Speciality chemicals stocks have corrected in line with the rest of the market from their peaks reached in the period October 2021 to January 2022. The cost of raw materials, which had been increasing from earlier quarter, impacted the EBITDA margins by 200-500 bps in 3QFY22, triggering the correction from dizzying heights. The fourth quarter results should further accentuate the impact of raw material costs on margins. The ability of individual companies to pass on the increases will be keenly watched differentiating advanced chemicals producers from commodity ingredients producers. On the top-line though, the companies have reported strong revenue growth into 3QFY22 and are expected to carry the revenue momentum of the last five years into the fourth quarter as well. This points to an intact long-term story for speciality companies, which has been the bedrock of valuation re-rating for the sector in the first place.

Long-term thesis intact

One theme that was building up from pre-Covid times was the surge in demand for speciality companies. First, prior to the current expansion phase, despite domestic raw material availability (benzene, ethylene and other petro-chemicals from refineries) and growing demand from end-user industries (pharma, agro-chem, and consumption), India was a net importer of many advanced to intermediary chemicals such as PVC, acetic acid, and methanol, for instance. Second, with China mothballing chemical plants on environmental concerns, domestic speciality players started adding capacities to keep domestic production going. Last, in keeping pace with economic growth the chemicals demand also improved in India and not just quantitatively. From base chemicals such as paper, agro-chem, and dyes the demand for textiles, fragrances, surfactants, and other advanced ingredients started increasing. Companies leveraged their supply chain credentials, built over a decade, to expand their offering. The last two years also witnessed higher government impetus to produce domestically with sops on land, taxes and production-linked plans. As a result, import substitution and supply chain diversification to domestic firms gained steam as supply chain disruption persisted from Covid times.

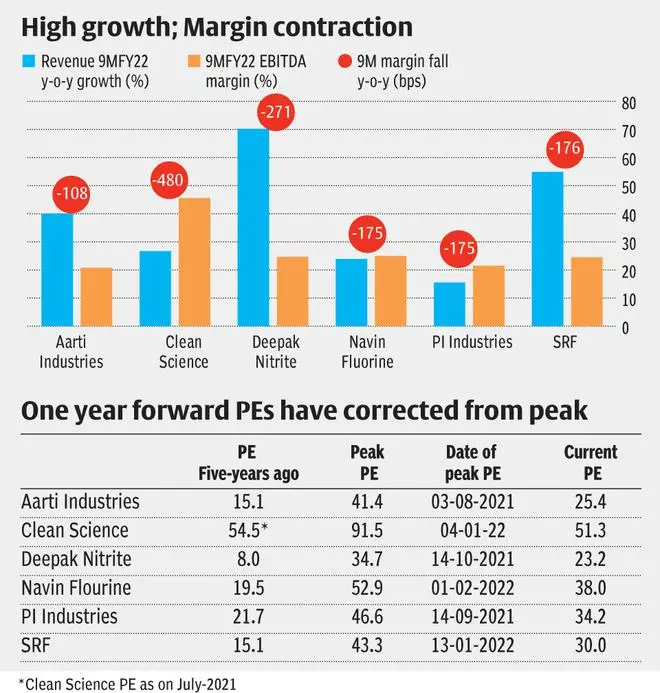

Companies across speciality chemicals, CRAMS and ingredients are posting their highest revenues with each passing quarter and this trend continued in the third quarter of FY22 as well. Starting from industry leaders SRF and Aarti Industries to recently-listed companies such as Clean Science and Ami Organics, companies reported average 40 per cent growth in revenues in 9MFY22 over the Covid-impacted base period of 9MFY21. This is on the back of both commercialised capacities added in the last few years providing volume growth (10-15 per cent) and pricing growth supported by strong demand.

The companies continue to be in investment mode. Clean Science not only added new product facilities and expanded capacities of existing products as of Q3FY22, but has also announced higher capex for next year. Similarly, SRF has added significant capex and the guidance for FY23 stands similarly higher than in FY22. Deepak Nitrite has plans to raise capital for expansion, while Navin Fluorine is investing into multipurpose plants which can later add to its base production in addition to its new CRAMS plant commercialised.

Challenges ahead

The persistent overhang to the growth story will be the return of Chinese investments in chemical sector, which in most cases must be greenfield investments. But the overhang is significantly tempered by the 7-8 years required for commercialisation, investments into products higher up the value chain by the Chinese and captive consumption.

Margin pressure is another challenge. Companies reported higher costs, starting from Q2FY22 to Q3FY22, where the margins contracted by 200-500 bps even as price increases were passed on to an extent. With logistics, power, petrochemical raw materials continuing to peak into the fourth quarter of FY22 and analyst expectation of sticky inflation, margin contraction can continue. But the high EBITDA margin base of 25-30 per cent of speciality chemical companies can cushion the impact.

Valuations reflect optimism

The optimism is more than reflected in soaring valuations. The valuations of key stocks have corrected from their peaks in October 2021 (30-45 times one-year forward earnings) to 25-35 times currently. But they have still doubled in the last five years. The upcoming fourth quarter results can differentiate companies. Advanced ingredients suppliers can pass on price increases above a certain range and irrespective of contracts signed. This ability will be awarded a premium in the current inflationary markets. Management commentary post-results can also indicate the company’s views on expansion in a period when interest rates are expected to increase along with an increasing uncertainty in global macroeconomic indicators.

As companies face high inflationary period, the high valuations will ensure that any operational miss by companies will result in large, outsized corrections. With a quantum of demand shifting to Indian producers of speciality chemicals, the longer-term investment opportunities can be found in short-term corrections for specific stocks.

Agro-chem, pharma and textile chemicals companies with export potential (SRF, Ami Organics and PI Industries) hold promise for investors. CRAMS operators with established credentials (Navin Fluorine) and companies leveraging import substitution (Deepak Nitrite and Clean Science) also can be good addition to the portfolio on corrections.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.