The follow-on public offer (FPO) by Adani Enterprises (AEL) has been off to a rocky start, with serious allegations from an overseas short-seller emerging on the eve of the issue. With the AEL share price trading 11-15 per cent below the offer price of ₹3,112-3,276, the FPO, which is open between January 27 and 31, attracted very low subscription on the first day.

Offer details

AEL intends to raise ₹20,000 crore through this offer, with 50 per cent of the offer price to be paid on subscription and balance via subsequent calls, to be decided later. Of the offer proceeds, about ₹10,800 crore will go to fund capital needs of AEL’s subsidiaries in green hydrogen, airports and expressways, while about ₹4,100 crore will go to retire borrowings of the company and its subsidiaries.

The offer is in a price band of ₹3,112 to ₹3,276, with a 50 per cent QIB reservation and 35 per cent set aside for retail investors. Post offer, the promoter’s stake is expected to fall from 72.63 to 68.94 per cent (which is still quite high), while public holdings will rise from 27.37 to 31.06 per cent.

Logically, it doesn’t make sense for an investor to subscribe to an issue of new shares from a company at a premium to its market price, although in this case investors need to pay only 50 per cent of the asking price now. But in this analysis, we have ignored both the Hindenburg report (which we can’t verify) and the recent stock price reaction to it, to analyse whether the current fundamentals of the Adani flagship justify buying the stock now.

After an analysis of its financials, we believe that investors would be better off avoiding the AEL stock now. The primary deterrent is the stock’s unsustainable valuation. At its current price, AEL trades at a price to book valuation of 9 times (10.5 times at offer price) and a P/E of 168 times (195 times) the six-month annualised earnings for FY23. AEL’s share price is significantly out of sync with its fundamentals.

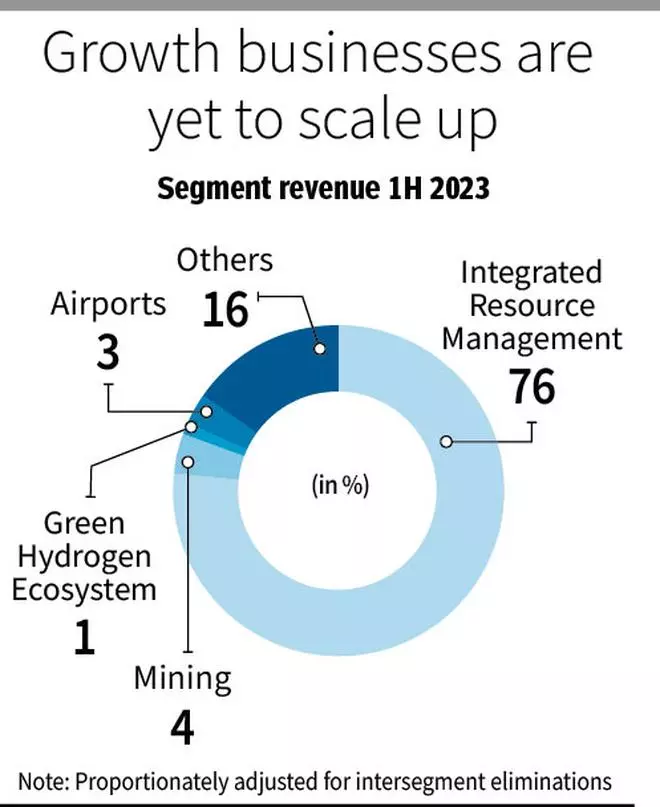

From pre-Covid highs of February 2020, the stock of Adani is up about 11 times. During the same time, its net worth is up 1.9 times while its earnings (annualising six-month FY23 earnings) are up 1.6 times. This disconnect between share price growth and growth in fundamentals is unsustainable for any company, leave alone one in which the business mix is dominated by businesses that have high linkages to economic cycles. Two, a significant 76 per cent of AEL’s revenue in the first half of FY23 was from its ‘Integrated Resource Management’ segment, where the primary business is sourcing and delivering imported coal to thermal power customers in India. This is typically not a business that commands high valuations.

