When it comes to fintech and markets, there are quite a few things that India ranks high in. One amongst these is the volumes in derivative trading. As per recent NSE data, the total derivatives turnover (futures and options premium combined) in the current financial year so far is at ₹3,28,88,25,030 crore (Yes, you read it right!). This is nearly two times that of FY22 turnover.

Within derivatives trading, Option trading, especially the index options, is hitting new highs as the number of contracts traded in the current financial year has nearly doubled compared to the previous one — 34.7 billion index option contracts were traded in FY23 as against last year’s 17.6 billion. So, it does appear that this is quite popular amongst traders.

However, the important thing to note here is this — while anyone can trade options, making money is not easy. In our Big Story published on October 9, 2022, we stressed the importance of understanding how options as a product is different from a futures contract or equity, the pricing mechanism, the concept of time value and volatility, etc.

In continuation of that, we discuss here how to set up an options strategy. But before that, the starting point is to form a view not just with respect to the direction of the next possible price swing of the underlying stock/index, but also on volatility.

Trend and volatility

Since there is a fundamental difference right at the pricing level in options, traders should tweak their approach accordingly. Typically, you buy or sell based on the expectation of the direction in which a security will possibly move in the future, which can be one day, one month or even longer. When it comes to options, you should also forecast how the volatility is going to be because volatility plays a considerable role in option pricing and will eventually determine your profit or loss.

To predict the trend, technical analysis or a combination of technical and fundamental analysis can be more beneficial, as options are generally short-term trades. For volatility, one can use India VIX as a proxy. For stock-level data, one can opt for the option chain of that stock which you can find on the NSE website. However, do note, this requires regular tracking to know the characteristics of a particular asset. Commonly, the volatility can go up ahead of a data release or a result announcement. There are traders who use statistical concepts to predict the direction and volatility.

Many small wins instead of one big win

In general, trading a plain vanilla option may appear like the simplest thing to do. When you are bullish on an underlying security you can buy a call option and if you believe the price of a security is set to fall, you can buy a put option on it. Although it sounds very simple, volatility can play spoilsport. Many a time, when the price of underlying goes up/down, the call/put option price remains the same. It will be a case of your view turning out right, but of no benefit to you.

Thus, when it comes to options, implementing a well thought-out strategy based on risk/reward or pay-offs analysis, with adequate risk management, can work out well in the long term. The objective, when it comes to options trading, must be to have many small wins, rather than one big win.

Once you form a view on trend and volatility, it becomes easy for you to shortlist the type of strategy that is best suited to the prevailing market conditions. Given that there are innumerable ways in which one can play in the derivatives segment, here we have focussed only on a few important strategies that are popular among option traders.

Moderately bullish

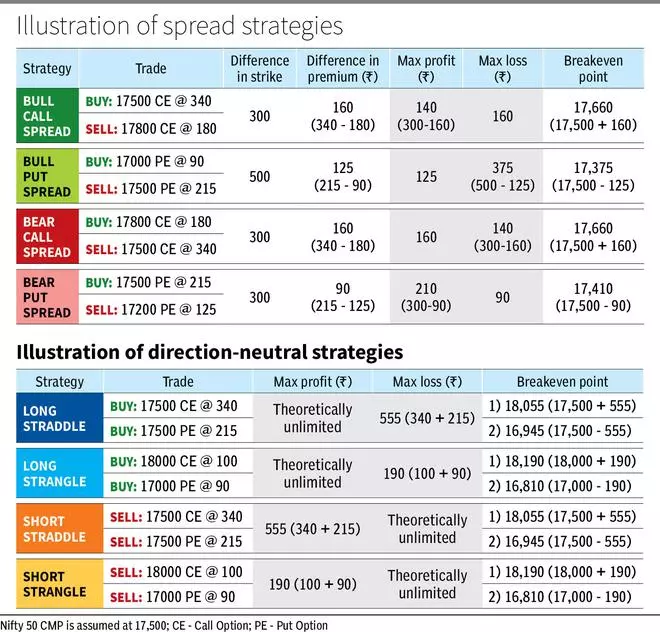

There will be times when you expect an asset to move up, but the upside potential is limited. This may be because of technical reasons, like the stock facing a strong resistance above or a fundamental reason which you believe can only lift the stock to some extent. In this scenario, one can opt for bull call spread or bull put spread.

