The performance of office-based real estate investment trusts (REITs) in India has been a disappointment so far with per unit distribution yields below the benchmark 10-year government paper and little capital appreciation since their listing.

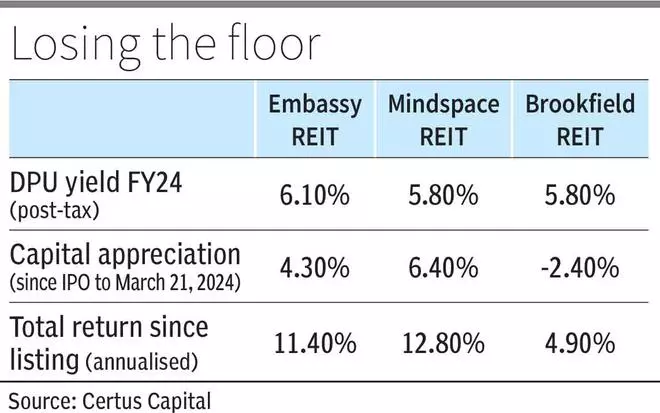

In FY24, the distribution per unit yield of the three office REITs – Embassy Office Parks, Mindspace Business Parks, and Brookfield India Real Estate Trust – ranged between 6 and 7 per cent on a pre-tax basis and 5.8 to 6.1 per cent post-tax, according to calculation by Certus Capital.

Currently, the yield on a 10-year government securities paper is well above 7 per cent.

The capital appreciation of the REITs have also been underwhelming. Embassy REIT’s units have appreciated a mere 4.3 per cent from its IPO price to March 31, 2024, that of Mindspace REIT has gone up 6.4 per cent, while units of Brookfield REIT have fallen 2.4 per cent. Embassy REIT listed in 2019, Mindspace REIT in 2020 and Brookfield REIT in 2021.

Compare this with the Nifty Realty Index that has nearly quadrupled over a five-year period and more than doubled in one year.

Embassy REIT has performed better in FY24 with its units appreciating 18.4 per cent. Mindspace REIT’s units appreciated 5.6 per cent, while that of Brookfield REIT fell 9 per cent.

The total annualised return of the REITs has ranged between 4.9 and 12.8 per cent since their respective listings and FY24-end.

Vacancies

While office leasing activity and rents have improved over the past 2-3 years, vacancy levels at the REITs remain high. At Embassy REIT, vacancy levels have increased to 15 per cent in FY24 from 7 per cent in FY20, while that at Brookfield REIT has risen to 18 per cent from 13 per cent in FY21. Mindspace REIT, however, saw a dip in vacancy at 11 per cent from 16 per cent in FY21.

A major reason for the high vacancies is the exits that have been witnessed over the past several quarters, especially by IT companies where hiring has dipped, and many multinationals have also given up office space. This has dragged down the net leasing by the REITs, while gross leasing was decent.

The fourth quarter of FY24 also saw exits, but the pace is moderating, Nuvama Institutional Equities pointed out in a note on the sector.

Other real estate companies which have office assets in their portfolio have also seen significant uptick in vacancies. At Oberoi Realty, vacancies doubled between FY20 and FY23 to 26 per cent before falling to 20 per cent last fiscal year. DLF Cyber City Developers, which has a substantial office portfolio, has also seen an increase in vacancies but in single digits.

Management commentaries by individual REITs have held out hopes of occupancies trending up higher in future quarters as leasing picks up.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.