“You either die a hero or live long enough to see yourself become the villain.” This striking quote from the Dark Knight sums up the pandemic-driven tech boom. From being the hero sector for investors and employees, having got stretched beyond measure, it is now turning out to be the villain with record wealth destruction and job layoffs.

Latest to join this club is Accenture with its shocking announcement last week that it plans to cut 19,000 jobs. This is a news that may need to viewed as a harbinger of more pain for investors in Indian IT stocks, especially given the stark contrast in their valuations when compared with global tech players.

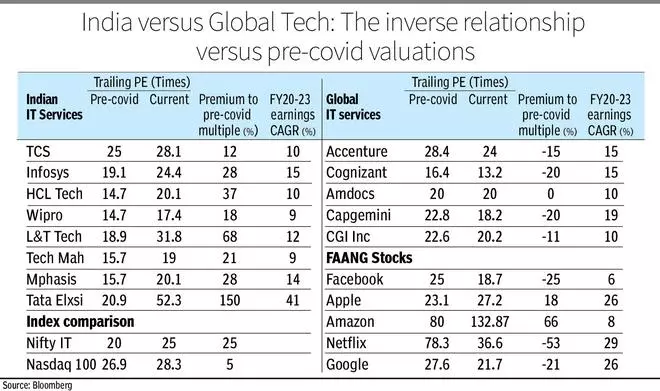

Premium to pre-Covid valuations

Globally, tech stocks in most cases have been routed. Big and small are trading on par or at discounts to pre-Covid valuations. For example, Accenture is trading at a 15 per cent discount to its valuations just before the pandemic struck. Cognizant Technology Solutions is trading at a 20 per cent discount. However, in stark contrast, Indian IT services companies with businesses similar to these global counterparts are trading at sizeable premium to pre-Covid valuations. While Indian tech stocks too have corrected, global tech has corrected more. The relative resilience in domestic tech stocks has been quite remarkable. But can it sustain?

The earnings growth of many of the global tech companies has been on par to better versus Indian tech companies. For example, Accenture’s FY20-23 earnings CAGR is at 15 per cent, beating close counterpart TCS’ earnings CAGR of 10 per cent.

At the global level, there are a few stocks like Apple and Amazon that are trading at premium to pre-Covid valuations. But these appear more like outliers rather than the norm.

At a broader level, the tech-heavy Nasdaq 100 index is trading at 5 per cent premium to its pre-Covid levels, while Nifty IT is trading at a significant 25 per cent premium.

Who is right? Was it the investors who valued Indian tech stocks pre-Covid, or the ones holding on to the stocks now? This a battle that the bulls and bears have to sort out over the next few months, but it would be reasonable to conclude that fundamentals appear to favour the bears. Further, the more one pays for the same asset today, the less returns one can reap in the future.

Resilience to get tested

The trifecta of impact of global slowdown (as can be inferred from Accenture job cuts), a banking crisis (one of the biggest clients for technology companies) and higher interest rates can continue to pressurise domestic tech stocks. That Nifty IT has been one of the worst underperformers in domestic markets over the last year, may not be enough to stall the pain.

While it cannot be said with certainty at what valuation levels the stocks can bottom, it is more probable that given the premium valuations Indian IT stocks can remain an underperformer vis-à-vis Nifty 50 as well as global tech. The rebound and recovery that many who locked into the sector prior to January 2022 peak in Nifty IT would have been hoping for, may not be forthcoming right now.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.