Bull call spread: This is a two-legged strategy consisting of one long call with lower strike price and one short call with higher strike price. The long leg will usually be an at-the-money (ATM) strike and the short leg, an out-of-the-money (OTM) strike, can be the one just above the resistance level that you think will cap the upside. This is a net debit strategy i.e., net outflow at initiation.

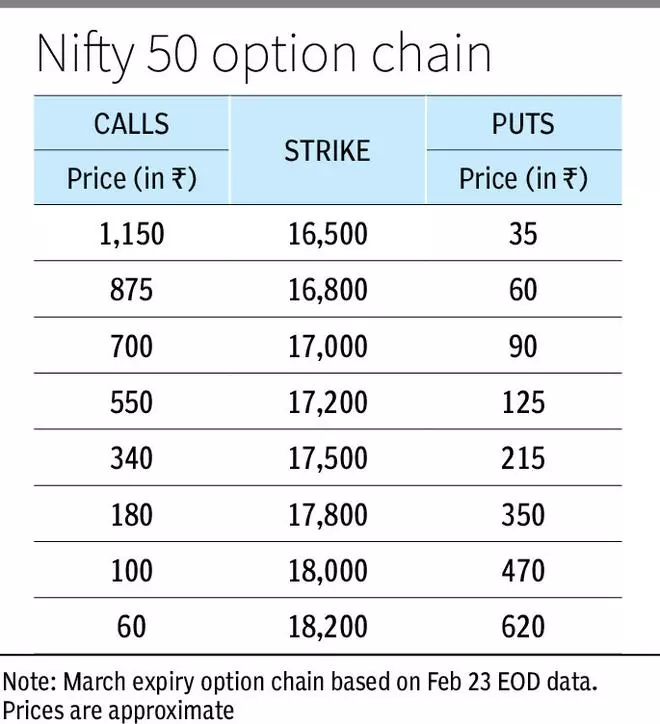

Find the table for examples for all strategies. Refer the option chain for the strike and the corresponding price of the options. We’ve taken March expiry Nifty 50 option chain based on February 23rd EOD data. Note that prices are approximate.

Bull put spread: A two-legged strategy where you sell a higher strike put and simultaneously buy a lower strike put. The short leg can be either in-the-money (ITM) or ATM option whereas the long leg is an OTM put. This is a net credit strategy i.e., net inflow at initiation.

Moderately bearish

Like a rally with limited potential, sometimes we might face a situation where the stock might see a temporary fall in price — for instance, a corrective decline within a broader uptrend. Such moves can be capitalised by strategies like bear call spread and bear put spread.

Bear call spread: Involves two call options like bull call spread. But here, the lower strike i.e., ATM/ITM call will be sold and simultaneously an OTM call will be purchased. Thus, a net credit strategy.

Bear put spread: Constructed by buying an ITM or ATM put option and at the same time selling an OTM put contract. This strategy will result in net debit.

Note that for all the spread strategies discussed above, the underlying, the expiration date and number of options i.e., lots, should be the same.

Volatility explosion

Certain events or data are sure to create an impact on the market. Be it a macroeconomic/geopolitical event or a stock-specific event like results, they can have a significant impact on prices at least in the short term, shooting up the volatility which, in turn, affects the option prices.

However, we may be unsure of how the markets will react to the latest information or data. So, in a situation where we know there will be a large move but the probability of moving up or down is equal, long straddle and long strangle can be the go-to method. Here, you are directionally neutral but long on volatility.

