Stock markets around the world have turned volatile this year amidst fears of monetary policy tightening. The US Fed has aggressively hiked rates there to tame inflation. Higher interest rates have dampened bullish sentiment towards riskier assets, as central banks elsewhere in the world had to follow through. However, Indian equities have been an outlier of sorts amidst this gloom and doom. Year to date, Nifty 50 and Sensex are up over 2 per cent when China (Hang Seng) is down 36 per cent, US (Nasdaq) is down 29 per cent, Germany (DAX), down 17 per cent and France (CAC 40) down 12 per cent.

India appears to be relatively well-placed, like a steady ship in choppy waters, given stronger macro fundamentals compared to many peers. The RBI projects India to grow at 7 per cent in FY23. This places the Indian economy, the 5th largest now after overtaking the UK, on track to pip Germany in 2027 and Japan by 2029 at the current rate of growth, as per an SBI research report.

In this backdrop, investors in India today have an opportunity to dig their heels deep and increase exposure to four select themes to bet on the domestic economy — manufacturing, infrastructure, financial services and transportation/logistics. All these investment plays are multi-year opportunities, given the anticipated growth in the Indian economy. We highlight for you the best-in-class offerings available in the MF route to capitalise on these attractive thematic opportunities.

Manufacturing

India missed the manufacturing bus in the eighties, even though we did excel in services such as software to become the back office to the world. Now, with China+1 becoming a geopolitical imperative, it is an opportune time for India to expand the manufacturing sector. Real manufacturing gross fixed capital formation is expected to rise from 5.5 per cent to 7 per cent levels of GDP by FY27, with absolute number almost doubling in this period. This is expected on the back of a renaissance in the Indian manufacturing sector, thanks to phased manufacturing programmes, ‘Make in India’ focus, Production Linked Incentive (PLI) scheme, 100 per cent automatic foreign direct investment in sectors, tax cuts, single-window clearance system, import duty protection, etc. In short, manufacturing in India now has the potential to be a major driving force for the economy.

What might work in India’s favour today is the potential for significant domestic demand, Government’s drive to encourage manufacturing, and a distinct demographic edge. The manufacturing sector could outpace overall GDP growth by approximately 4 per cent, leading to an incremental contribution opportunity of $300-$500 billion from the manufacturing sector to the economy in 2030, as per Mirae Asset. In this scenario, the manufacturing sector’s share towards India’s GDP in 2030 could potentially reach around 20 per cent, it said.

Funds: There are over half a dozen manufacturing theme-focussed offerings, including three passive investment options. But half of them are recent funds, having been launched within the last one year. Given the short time period that the theme has been in focus, go for options with some track record. The funds that fit the bill here are ABSL Manufacturing Equity and ICICI Pru Manufacturing. The latter has done better in terms of beating benchmarks. Both have differentiated portfolios but ICICI Pru offering is more concentrated. Auto stocks are a big bet for both the actively-managed funds we recommend but while ABSL’s top preferences are consumer non-durables and pharma, the ICICI Pru offering favours petroleum products and cement .

Another noticeable feature is the multi-cap approach (large: 50, mid: 25 and small: 20) of the ABSL fund, while IPru scheme has capped small-cap exposure to 7 per cent. Cost-conscious investors can use Navi Nifty India Manufacturing Index Fund (direct plan: expense ratio of 12 bps) or (36 bps) to play this theme. While the S&P BSE Manufacturing Index has outperformed S&P BSE 100 in the last one year, there is a tactical opportunity for the manufacturing sector, given its under-performance in 3- and 5-year periods.

