Incessant pull out of money by foreigners, gloomy global situation and over valuation concerns led to Indian markets cracking 9 per cent in the first half of this calendar year. But the month of July was different, with the Sensex climbing up by 4,500 points or 8.5 per cent. Is a sustained rebound on the cards this year?

Tracking swings

Since 1980, there have been 8 instances out of 15 when Sensex marked a turnaround in July-December after slipping in the first half i.e., January-June. While at a probability level this is a fifty-fifty chance, there is growing belief that if inflation is brought control and corporate earnings continue to grow, the Indian stock market will regain its mojo in no time.

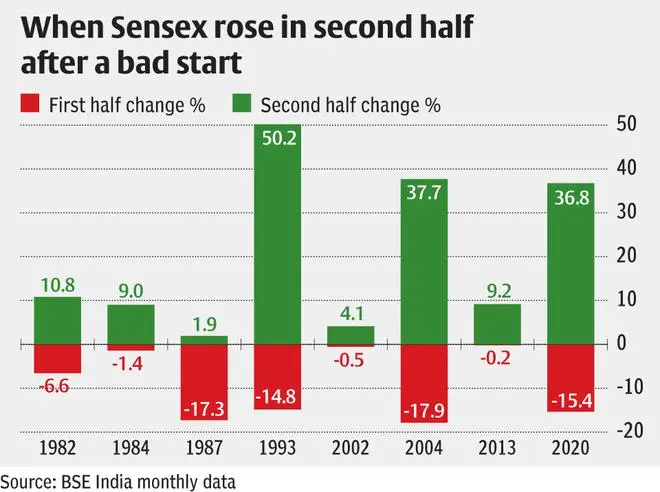

Indian stock markets have historically seen many turnarounds in the second half after a negative first half in terms of return. Even if we ignore early years such as 1982, 1984 and 1987, investors saw a turnabout in 1993, 2002, 2004, 2013 or as recently as 2020 (see table), albeit under different macro-economic conditions.

Truth be told, markets are driven by sentiments, and sentiments can change swiftly. In 1993 the Harshad Mehta scandal roiled Indian shares, but after slipping about 15 per cent in Jan-Jun, markets zoomed over 50 per cent in Jul-Dec period. In 2004, the first half was marked by political uncertainty following national elections and markets tanked 18 per cent but the second half brought steadiness and equities skyrocketed 37 per cent in the next six months.

In the Covid-ravaged 2020, too, it was all gloom and doom in the first half, before markets realised that it was not the end of the world because of the virus. Consequently, stocks saw massive buying and markets — after declining over 15 per cent in the first half — sprang back 36 per cent in the second part of the calendar year.

Waiting for signals

The 9 per cent crash in January-June of 2022, if we exclude 2020, is actually the first time that markets posted negative returns in first half since 2013. A multi-year sustained upward march and the sharp rise since 2020 made investors edgy.

While the Indian economy in 2022 is well placed for the long-term, it has been facing other near-term macro headwinds such as weak rupee and the Ukraine war aggravating the rise in commodity prices. The rising interest rates for the time being do hurt, but at this point, experts are neither projecting a slowdown in domestic equity flows or in economic growth.

Says Sanjay Chawla, Head of Research and Strategist, Emkay Global: “Global growth outlook is weakening; India is resilient in relative terms and is a major outlier. Inflation is manageable in India, and not out of control; expect terminal/peak repo rate below 6 per cent in Q4FY23.”

In a BofA Global Research report, economists have alluded to the possibility of inflation peaking in India and the Monetary Policy Committee (MPC) acknowledging that pretty soon.

From fundamentals standpoint too, domestic markets are not expensive. Nifty’s one-year forward P/E is at 17.4 times, which is similar to its 10-year average.

A sustainable rally from here on depends on tapering of FPI outflows. After selling over ₹2.5-lakh crore worth Indian stocks between October 2021 (when markets peaked) to June 2022, things are looking up. In July, for instance, FPIs were net buyers of equities worth nearly ₹5,000 crore, per NSDL data. This was the first time in 10 months that FPIs were net buyers. If the trend holds, the second half picture could be markedly different.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.