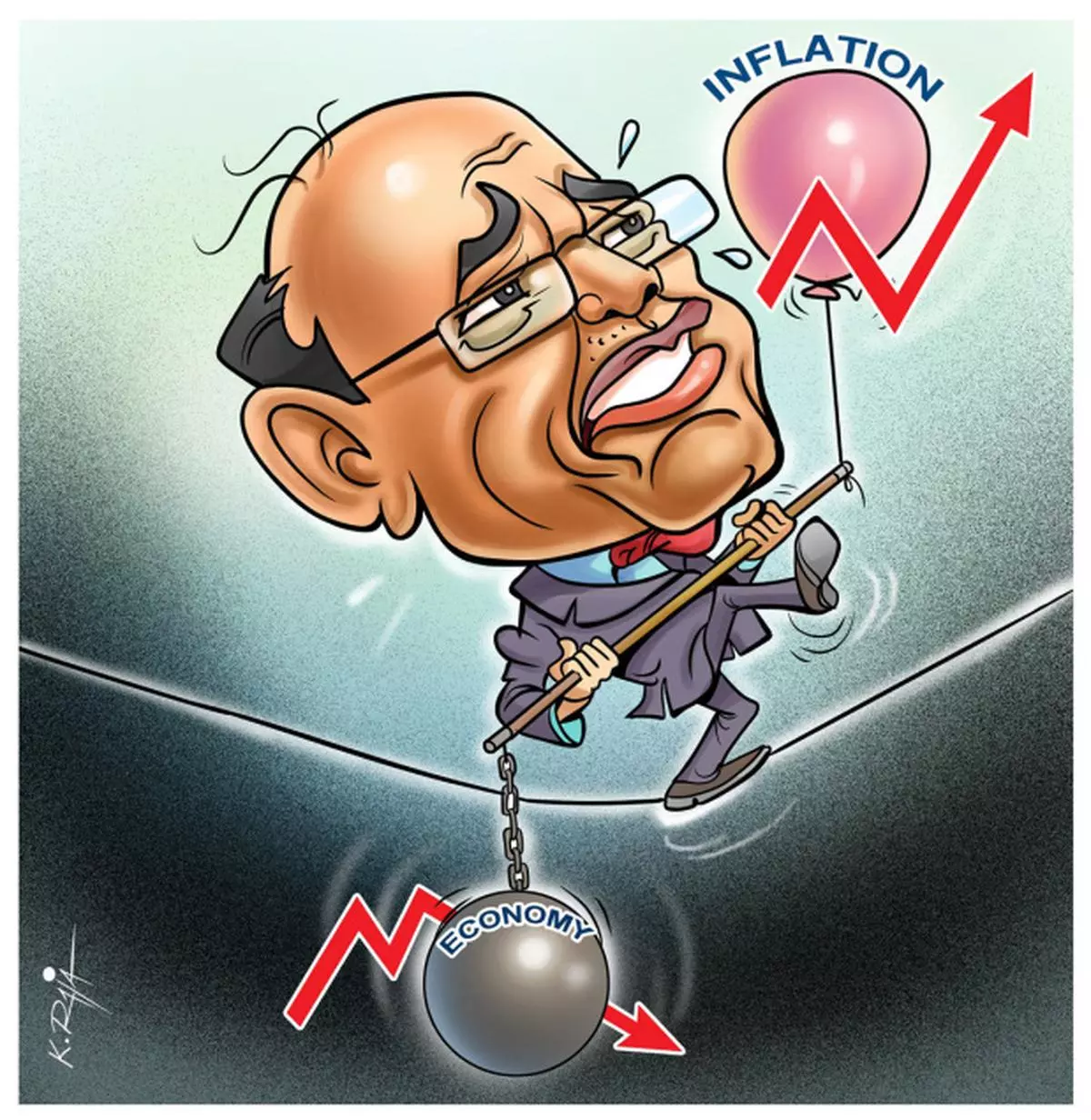

The situation facing the Reserve Bank of India (RBI) as it formulates its mid-quarter review of monetary policy is depressing. The growth rate for the last quarter of 2011-12 was 5.3 per cent, the lowest in many years. What is disheartening is that it continued a trend that started in April-June 2011, when growth was 7.7 per cent (against 8.5 per cent in the previous one), followed by a decline to 6.9 per cent and 6.1 per cent in the following two quarters.