Banking and finance

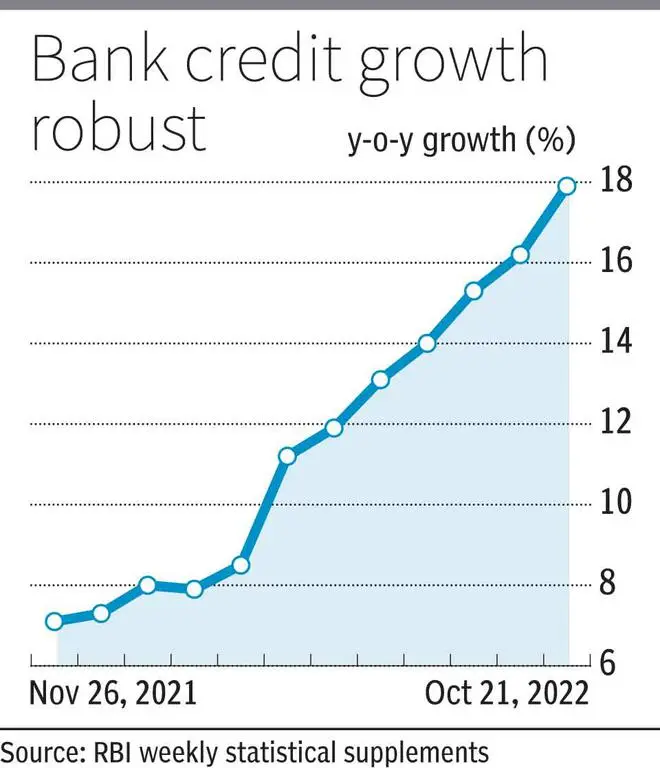

The banking and financial services sector serves as a proxy to India’s growing economy, since every aspect of the economy is influenced by it. This broad universe appears well-placed for meaningful growth, with tailwinds such as improving credit growth (nine-year high of 16 per cent yoy in September 2022), adequately capitalised balance sheets, clean-up of NPAs, etc. The Government thrust on infrastructure and manufacturing is expected to provide impetus to the credit demand. Retail credit has been increasing at a steady pace over the last few years and is expected to grow, given the under-penetration of retail credit in India.

In the short term, there is continued traction in the retail and SME segment, while the Corporate segment is also seeing a revival. Home, Vehicle, Unsecured, and Small Business continue to do well, while the demand for CV is also improving. Credit cards business is seeing healthy momentum too.

Over the past decade, India’s financial services sector has been hammered by demonetisation, IL&FS crisis, YES Bank’s collapse, etc. But, investing in high-quality financial stocks has proven to be rewarding. Besides banks, NBFCs, insurers, asset managers and brokers have a massive opportunity to consolidate market shares. Well-run lenders with adequate capital can grow faster as the economy becomes larger. With only 5 per cent of Indian wealth in financial assets, non-lenders are a great way to play the large structural opportunity that presents itself from the ‘financialisation’ of Indian household savings. Rapid urbanisation (50 per cent by 2050), rising income (per capita income growth nearly 7 per cent over the last 15 years) and high savings rate (29 per cent) are key growth drivers of the financial sector. Nifty Bank index is expected to show 30 per cent earnings growth over CY21-23, as per Bloomberg consensus expectations.

Funds: At this moment, there are 15 actively-managed banking and financial services funds. We prefer at least 5-year track record funds that have balanced exposure to financials across domains such as banks, finance and insurance — for instance, ABSL Banking & Financial Services (60:29:6), ICICI Pru Banking & Financial Services (55:29:10) and Nippon India Banking & Financial Services (60:31:5). From pure alpha perspective, SBI Banking & Financial Services is the only offering that has beaten benchmark on 1-, 3- and 5-year returns.

Three-year and 5-year rolling returns based on last 10 years of the biggest actively-managed funds show that Nifty Bank total return index has been hard to beat, for the majority. So, passive funds may be a better way to play this theme. There are 20 passively-managed offerings comprising 4 index funds and 16 ETFs based on banks as a whole, private-sector/public-sector banks, and financials (excluding banks). Edelweiss ETF-Nifty Bank (5 bps) and Navi Nifty Bank Index Fund (10 bps) are the cheapest in the respective sub-segments. In terms of lowest one-year tracking error, ICICI Pru Nifty Private Bank ETF and SBI Nifty Private Bank ETF are alternatives.

