Across the globe, the central banks went on a gold buying spree purchasing record levels of the precious metal in the third quarter of 2022, according to World Gold Council’s latest demand trends.

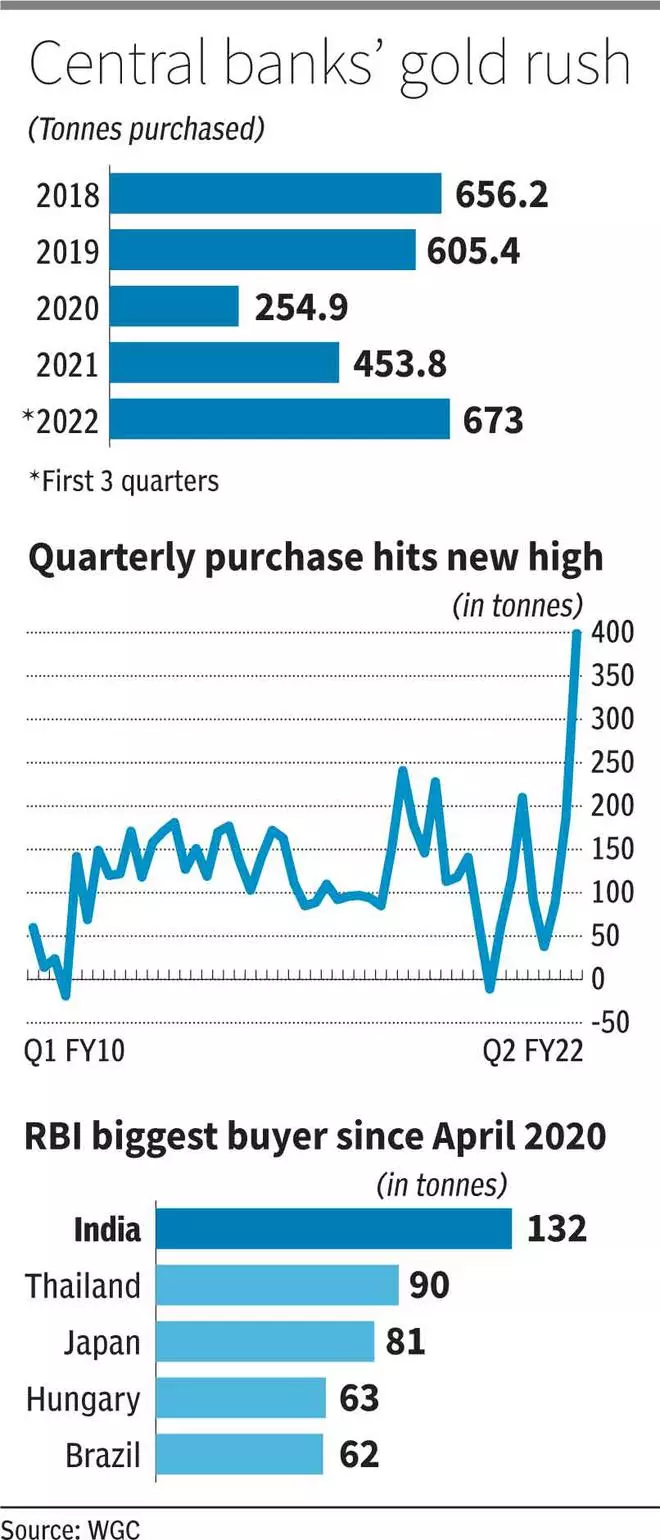

Central banks bought 399.3 tonnes of the yellow metal compared to 90.6 tonnes in the same quarter of 2021. This is the highest purchase in a quarter, in more than a decade.

With this, central bank demand, which stands at 673 tonnes for the first nine months of 2023, has already exceeded the record yearly purchase of 656.2 tonnes they made in 2018.

Economic uncertainty and reserves rebalancing seem to have prompted this move.

Safety factor

In the 2022 annual survey of central banks by the WGC, ‘Historical Position’ was the top reason cited by central banks to buy gold. Gold has always been a critical component of a country’s reserves.

Others factors they find relevant are gold’s dependable performance during a crisis, as a tool to hedge against inflation and no risk of default. So, given the prevailing high inflationary environment and global growth uncertainties, it is not surprising that central banks are stocking up on gold.

Even in 2018 (656.2 tonnes) and 2019 (605.4 tonnes), when there were worries about a global economic slowdown, central banks had bought substantial quantities of gold.

Dollar rebalancing

Secondly, since the dollar, another key component of reserves of most countries, has rallied significantly, the weight of it in the overall reserves would have gone up. The dollar index has appreciated 16 per cent this year until October. Therefore, central banks might want to add gold to rebalance their reserves to their preferred strategic level.

Although the buying is at record levels, granular data on who’s buying is available only for about 120 tonnes out of the total 399 tonnes central bank picked up. Given their huge holding and affinity for gold, there is speculation that Chinese and Russian central banks were the unknown buyers. In the past, Russia has led the way, in 2018, for instance. And China last reported its gold holding in September 2019.

India factor

The Reserve Bank of India was the third largest among the known buyers in Q3 of 2022 as it added 17.5 tonnes to the reserves. “Because of the fluctuation in the rupee-dollar exchange rate, trade deficit concerns and geopolitical uncertainties, the RBIadded a considerable quantity of gold.

The objectives of central banks are different from market participants, and their actions thus guided by the demands of the economy and financial stability,” says Soumyajit Niyogi, Director, Core Analytical Group, India Ratings and Research.

Interestingly, the RBI is also the largest buyer since the pandemic by purchasing 132.4 tonnes between April 2020 and September 2022. According to the WGC, gold as a percentage of the RBI’s total reserves stood at nearly 8 per cent at September-end, slightly higher than 6.5 per cent a year ago.

Outlook

Alongside buying by central banks, jewellery demand led by India and China also saw a surge in Q3. However, despite jewellery and central bank demand shooting up, the average price of gold was down 3 per cent y- o-y in Q3 at $1,728.9/ounce (LBMA price) and has dipped further now.

Price down

Significant outflows from global gold ETFs (Exchange Traded Funds) have also weakened the price. According to WGC data, the net outflows from ETFs stood at about 227 tonnes in Q3, the highest since Q2 of 2013.

“We believe central banks’ gold buying will continue as gold’s safe haven and diversification attributes feature strongly in an era of global uncertainty. Jewellery demand — even though we might not see the quantum we saw in Q4 last year — will stay steady,” says PR Somasundaram, Regional CEO - India, WGC.

However, whether these factors may have a positive impact on prices needs to be seen. The Q3 trend suggests otherwise. Unless there are any promising signs of recovery in prices, investment demand (ETF buying) may not pick-up.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.