Coal India, which is into mining and supplying coal from domestic sources, saw its net worth going up 1.68 times and earnings increasing by 1.8 times from FY20 to now (1H FY23 annualised). But in the same time span, Coal India share price was up a mere 1.3x.

Having said this, the primary attraction for investors betting on the AEL stock appears to be the host of emerging businesses it has seeded in recent times. These range from setting up a green hydrogen ecosystem from scratch to forays into data centres and airports. But these new businesses will remain cash guzzlers, requiring capex funded by debt or equity raise (like this FPO) before they generate decent growth. It may be quite a few years before any of these ventures can scale up to make a dominant contribution to AEL’s business mix.

Three, AEL’s relatively high leverage with low interest coverage ratio at a time of rising rates (even without factoring in what recent allegations can mean for AEL’s global fund-raise plans) can make capital raise more challenging in future, which can impact AEL’s liquidity or ability to invest. Its FY22 interest coverage ratio was at a fairly low level of 1.37 times. In the first half of FY23, however, driven by buoyancy in commodity-related earnings, the cover improved to 1.7 times. Given the cyclical nature of commodity earnings, this is not yet a cause for comfort. However, AEL’s debt/equity ratio is within reasonable limits at around 1.2x as of September 30, 2022. While this will see an immediate decline on the retirement of debt with FPO proceeds, it needs monitoring as future investment plans may result in increasing debt.

Finally, most of the company’s new business forays come within the ambit of heavily regulated businesses which require government support. The risk of policy changes that can adversely affect performance/profitability is thus high. AEL’s current valuations do not reflect these risks.

Business, prospects and challenges

AEL is a sprawling conglomerate with multiple unconnected business operations. Although Reliance too has unconnected businesses, in the previous decade it had a very healthy cash cow in the form of its main refining and petro-product business to fund its diversifications into new growth businesses. Unfortunately AEL doesn’t have such a cash cow.

AEL’s business spans coal trading, mining, FMCG (Adani Wilmar), solar manufacturing, airports, roads, data centres and green hydrogen. Barring coal trading, FMCG and to a lesser extent airports and roads, the company’s other businesses are small at an absolute level or at an industry level. The other businesses reflect big ambitions, but right now what investors have is just a business plan in search of actual execution. Success in these businesses is not guaranteed and will require multiple elements falling in place over the next few years.

For instance, a substantial portion of the FPO RHP document focusses on the science and opportunity of green hydrogen. The company intends to use 50 per cent of the FPO proceeds (total ₹20,000 crore) for capex relating to its green hydrogen ecosystem, airports and roads forays. Of this, plans to invest $50 billion (₹4.1 lakh crore) in the green hydrogen ecosystem over the next 10 years suggest that this foray may take up the lion’s share of the FPO. Green hydrogen refers to producing hydrogen using water and renewable energy and hence is deemed environment-friendly. If green hydrogen is developed successfully, it can reduce India’s import bill (currently hydrogen is produced using natural gas – grey hydrogen) and also enable it to meet its climate goal commitments.

But the important thing to note here is that, without significant subsidies, a green hydrogen business model is currently not commercially viable in India on its own. The current cost of producing green hydrogen is nearly twice as expensive as grey hydrogen. Success depends entirely on government support and subsidies, which are in the drawing board stage with the Government only recently approving the National Green Hydrogen Mission. High subsidy dependence apart, numerous execution challenges are ahead, including the need for construction of massive new renewable energy capacity and facilities for safe transportation of hydrogen. The company plans to expand in the promising data centre business as well. But this business is, again ,nascent. While it plans to build data centres with aggregate capacity of 1,000 MW, the company’s very first data centre with 17 MW was set up in October 2022 — there’s a long way to go before investors start assigning value to the business.