Do note that since BFSI is already a big weight in Nifty 50/Sensex or any large-cap fund/index, investors should go for incremental exposure only after taking into account their current indirect allocation through other funds.

Infrastructure

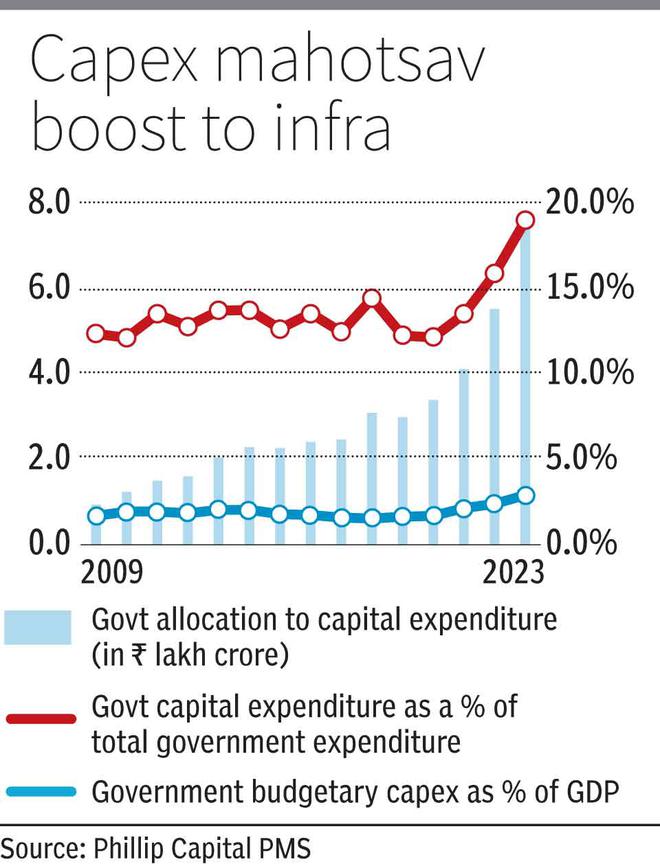

With India aiming to be a $5-trillion economy, the focus on infrastructure development has deepened in many ways over the last few years. Investments in infra have a snowballing effect on growth in several supply and demand-side channels. To achieve GDP of $5 trillion, India needs to spend about $1.4 trillion (over ₹100 lakh crore) over these years on infrastructure so that lack of infrastructure does not become a constraint to the growth of Indian economy, according to government calculations (Eco Survey 2020). Given the large listed universe of stocks that fall in infra theme, it is a multi-sector opportunity spanning asset owners (roads, railways, ports, power and telecom), asset financiers (lenders) and asset creators (construction, cement).

Infrastructure as a theme came into vogue in 2004 and picked up pace till 2008 before the global financial crisis spooked markets. Due to concentrated exposure, infrastructure theme can go through extended periods of under-performance as it did in 2018 and 2019. Given that infrastructure projects are long-gestation in nature, it is high-risk and there is a long wait involved. Hence, investors in this space must prep up to stomach intermittent periods of under-performance. Nifty Infrastructure index earnings are anticipated to show double-digit CAGR growth over CY21-23, as per Bloomberg consensus estimates.

Funds: Most of the 20+ infrastructure-oriented thematic mutual funds have 3- and 5-year track record. About half of the funds have beaten relevant benchmarks in 1-, 3- and 5-year periods, while half a dozen have also outshined category average returns. We prefer Kotak Infra & Eco Reform, ICICI Pru Infrastructure and Tata Infrastructure on account of better portfolio diversification in terms of top sectoral and top stocks concentration. Across infra funds as a category, Industrial Products, Construction Projects, Industrial Capital Goods, Power, Cement and Banks are top choices and this plays out for the recommended funds. In terms of m-cap exposure, Tata and Kotak offerings are more mid- and small-cap oriented but ICICI Pru appears to have preferred large-caps and capped mid-cap exposure. Do note these are thematic bets and should form part of the satellite portion of your portfolio.

