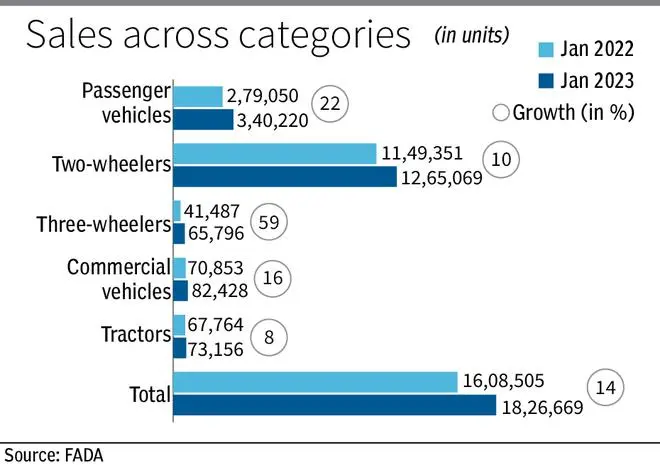

The two-wheeler retail sales in January grew 10 per cent year-on-year (y-o-y) to 12,65,069 units as against 11,49,351 units in the corresponding month last year, show the monthly data shared by Federation of Automobile Dealers Associations (FADA) on Monday.

However, the rural market is yet to improve as cost of ownership is still high.

“While sentiments are improving at a snail’s pace and are better than what it was a year ago, rural market is yet to fully come to the party as cost of ownership has shot up significantly while disposable income has not increased in the same ratio,” Manish Raj Singhania, President, FADA, said.

Cash crunch

According to a report by ICRA recently, pandemic-induced income uncertainty, coupled with steep rise in cost of ownership, constrained demand over FY20-FY22. But, the low base and opening-up of the economic activity to support industry volume growth may drive domestic market growth over near term as export outlook remains weak.

“The basic income will increase due to the new tax regime announced in the Budget, which has left some money in the pockets of people. The rural demand is expected to improve due to such relief. Hero MotoCorp and Honda Motorcycle & Scooter India (HMSI) have recently launched 110cc scooters to attract rural customers and are also expected to launch more commuter segment motorcycles and scooters in future,” Som Kapoor, EY India Automotive, Future of Mobility Leader (Consulting), and Partner, told businessline.

Mixed bag

Both Hero MotoCorp and HMSI reported decline in wholesales (dispatches to dealers) in January. While Hero reported a decline of more than 2 per cent y-o-y to 3,49,437 units (3,58,660), HMSI reported a decline of 12 per cent y-o-y to 2,78,143 units (3,15,196). Other players such as TVS Motor Company, Bajaj Auto and Royal Enfield reported positive numbers.

Meanwhile, in the overall segments, FADA report said the industry grew 14 per cent y-o-y in the month to 18,26,669 units (16,08,505).

The passenger vehicle (PV) segment continues to perform well with a growth of 22 per cent. While good enquiry, healthy bookings and improved supplies are helping this segment, it is the entry level sub-segment which is still feeling the pinch, Singhania said. Apart from this, while waiting period for some models have come down, compact SUVs, SUVs and luxury vehicles continue to witness minimum waiting of around three months, he said.

“With China’s factory activity once again gaining pace, global supplies of parts and semiconductors will see a recovery, thus aiding better vehicle supplies and lower waiting period in future. This will further fuel growth for the already healthy PV category,” Singhania said.

The commercial vehicle category has also shown growth of 16 per cent to 82,428 units (70,853). Continued demand in the market due to replacement of fleet, growth in freight availability and government’s consistent push for infrastructure projects has helped the CV segment rise above pre-Covid numbers, Singhania added.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.