AEL has strong presence in airports, including the control of the flagship Mumbai Airport. However, the revenue contribution of airport’s business to total revenue is a mere 3 per cent. GMR Airports Infrastructure, which has a marginally higher market share than Adani Airports, is valued by the markets at ₹22,000 crore. Similar valuation for Adani Airports can be deemed reasonable on a relative basis. It is not clear what markets are assigning for the same as against AEL’s total current market cap of ₹3.15 lakh crore.

Besides these, AEL also plans to grow its mining, integrated solar modules manufacturing and other businesses (petrochemicals, copper, strategic military and defence, digital super-app). It is tough to assign a valuation to these businesses, with many of them currently in a nascent stage.

Financials

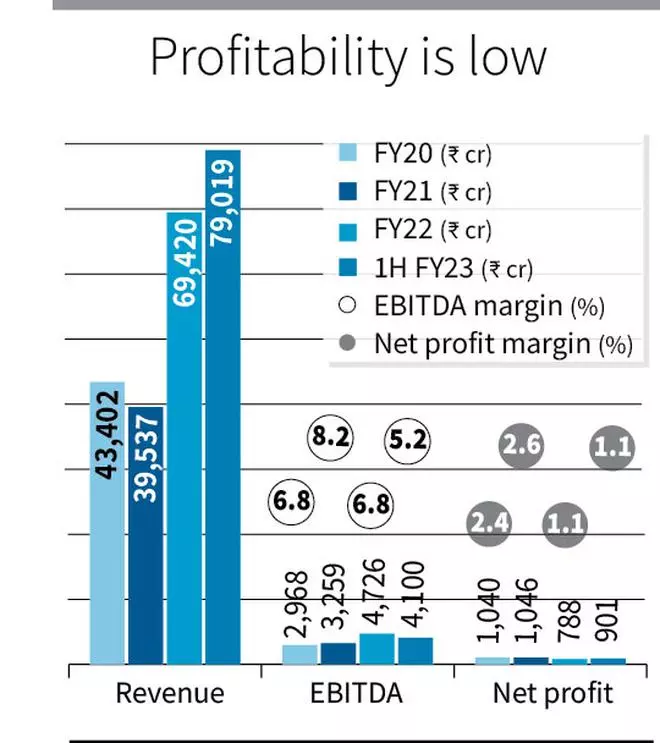

During FY20-FY23 (six months annualised), AEL’s revenues, EBITDA and EPS have registered strong CAGRs of 54, 40 and 17 per cent respectively. But extrapolating this to future is difficult, not only due to the cyclicality of the resources business, but also due to the significant changes expected in the composition of revenues and profits owing to new business forays.

In 1H FY23, AEL reported revenue of ₹79,019 crore, up from ₹25,796 crore in 1H FY22. EPS was at ₹8.23, up from ₹4.40. While the increase is significant, it needs to be noted that it is primarily driven by its coal trading business. The profitability was accordingly low with EBITDA margins at around 5.2 per cent in 1H FY23.

Between March 2020 and September 2022, AEL’s total debt increased three times. Though AEL’s total borrowings stand at around ₹43,000 crore, it has reported negative free cash flows in recent years. Based on the company’s utilisation plans of FPO proceeds, debt can reduce by about ₹4,000 crore in the short run. But whether this will sustain over time given the capex-heavy forays remains to be seen. Cash and cash equivalents on the balance sheet are fairly low for a company of its size at just a little over ₹1,000 crore. While AEL does not own too many liquid or quoted investments, its 44 per cent stake in Adani Wilmar is worth about ₹30,000 crore at current market prices. As per its RHP, the company has 184 subsidiaries, which makes its aggregate capitalisation, debt position and business structure quite complicated to decipher.

Overall, AEL’s current financials buttress the view that much of the stock’s premium valuation is derived from the hope that its ambitious new business forays will take off over the next few years. But the risk-reward equation appears unfavourable at present for retail investors to take that long shot.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.