Long straddle: When you simultaneously buy the same number of ATM call and put options of the same underlying, same strike and same expiry, it is called a long straddle. The strategy will be profitable if the underlying sees a considerable move in either direction. This is a net debit strategy and notably, there are two breakeven points.

Long strangle: While both legs are longs, unlike straddle, the strike price of call and put option are not the same. Here, you buy one OTM call and one OTM put at the same time. The options will have the same underlying, same expiration date and same number of lots. You will end up profitable if the underlying asset trends in either direction. It results in net debit and has two breakeven points

Compared to straddle, strangle costs less and so is less exposed to time decay. However, in strangle, the breakeven points are farther and require much larger moves to be profitable. For example, post the 2004 election results, Nifty hit the lower circuit and post 2009 election results Nifty hit the upper circuit. Thus, in both instances, although the directions were different in these cases, the same strategy would have been highly profitable.

The biggest risk for these two set-ups is consolidation because a sideways movement can lower the volatility, increasing the time decay. Since both the legs are longs, time value loss can be higher compared to spread strategies discussed earlier.

Volatility implosion

Like price, volatility will also go up and down depending on the overall expectations of the market participants. But unlike the price of an asset, which can be eternally appreciating with some intermittent corrections, volatility is not ever increasing.

If a piece of news or data release becomes a non-event, the underlying asset might start consolidating. Consequently, the volatility might implode i.e., decrease drastically. If you are holding a long position on options, you are likely to face considerable losses as the premium swiftly falls.

Another example is the situation where you think the security has reacted to the latest piece of information to the fullest. This can also be statistically concluded. Suppose a stock rallied post the announcement of a better-than-expected result and reached 2 Standard Deviations (SDs) level. Statistically, 95 per cent of the values lie within 2 SDs and so, the probability of a rally above 2 SD is less. Also, the price may not fall as short sellers might stay away because the stock has posted good results. Here, the price might start moving sideways, leading to a drop in volatility. During such scenarios, traders can implement short strangle and short straddle which are neutral in direction but short on volatility.

Short straddle: Implemented by simultaneously selling ATM call and put options of the same underlying, same strike, same expiry, and same quantity. So, you will be a net receiver of the premium i.e., a net credit strategy with two breakeven points.

Short strangle: This strategy is constructed by selling an OTM call and an OTM put at once. Therefore, you will receive net credit to the tune of the premium of both the options.

These strategies will not work when the underlying is trending. There is also a high degree of risk as you hold only short positions. For example, after you execute a short straddle/strangle, if the security starts trending, the losses will keep on increasing to the level up to which it moves on either side beyond the breakeven price.

Therefore, traders should keep stop-loss for both the legs. Alternatively, it can be hedged by going long in OTM options. Such strategies are multi-legged ones which we will discuss later.

A word of caution

According to a study by market regulator SEBI (Securities and Exchange Board of India), 9 out of 10 derivative traders lose money. The rise of discount broking and technological advancements has enabled anyone to start options trading with ease. But one should understand the risk involved. The common misconception is that buying options is easy and cheap. While operationally it certainly is a breeze, traders generally forget the larger picture. They keep on buying options as the risk is ‘small’. However, over a period of time, it could be very late before you realise that you have made many numbers of small losses, creating a large hole in your capital. So, one should always be aware of what he/she is doing, the amount of risk taken per trade as a percentage of overall capital, what is the reward for the risk that you take, etc.

Always protect the downside by using a stop-loss or a hedge, try to use a separate account for options trading so that you can measure your performance precisely with respect to options. This way you can also ensure your risk is only limited capital tied to that account. Always try to understand the reason behind a loss, do not take emotional decisions, do not attempt to make up for the loss by trading bigger lots, if you are profitable see whether it is because of the same reason that you predicated or for some other reasons. Traders must have an entry and exit strategy. The larger point is, anyone can trade options but to be profitable there should be a systematic way in trading and always strive to reduce the risk per unit of reward.

If you can’t follow these rules, options trading is not for you.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.