Mirae Asset MF has recently launched a flexi-cap fund offering. This is the 7th new fund launch in this popular category by fund houses in the last one year. The flexi-cap fund category, announced in 2020 by SEBI, mitigated the risk of many multi-cap funds, which would ordinarily have to rejig portfolios to comply with the new mandate of at least 25 per cent each in large-, mid- and small-cap stocks. The definition of the flexi-cap category is quite liberal as holding at least 65 per cent of portfolio in stock-related instruments acts as a qualifier. Thus, such dynamic equity schemes investing across companies of any market capitalisation enjoy the full freedom with no bias to sectors and possess the flexibility to move across large-, mid- and small-cap basis respective framework. But have the funds done justice to the leeway? Let’s find out.

Basics

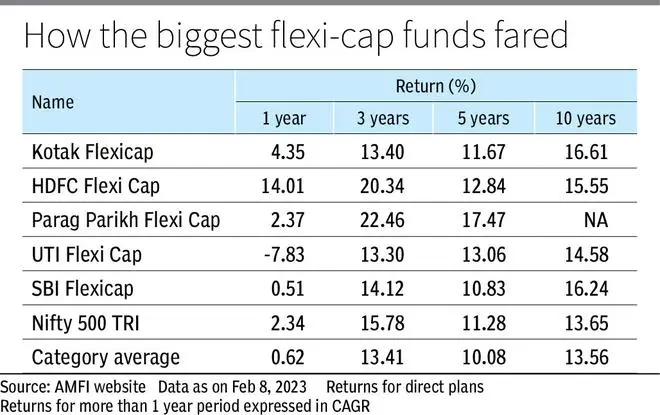

There are 33 flexi-cap equity funds in the market, the second biggest category in terms of diversified schemes. In terms of investor assets, flexi-cap funds, as a group, are the biggest with nearly ₹2.5-lakh crore across 1.25 crore investor accounts. This category is home to some of the oldest and also largest schemes such as Kotak Flexicap, HDFC Flexi Cap, Parag Parikh Flexi Cap, UTI Flexi Cap and SBI Flexicap. With creation of this so-called new fund category in 2020, the schemes’ then current strategy, risk level, and portfolio make-up did not have to change much, courtesy a liberal definition.

The flexibility to align the portfolio with risk-reward perceptions is handy. On paper, the freedom to move in and out of stocks is a great advantage. Sectoral divergence is noticeable, and changes happen each year both in terms of top performers and bottom performers. Different sectors behave differently. Winners can be across market caps, and so narrow investment mandates can rob the fund of the freedom to take/exit positions. This suits new investors who are seeking exposure across market caps through a single fund.

Portfolio

So, how have flexi-cap funds used the leeway? As per ACE MF data up to December 2022, flexi-cap funds, on an average, have 69.5 per cent allocation to large-cap stocks, 15.2 per cent in mid-cap stocks, and 7.9 per cent in small-caps. Clearly, flexi-cap funds have heavily relied on the steadiness that large-cap stocks bring to the portfolio, while allocating about one-fourth of money to mid- and small-caps which provide better growth potential. This distribution has broadly not changed much vis a vis one year ago and also when compared to December 2020 (category creation time). Interestingly, at current m-cap distribution levels, flexi-cap funds are somewhat similar to tax-saver ELSS funds. Tax-saver funds have 71.3 per cent allocation to large-caps, 16.9 per cent to mid-caps and 11.4 per cent to small-caps.

In terms of sectoral allocation, flexi-cap funds have bet big on Banks (23.2 per cent), Software (9.5 per cent), Finance (9.1 per cent), Consumer Non-Durables (5.4 per cent), Auto (4.5 per cent). Pharmaceuticals, Petroleum Products, Cement and Construction Project have 2-4 per cent individual exposure. A majority (70 per cent) of flexi-cap funds have Nifty 500 TRI as their benchmark, while one-third have adopted S&P BSE 500 TRI as the yardstick. Barring a few sectoral tweaks, BFSI, Technology and Consumer seem to be dominant themes in flexi-cap category.

Returns

Amongst the market-cap based equity fund categories, flexi-cap funds, at the moment, rank low in terms of category-average return. In one-year period, 0.62 per cent return of flexi-cap funds places it just at the bottom just above small-cap funds (0.52 per cent). In three-year period, category average return of flexi-cap funds at 13.4 per cent CAGR is the lowest and even below 13.7 per cent of large-cap funds. The same story plays out in the five-year period too. In the 10-year timeframe, flexi-cap funds with 13.6 per cent CAGR is placed fourth among five categories including small-cap, mid-cap, large and mid-cap, and large-cap funds. Individually, four funds — HDFC Flexi Cap, JM Flexicap, Quant Flexi Cap and Franklin India Flexi Cap — consistently beat category-average return across all the aforementioned time periods.

Actively-managed funds charge higher expenses (TER of flexi-cap funds is 1.5-2.5 per cent) to deliver alpha and so should be assessed using this metric. Using Nifty 500 TRI as benchmark versus flexi-cap funds, the category has under-performed by 172 basis points in one-year period, 237 basis points in three-year period, 120 basis points in five-year period and 9 basis points in 10-year period. Individually, the percentage of flexi-cap funds outperforming Nifty 500 TRI is low in one- and three-year periods at 33-39 per cent, but the share of outperformers dramatically rises to over three-fourth in five- and 10-year periods. Three schemes — HDFC Flexi Cap, Franklin India Flexi Cap and Quant Flexi Cap — are the most consistent outperformers across all time periods.

Based on proprietary bl.portfolio Star Track MF ratings system, Parag Parikh Flexi Cap and Quant Flexi Cap are 5-star rated, while four funds such as Canara Robeco Flexi Cap, HDFC Flexi Cap, JM Flexicap and PGIM India Flexi Cap are 4-star rated.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.