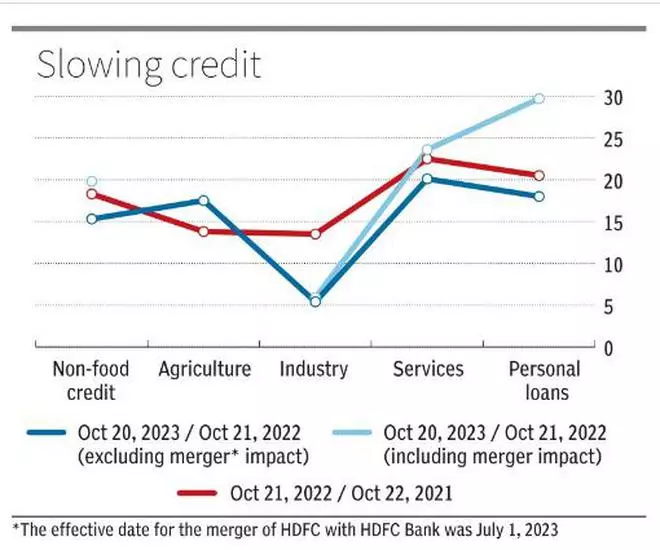

Non-food bank credit growth moderated to 15.3 per cent year-on-year in October 2023 as compared with 18.3 per cent a year ago due to a sharp decline in credit to industry and deceleration in credit to the services and personal loans sectors, as per RBI data on Sectoral Deployment of Bank Credit.

The non-food bank credit, which includes credit to four major sectors – agriculture, industry, services and personal loans, growth rate for October 2023 excludes the impact of the merger of a non-bank (HDFC) with a bank (HDFC Bank). Including the impact of the merger, the credit growth for October is higher at 19.8 per cent.

Agriculture bucks the trend

Out of the four major sectors, only credit growth to agriculture and allied activities improved to 17.5 per cent y-o-y in October 2023 from 13.8 per cent a year ago.

Credit growth to industry slackened to 5.4 per cent y-o-y in October 2023 as compared with 13.5 per cent in October 2022.

Credit growth to services sector slowed to 20.1 per cent y-o-y in October 2023 as compared with 22.5 per cent a year ago. Within this sector, ‘non-banking financial companies (NBFCs)’ and ‘trade’ sub-sectors were the major contributors to credit growth in the reporting month.

Personal loans growth decelerated to 18 per cent y-o-y in October 2023 (20.5 per cent a year ago), due to moderation in credit growth to housing, according to an RBI statement.

CARE Ratings, in a report earlier this month, said the outlook for bank credit offtake remains positive, with a projected growth of 13-13.5 per cent for FY24, excluding the merger’s impact.

Furthermore, as the Credit to Deposit ratio remains elevated, growth in the liability franchise would play a significant role in sustaining loan growth.

However, inflation, elevated interest rates and global uncertainties could potentially impinge on the credit growth in India.

The credit rating agency observed that the competition for deposits is likely to intensify even further, resulting in a rise in funding costs in the coming period as rates remain elevated and CASA (current account, savings account) share reduces.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.