exposure to MSMEs helped banks diversify their loan books, these loans are more vulnerable. Geopolitical shocks and global slowdown which impact exports have a debilitating impact on the smaller businesses. Growing repayment obligation in a rising rate cycle can also hurt these companies more.

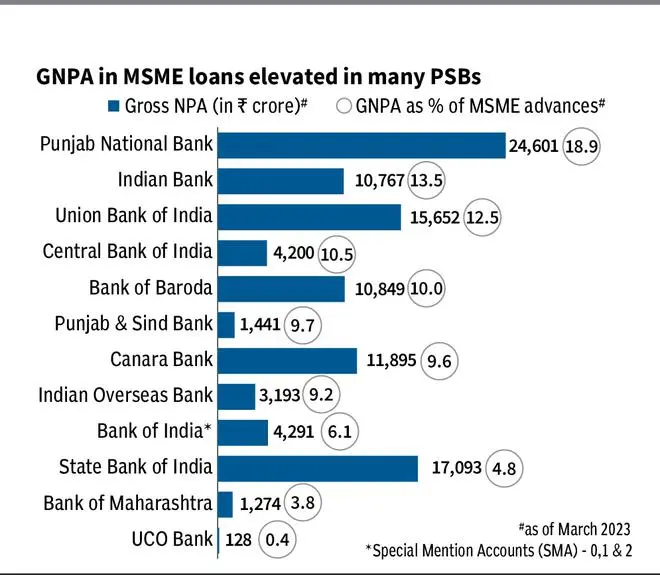

Many PSBs are still grappling with high gross non-performing assets (GNPA) ratio in the MSME loan book. For instance, GNPA in MSME loans of PNB stood at ₹24,601 crore, or 18.9 per cent of its MSME advances towards the end of March 2023. Indian Bank, Union Bank of India, Central Bank of India and Bank of Baroda have recorded over 10 per cent gross NPA in their MSME advances.

“As compared to their corporate and retail loan books, NPAs in MSME book is higher for public sector banks,” said Krishnan Sitaraman, Senior Director and Chief Ratings Officer, Crisil Ratings Ltd.

“MSME accounts, given their relatively higher vulnerability and lower balance sheet strength compared with larger corporates, did face heightened challenges during the pandemic,” Sitaraman said.

Also read: Bank of Maharashtra top performer in NPA management during FY23

Aashay Choksey, Vice-President & Sector Head-Financial Sector Ratings, ICRA Ltd., said various regulatory interventions during the pandemic helped prevent a severe weakening in asset quality levels across segments including MSMEs.

Citing an RBI study, Choksey said NPA levels of MSME borrowers who availed one of the supportive measures (Emergency Credit Line Guarantee Scheme) fared much better in asset quality than those eligible borrowers who chose not to avail it. “As these interventions wane off, the NPA levels in the segment could be a challenge,” he added.

Sitaraman said with the economy reviving and the cash flows normalising, the health of MSMEs is again improving. “But we will need to monitor these accounts closely as stresses due to factors like export slowdown, higher input costs and elevated interest rates can impact them to a greater extent,” he added.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.