Aether Industries (Aether), a nine-year-old speciality chemicals manufacturer with strong growth credentials, is the latest from the industry to come out with an IPO. The experienced promoter group (earlier co-founded Anupam Rasayan and no continuing relationship now) has established an R&D intensive speciality chemicals operations. The company has delivered FY19-22 revenue CAGR of 43 per cent(9MFY22 annualised) in the early stages of its lifecycle. The product portfolio aimed at benefitting from limited competition is set for continued expansion with fresh inflows of ₹627 crore from the IPO (debt clearance ₹138 crore, capex ₹163 crore, working capital ₹165 crore and for general corporate purpose). Balance ₹181 crore of the issue is an OFS. While operational and product prospects hold promise, the IPO valuation is also priced in a premium range. Hence, the offering can be avoided as the high valuation may not leave much value to investors.

R&D driven operations

Aether commenced operations in the year 2013, but significant revenue generation started in 2018 (which it calls the second phase) as till then it was strengthening its R&D and infrastructure base. The company focusses on process research, blending chemistry with automation to achieve scale. The process focus and presence across pilot testing stage to commercial production has allowed the company to operate CRAMS (Contract Research And Manufacturing Services) and contract manufacturing divisions as well, which have contributed 7.4 and 21.8 per cent respectively to 9M FY22 revenues. Aether has historically supported around 15 CRAMS projects at any point of time. These projects are in advanced stages of pre-commercialisation research across agrochem, performance materials, oil & gas and coatings. A quarter of these go through to Aether’s Contract Manufacturing segment, which provides dedicated manufacturing capabilities for commercialised molecules and providing IP protection to clients . The essentially large-scale manufacturer presenting research solutions makes for a better client engagement apart from diversification benefits as Aether is amongst the few with process research capabilities in India, especially in the non-pharma space. This wide and proven delivery capability has allowed for comparatively faster scale up with international clients, which otherwise extends around a decade in speciality chemicals.

Limited competition product profile

Large scale manufacturing accounts for 70 per cent of company’s revenues. Aether chooses products based on it being the only producer domestically for the product, involves complex chemistry or technological barriers (at least four steps in production) and sufficient demand scenario for the product. Aether has been the only manufacturer in India even for few products launched in 2015 period or recently launched products and expects to filter products on similar lines for future expansion as well. The average volume growth of 32 per cent in the last two years (mostly in line with expanding facilities) has been enabled by Aether replacing imports from China, Europe, and Japan for its products in the domestic and even international markets (average export revenue of 50 per cent ).

Aether generates close to 62 per cent of revenues supplying advanced intermediaries to pharmaceuticals and 22 per cent from agrochemical (9M FY22). Within these sectors, supplying intermediaries to old molecules which have been genericised for some time puts an upper limit on the margin profile of the products for Aether. The gross and EBITDA margins have ranged between 45-51 per cent and 22-28 per cent respectively for Aether which are comparable to mid-section of the peer range.

Aggressive expansion plans

Aether expanded installed capacity at 27 per cent CAGR from March 2019 to December 2021, to 6,100 MTPA. The company will utilise from fresh proceeds ₹163 crore and internal accruals for expansion in its third site, which should increase installed capacity to around 15,000 MTPA in the next two-three years. The company has reported doubling the R&D capacity and plans to increase it further as well to support the expansion plans. Aether has listed five APIs or end products whose intermediaries will be developed in the next one year as part of portfolio expansion, which also meet the low competition and higher manufacturing barriers of the company. Existing product and new product expansion should be sustained by the new capex. The company is also intent on expanding beyond pharma and agrochem end-user industries with the expansion plans. Aether reports a larger land bank availability near the current facility for further expansion beyond the next two years as well.

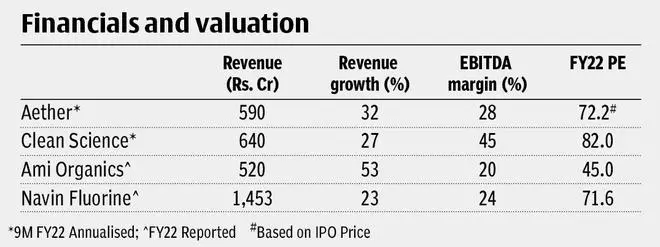

Financials and valuation

Aether reported 32/72 per cent YoY growth in 9M FY22 revenue and profit respectively. . The top line growth is largely volume driven with a 6.8 per cent CAGR in price growth in the period FY19-FY22 (9MFY22 annualised). The faster bottom line growth has been on account of improved efficiency in operations as price growth has been nominal. EBITDA margins improved to 28 per cent by December-2021 quarter from 23 per cent in FY19.

Aether’s debt to equity has improved from 3.3 times on March-2019 to 0.7 times on December-2021 which can further decrease from the fresh proceeds and the company management expects to be debt free post the IPO.

Aether is priced at 72 times annualised 9M FY22 earnings, which is at the higher end of peers. Such high valuations may be justified only if the company is able to deliver performance similar or better than the what the company delivered in the last three years. As the company matures to a larger revenue base and in a macro environment likely to be burdened by higher interest rates, sustaining the growth momentum and avoiding execution risks, may be challenging.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.