In today’s digital age, protecting oneself from online frauds is crucial as most people rely heavily on the internet for financial transactions. Through seemingly innocuous means such as SMS, these cybercriminals can gain access to sensitive personal information, including passwords, one-time passwords (OTPs), contacts, and other critical data.

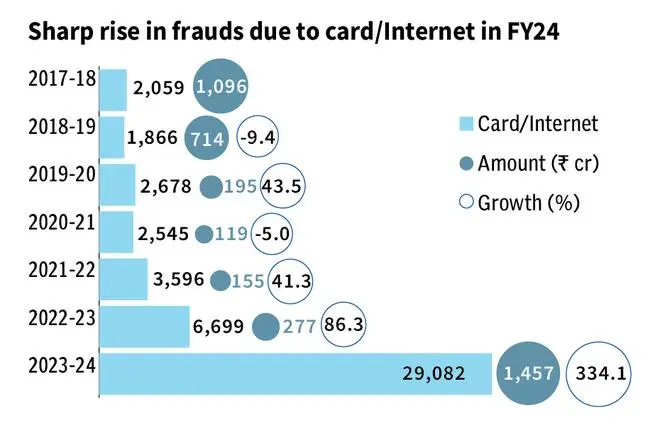

The Reserve Bank of India’s (RBI) 2024 annual report shows that in FY24, the largest number of banking frauds were related to the card/internet category with 29,082 incidents accounting for 80 per cent of all frauds. This was 334 per cent higher than the 6,699 frauds in this category in FY23. The 29,082 frauds in FY24 account for ₹1,457 crore worth of card/internet fraud, the highest amount in the last six years.

Nowadays, various types of online financial scams occur, including phishing, identity theft, hacking, and malicious software.

“Increased digitisation of the financial services ecosystem and increased adoption by customers for transacting through digital channels including payment gateways, has resulted into increased volumes through these channels. Fraudsters understand this trend and explore the vulnerabilities that are inherent in these channels as well as the customers (especially senior citizens) and hence we see the outcome,” Vivek Iyer, a Partner at Grant Thornton Bharat Iyer, explained.

The overall number of frauds in India has increased significantly. In FY23, 13,564 frauds were recorded, growing to 36,075 frauds in FY24. Of these, frauds related to cards and the internet have seen a sharp rise. There were 2,059 such frauds in FY18, which gradually increased to 3,596 in FY22. This number then surged to 6,699 frauds in FY23, and dramatically jumped to 29,082 frauds in FY24.

“Controls with respect to fraud prevention in advances are built at a disbursement level and the disbursements are done by the banking operations staff and customers have no role to play in it and hence the levels of vulnerability with respect to advances is minimal. This is not the case with customer-initiated payments where the vulnerabilities, especially behavioural are high and hence a high level of frauds there,” added Iyer.

According to the Future Crime Research Foundation’s (FCRC) report, ‘A Deep Dive into Cyber Crime Trends Impacting India,’ from January 2020 to June 2023, online financial frauds accounted for 77.4 per cent of all frauds. This was followed by online and social media-related crimes at 12 per cent and hacking/damage to computers at 1.5 per cent.

The FCRC report also suggests that among the 77.4 per cent of online financial frauds that occurred in India, UPI fraud constitutes 47.2 per cent, debit/credit card and SIM swap fraud account for 11.2 per cent, and internet banking-related fraud comprises 9.2 per cent, making them the most prevalent types of online financial fraud.

The RBI’s Integrated Ombudsman Scheme annual report shows that in FY23, most complaints lodged with the ombudsman were related to mobile/electronic banking, accounting for 20.3 per cent of the total complaints. This was followed by complaints about loans and advances (20.1 per cent), deposit accounts (17.1 per cent), and ATM/debit cards (14.6 per cent).

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.