India’s natural gas consumption is expected to grow 6-7 per cent Y-o-Y in the current financial year aided by higher domestic gas availability and softening international spot liquefied natural gas (LNG) prices.

India consumed 158.2 million standard cubic metres per day (MSCMD) of natural gas in FY23, down 2.5 per cent Y-o-Y. LNG consumption fell 13.35 per cent Y-o-Y to 71.4 MSCMD, while imports fell 15.18 per cent Y-o-Y to 72.1 MSCMD in FY23.

Akin to global gas markets, Indian gas utilities sector, after facing headwinds such as significant price volatility and availability of LNG over the last two years, is now returning to a tentative state of normalcy, ratings agency ICRA said.

“Gas consumption in India is expected to grow by 6-7 per cent Y-o-Y in FY24 over a low base, supported by softer LNG prices and an uptick in domestic gas production,” ICRA Senior VP & Group Head (Corporate Ratings) Sabyasachi Majumdar said.

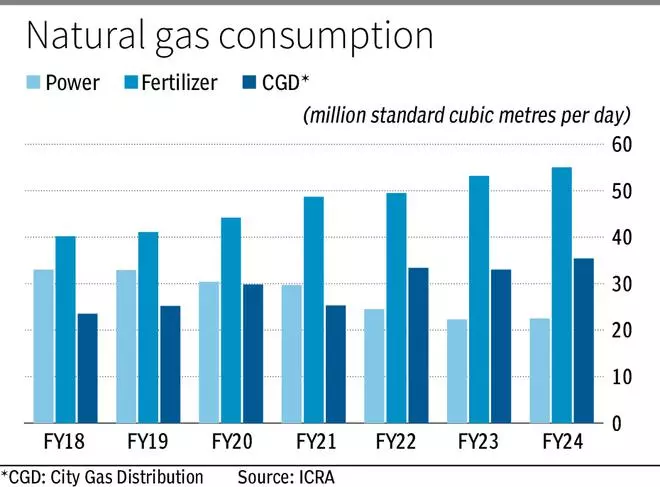

Pointing out that fertilizer sector will continue to remain the largest consumer of gas, he said this is supported a ramp-up of new fertilizer plants that were commissioned in H2 FY23.

The demand from city gas distribution (CGD) is underpinned by the compressed natural gas (CNG) segment, which remains robust owing to the strong economic advantage over alternate fuels, a testament of which is the strong uptick in CNG vehicle sales in the last couple of years, Majumdar added.

LNG prices

ICRA said that global LNG prices moderated in calendar year 2023 after achieving life-time highs in CY2022, aided by changes in demand patterns across the key consuming nations.

“LNG demand from China has been subdued amid an economic slowdown, rising pipeline flows from Russia, and increasing use of coal. The EU demand stabilised after the initial peak, owing to mild winters, austerity measures, and a weak economic environment,” it added.

The demand from Japan and South Korea was also tepid owing to their increased focus on the use of renewables and nuclear power. On the other hand, the US domestic demand has also witnessed subdued growth, and with healthy gas inventory levels, the Henry Hub prices have moderated.

On global LNG prices outlook in short term, ICRA’s Senior VP and Co-Group Head (Corporate Ratings) Prashant Vasisht said: “Global LNG prices are expected to not increase much from the current levels as the EU has ample storage and above the historical levels for this time of the year.”

South Korea and Japan consumption is expected to decline or stay stable due to increasing reliance on nuclear power. Although China’s consumption is expected to increase, the same is mostly tied up in term contracts. Lastly, five new liquefaction terminals are starting up within CY2023 so markets are expected to be well supplied, he added.

However, Majumdar cautioned that event risks persist, like an extended labour strike in Australian LNG facilities and a colder-than-expected winter in the northern hemisphere, which could result in volatility in the spot prices.

Given the lack of investments in the LNG projects over the past few years, incremental availability of LNG will be capped with major capacity additions expected in FY2025-26, he added.

Meanwhile, structural changes are underway on the demand front, such as the increasing focus of the EU on renewable energy, a shift towards coal usage by China, and increasing reliance on nuclear power by Japan and South Korea. The LNG offtake by South Asian countries remains highly price sensitive.

Domestic demand

The gas offtake by the domestic market is supported by softening LNG prices, uptick in domestic gas supplies, and a regulatory push by the government, ICRA said.

Gas production is projected to witness healthy growth in FY24, primarily from the Krishna-Godavari Basin, which is likely to keep reliance on LNG in check. CGD and fertiliser sectors will continue to drive the demand growth owing to favourable policy support.

ICRA expects demand from the industrial sector to witness a healthy uptick amid soft LNG prices and increasing domestic gas production.

CGD benefitted from implementation of the Kirit Parikh Committee recommendations in April 2023, resulting in lowering of domestic gas prices, thereby improving the cost economics for CNG and PNG (d) vis-à-vis alternate fuels, it added.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.