Last year, in our BL Portfolio edition dated June 6, we had recommended a hold onHCL Technologies for long-term investors when the stock was trading at ₹937. While we were cautious on the IT sector in general due to stretched valuations, we had a relatively positive view on HCL Technologies (HCL) given its comparable performance with other Tier 1 peers (TCS, Infosys and Wipro), and yet trading at a discounted valuation. This offered relatively better margin of safety vs peers.

While the stock is trading at ₹924.85 now, including dividends, it has returned around 5 per cent in this period, marginally outperforming the Nifty IT Index. With the headwind of economic slowdown in key geographies that Indian IT derives most of its revenues from (US and Europe), driven by hawkish central banks and impact of geopolitical issues (energy crisis in Europe), risk-reward remains unfavourable for most companies in the Indian IT space at current valuations. However, HCL Technologies, trading at one-year forward PE of 16.9 times, EV/FCF of around 19 times and a trailing dividend yield of 5 per cent (best amongst peers), appears to be an outlier in this aspect, and continues to offer better margins of safety as compared to other companies in the sector.

We now recommend long-term investors to accumulate the stock on dips. Given its position as one of the leading IT services companies globally and its well-established track record, its valuations are not expensive at an absolute level and its dividend yield is attractive. It also has a well-entrenched position and scale of operations to capitalise on the multi-year global digital transformation cycle.

However given the headwinds mentioned above, the probability is higher that the stock dips lower before moving up. Globally, tech stocks have been and are expected to remain under pressure for a while. The probability is low that Indian tech companies can buck this trend. Another factor that is likely to cause volatility in shares is continuing margin pressures in current quarter and next, due to higher salaries, subcontracting costs and attrition. Hence accumulating on dips over the next few months can be a better strategy.

Business & recent performance

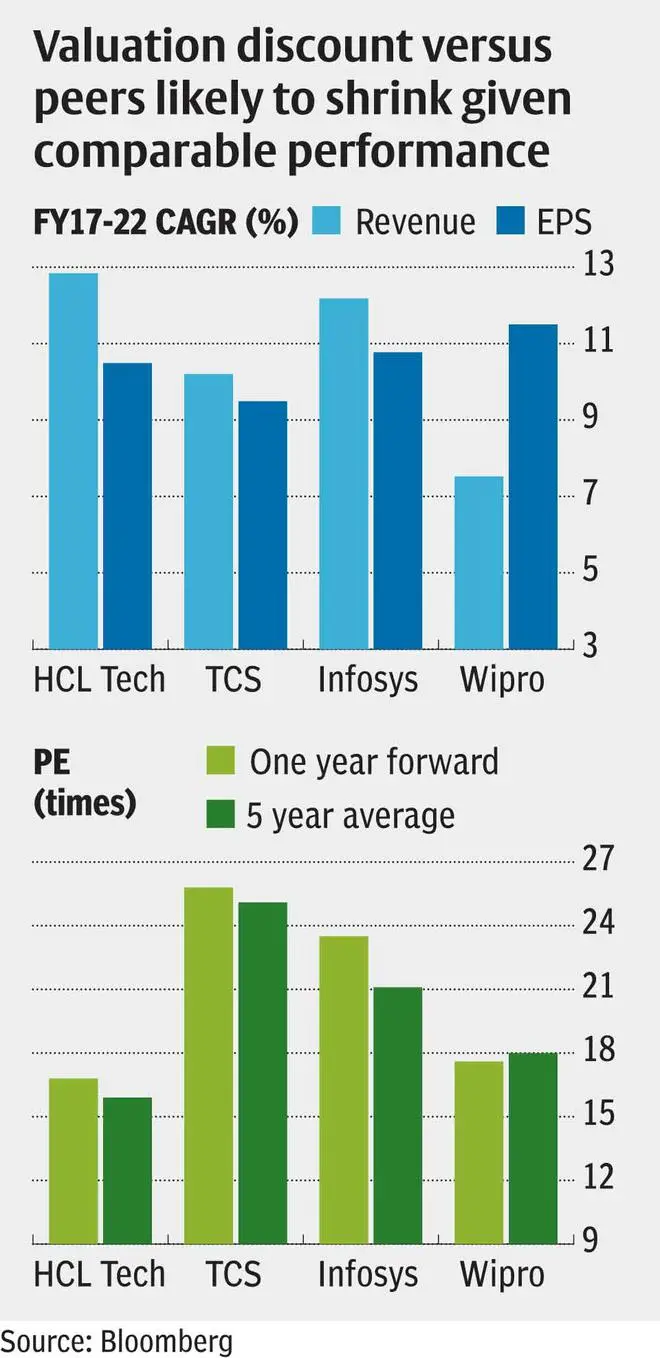

HCL Tech is currently the 3rd largest Indian IT services company behind TCSandInfosys. Business is well-established and diversified across verticals and geographies. Financial services, Manufacturing, Life sciences & healthcare and Technology services are the top verticals accounting for 21, 18, 16 and 15 per cent of revenue respectively. The company derives around 64 per cent of revenue from North America and 28 per cent from Europe. IT services accounts for 89 per cent of revenue, while products business (Products & Platforms segment), accounts for 11 per cent of revenues (IT services making up the rest). The products business performance tends to be lumpy and can impact quarterly performance both ways. However, this is part of a long-term strategy and focus for the company.

In its recently concluded June Q, company performance was mixed, with strong revenue growth offset by margin pressures. Constant currency Y-o-Y revenue growth in IT services was solid at 19 per cent(better than TCS’ 15.5 per cent and below Infosys 21.4 per cent) , with overall growth, including Products & Platforms, at 15.6 per cent. Management commentary in terms of outlook was optimistic, with no impact seen yet due to macro-economic issues in US and Europe. In fact company CEO Vijaykumar noted that he was more bullish on demand now than he was in the previous quarter. The company retained its FY23 constant currency revenue growth guidance of 12-14 per cent.

Thus, while underlying business momentum remains strong, what caused concern were the profit metrics, with operating income (EBIT) of ₹3,992 crore coming in 4.5 per cent below consensus and operating margins at 17 per cent missing consensus expectation of 17.8 per cent. However, on this aspect it needs to be noted that margin and profits missing expectations was a trend seen across the entire spectrum of Indian IT services companies as all of them are impacted by talent shortages and attrition.

The company has retained its FY23 operating margin guidance of 18-20 per cent, with a comment that it will review and update it after conclusion of Sep Q. The analyst community is, however, a bit sceptical on the company meeting its margin targets, given wage hikes that will get reflected in Sep Q results. To the contrary, management is not so pessimistic as they believe they have some revenue (pricing) and cost levers (like freshers coming on board, improving utilisation) to optimise upon and improve profitability. How management manages attrition, which was at 23.8 per cent at the end of Q1 (TCS at 19.7 per cent, Infosys at 28.4 per cent) will be a key factor to monitor.

What works

To sum up, given current global trends, it appears the near-term trend for Indian IT services may get a bit bumpy when slowdown in developed markets impacts clients’ IT budgets. However, the long-term trend remains strong with the ongoing digital transformation cycle that has many years of legs to run on. HCL appears well-positioned to tide through the short-term bumps, given its cheaper valuations and sustainable dividend yield (supported by solid annual free cash flows; net cash at 5 per cent of market cap). In the long term, another factor that is likely to work in favour of HCL is scope for some shrinkage in valuation discount of HCL versus peers like TCS and Infosys (last 5-year EPS CAGR of HCL at 10 per cent is similar to that delivered by TCS).

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.