Logistics and auto

If everyone is moving forward together, then success takes care of itself, said Henry Ford. Rapid urbanisation is accelerating growth in personal mobility requirements. Additionally, powerful enablers such as strong demand-led recovery cycle and margin improvement provide visibility for strong earnings growth for the auto/transportation and logistics sector. Consisting of more than a dozen sub-sectors, this theme provides a wide spectrum of investment opportunities, facilitating effective diversification of the portfolio.

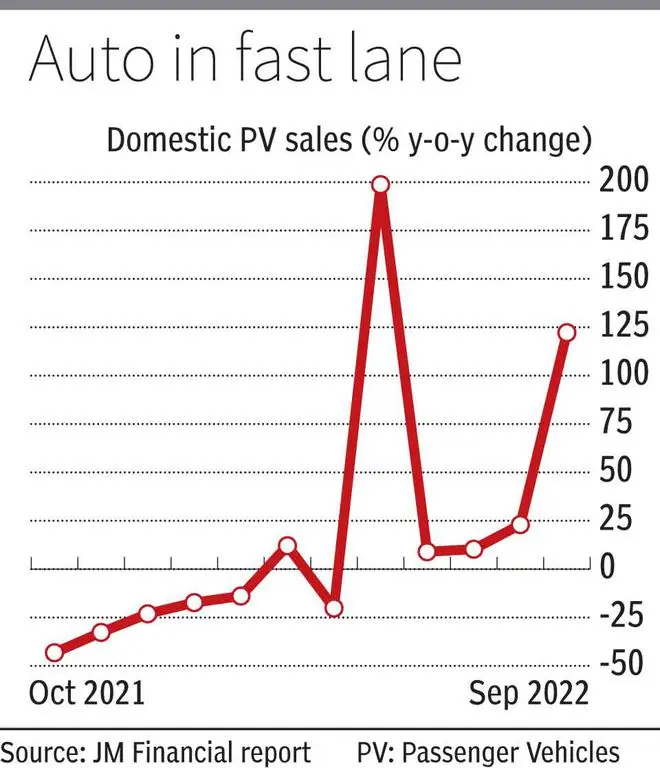

After a hiatus starting well before the pandemic, the auto cycle is finally looking up now, with utility vehicle (UV) and commercial vehicle (CV) sales leading the pack. After Power, BSE S&P Auto index is the best performing sectoral index year to date, with 22 per cent gains versus 2.9 per cent for the Sensex. Given the auto cycle typically holds for about three years, there is a case for tactical investment in funds focussed on the auto sector. Replacement demand, order backlog and lower inventory are key drivers here, apart from long-term ones such as the shift to electric vehicles. Nifty Auto is expected to show multifold (100 per cent CAGR) growth in earnings over CY21-23 period, as per Bloomberg consensus estimates

In case of logistics and transportation, enablers such as increased cashless payments, regulatory changes/policies such as National Logistics Policy (NLP) and PM Gati Shakti, technological advancement and export potential are positive. For logistics service providers, factors such as rise in foreign trade, shifts from unorganised to organised markets post GST and improving infrastructure are boosting fortunes. Long-term drivers such as e-commerce are also brightening the ecosystem.

Funds: Those who have a high appetite for risk can consider investing in UTI Transportation and Logistics. This is the only active fund focussed on the sector currently with a good enough track record (IDFC and ICICI Pru offers launched recently). Nifty Auto ETFs (from Nippon India and ICICI Pru) and one index fund from IPru may be good investment options if you want to track the underlying basket at a low cost (direct plan: 20 bps). However, the UTI T&L fund should be the go-to choice as the active fund is a proven player in terms of providing broader market exposure and good returns

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.