While data on industry and exports are discouraging, the Consumer Price Index for Industrial Workers for April 2012 has also shown an annual increase of 10.22 per cent.

The debate on growth versus price stability is again at the forefront. The choices before the Government are hard. They call for a reduction in fiscal deficit, the enactment of much-needed structural reforms and, most importantly, improvement in the administration of schemes such as the Mahatma Gandhi National Rural Employment Guarantee Scheme, under which employment, income and purchasing power are generated without much contribution to output. Will the Government bite the bullet or allow matters to drift?

Credit growth

The corporate sector is asking for cuts in interest rates, citing their current high levels for deceleration in the growth of the economy. There are observers asking for a further injection of liquidity in the economy through a cut in the cash reserve ratio (CRR) requirements for banks. But what are the facts?

In the first place, there is no lack of demand for credit at the prevailing interest rates. The credit-deposit ratio (CDR) stood at 76.72 per cent on May 18, 2012, thanks to the repo window of the central bank. Incremental CDR, year-on-year, on May 18, 2012 was even higher at 88.55 per cent.

Credit growth has stabilised around 16 per cent in the last 10 fortnights ended May 18, 2012, against an RBI-projected estimate of 17 per cent for 2012-13.

The banks had investments in mutual funds amounting to Rs 46,100 crore. The Statutory Liquidity Ratio (SLR) for the system stood at 30.12 per cent above the required 24 per cent.

Fall in GDP growth

Thus, there is no slackness in demand due to the high interest rates; and the economy is flush with liquidity. There is no case for any injection of funds through, say, a reduction in CRR.

For the RBI, the hard choice is between growth and inflation. In the past, the bank had given an indication that its policy stance could be reversed if the trend rate of growth of 8 per cent falls persistently.

Under the present circumstances of declining growth in GDP over four quarters, culminating in an annual growth of only 6.5 per cent in 2011-12, it is easy to reduce the policy rates by another 25 or 50 basis points. But would it help to raise the GDP or fight inflation? Today, the price levels are so high that consumers have to cut down the quantity of goods and services they consume to make ends meet, which affects aggregate domestic demand. More than 200 Udipi restaurants, once popular and relatively inexpensive, are reported to have closed in Mumbai in the last year or so.

Exports, likewise, depend on world income and relative prices. The second part is taken care of by the steep depreciation of the rupee. But the first one is not within the control of the RBI.

Reduction in rates

As company finance studies have shown, interest expenses account for a small proportion of the total cost of production. So a reduction in rates is not going to result in a decline in the prices of manufactured goods. Depreciation of the currency and fiscal concessions are easy options for stimulating exports, but devising cost-efficient methods of production is hard.

A major problem on the external front is the depreciation of the rupee. While the Non Resident External Rupee deposits are completely deregulated, the Foreign Currency Non Resident (B) scheme is still subject to ceilings in interest rates. As a result, there has been a diversion of deposits from the latter to the former. Interest income from Non-Resident deposits is free of tax in India. But it is taxable in other countries except those in the Gulf.

One characteristic of the NRI distribution is that those working in the Gulf are mostly blue-collared workers, whereas others in the rest of the world are high net-worth professionals.

There is no doubt that the latter are more affluent and their wealth should be tapped. While the Gulf NRIs are influenced in their remittances by the depreciation of the rupee, those in the rest of the world look for yields in their investment decisions where tax considerations prevail.

Refinance window

Our banks have to offer attractive yields compared with the low returns of 1-2 per cent that NRIs get in their resident countries. The RBI can help the banks in offering good rates, by exempting all incremental or fresh NRI deposits not only from interest rate regulation but also from the SLR.

Banks can offer forex currency loans to Indian entrepreneurs on attractive terms so that they do not resort to external commercial borrowing.

The RBI can think of opening a refinance window for such loans. It will help to stabilise the rupee; the forex will return to the reserves when repayments are made, unlike in the case of market intervention, and the central bank will earn a better return than what it is getting from its present portfolio.

(The author is a Mumbai-based economic consultant.)

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.