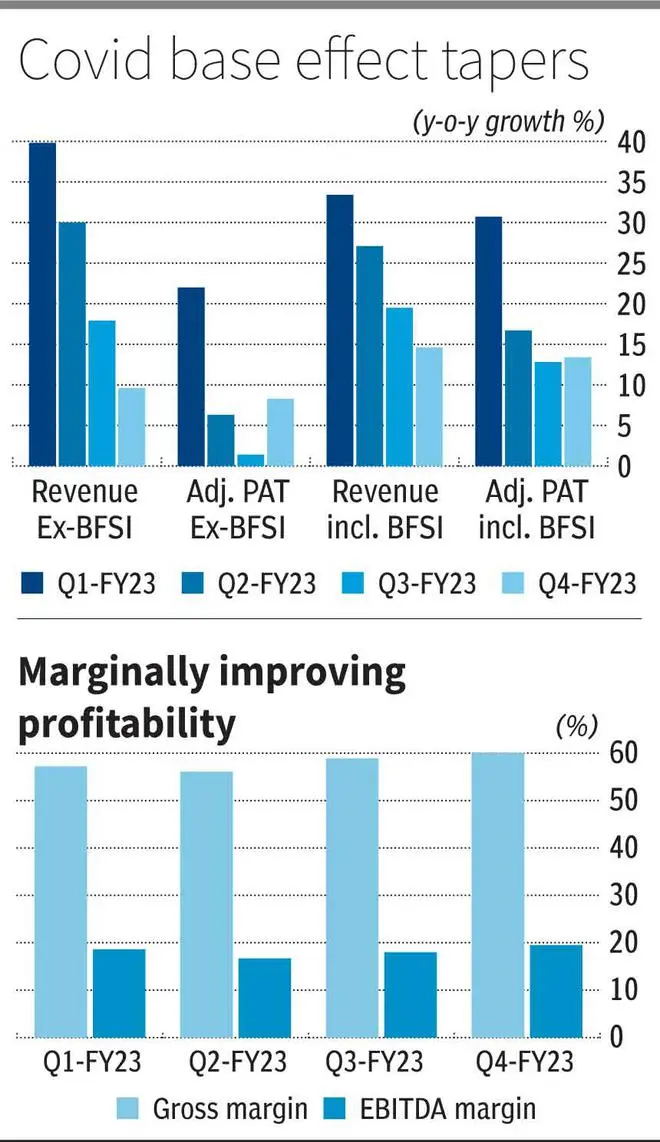

The initial set of Q4 results of 186 companies until April 27 shows that unlike the first three quarters of FY23, India Inc’s revenue and profit growth (year-on-year) have moderated to single digits at 9.6 per cent and 8.3 per cent, respectively (excluding BFSI).

However, there is good news on the margin front. The gross margin, which has trended up over the last four quarters, stood at 60.1 per cent in Q4, but was still off pre-Covid levels of 62-64 per cent.

EBITDA margins, too, have inched up. Despite a moderation, adjusted PAT growth at 8.3 per cent YoY was in line with revenue growth. In contrast, earnings growth lagged revenue growth in the first three quarters of FY23.

Strong numbers from banking, auto

Many of the initial set of numbers have come in from the BFSI vertical and these companies have reported strong top-line growth (28 per cent YoY). It is amongst a few sectors witnessing a higher traction compared to Q3FY23 (24 per cent YoY growth in revenues) as well. Thus, with BFSI, the top-line growth looks more robust at 14.6 per cent .

Demand growth in automobiles, at perhaps the peak of the cycle, is also strong at 19 per cent YoY. The IT sector also reported 16 per cent YoY growth, though the outlook is weak. The metals, consumer durables, and pharma scorecard on the aggregate numbers remains to be seen.

Also read: Banks end FY23 with a robust 15.4 pc credit growth

Commodity cool-off taking time

Crude and a wider basket of commodities represented by the Bloomberg Commodity Index have corrected by 16 and 30 per cent, respectively, in the last year. However, though gross margins edged up, management commentary indicates that most companies are still on ‘expectation’ mode for commodity price softening.

Consumer facing industries ranging from HUL to Nestle or Voltas or even Maruti Suzuki have reported gross margin contraction in Q4FY23 because of their raw material baskets.

This implies that while the steep inflation in input prices witnessed last year may have slowed down, contraction is not yet happening at the same pace.

The sharp rupee depreciation at seven per cent in the last year further impacted companies that import raw materials, offsetting any decline in the dollar price of the commodity. Companies are also reporting strong competition in demand for raw materials — supporting the slower pace of correction in input material costs.

Mixed outlook

The initial results indicate that revenue growth from here on will have to factor a robust base year performance, which was in the past helped by the low Covid base of FY21.

Besides, though there are signs of margins improving, the way forward remains to be seen. In the meantime, sectors with high competitive intensity may sacrifice margins for growth in the short run. This may play out prominently in the FMCG, consumer durables and realty sectors. Due to these factors, margin expansion in the short term is not a given.

The Nifty50 is trading at 18.9 times one-year forward earnings (Bloomberg consensus) — in line with its last 10-year average. The index returns have also been flat in the last one-and-a-half years. From earnings growth under-performing revenue growth in the last two years, this quarter has finally seen both moving in tandem.

While this is a positive takeaway from the early bird Q4 results, what is important is whether earnings over the next few quarters meet current consensus expectations, given the ongoing slowdown concerns.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.