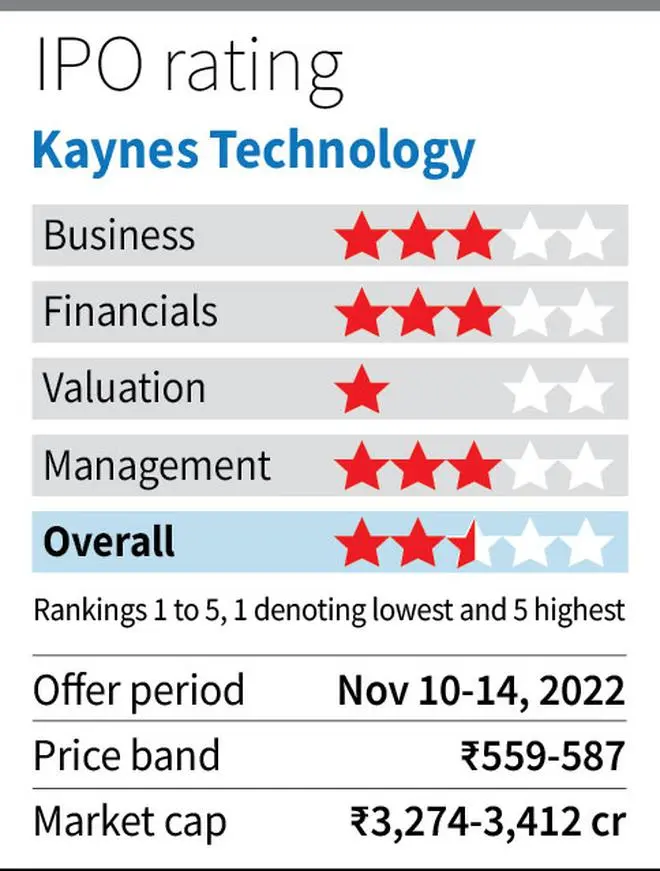

The IPO of Kaynes Technology (Kaynes), which opened for subscription on November 10, is on till November 14. The issues size of around ₹ 850 crore consists of a fresh issue of ₹530 crore, the rest being offer for sale by promoter and another investor.The company intends to use the proceeds from fresh issue for capex/capacity expansion, repayment of borrowings and funding working capital requirements. The promoter shareholding, which is at 80 per cent now, will reduce to 64 per cent post issue.

Kaynes is in the business of integrated electronics manufacturing. While the growth prospect is interesting, at the upper end of the IPO price band of ₹559-587/share, Kaynes is valued at very expensive levels. On post issue shareholding basis, the valuation works out to 82 times FY22 PE and around 87 times annualised June Q FY23 earnings. Such a valuation more than adequately factors growth prospects and leaves no margin of safety for investors. Hence long-term investors can give the IPO a miss.

Business

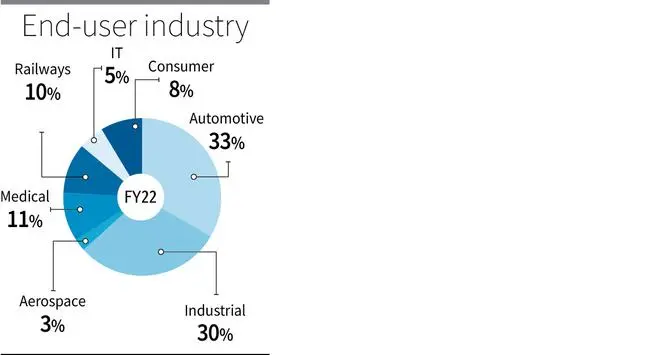

As an integrated electronics manufacturing player, Kaynes has capabilities across a broad spectrum of electronic system design and manufacturing services (ESDM). It has experience in providing conceptual design, process engineering, integrated manufacturing and life cycle support for major players across multiple industries (see infographics). It operates out of eight manufacturing locations in the country. Some of the products amongst many supplied by Kaynes are cluster printed circuit board assemblies, electronics for automotive lighting, street light controllers, engine control panels, energy meters, wired and wireless headsets, etc. Relative to sector, the company has a reasonably diversified customer base with top 10 customers contributing to 51 per cent of revenue. Around 20 per cent of company’s revenue comes from exports.

Prospects

While ESDM players originally started off as contract manufacturers a few decades back, today many of them partner with original equipment manufacturers (OEMs) right from product design and prototyping/testing phase, thereby increasing their value in the overall product life cycle. Global ESDM industry was at $804 billion in 2020, with India’s share at a minuscule 1.8 per cent. China leads the pack with a share of 45 per cent, followed by the US at 16 per cent. As per a Frost and Sullivan report, the market size is expected at $1,002 billion in 2025, with possibilities that India’s contribution can be as high as 8.1 per cent, implying a CAGR of 41 per cent for the industry. While this might be overly optimistic, the growth nevertheless can be good. Factors that work in favour are government push and incentives to promote manufacturing in India, domestic cost competitiveness (Indian wages 46 per cent cheaper than China as per a report), import substitution, China+1 strategy of global companies, etc.

Risks

Some of the key players in the industry in India besides Kaynes are listed players — Dixon Technologies, Amber Industries, SGS Syrma; and unlisted players like Bharat FIH, SFO Technologies, Avalon Technologies and Sanmina-SCI Technology. Bharat FIH and Sanmina-SCI are Indian units of formidable international players.

At the same time, this is also an industry with very high competition (domestic and established international players) and low margins. Global slowdown is also a near-term risk that may impact revenue and pressurise margins. Industries and companies with lower margins tend to experience higher volatility in earnings. Higher interest rates can also impact cost of working capital and impact profitability. Thus, growth prospects need to be considered along with these risks. Dependence on imports for key raw materials till India is able to set up domestic capacity for the same is also another risk. For example in FY 22, imported raw materials accounted for 64.46 per cent of total purchase of raw materials for Kaynes.

Financials and Valuation

In FY22, Kaynes reported revenue from operations of ₹706 crore and net profit of ₹41.6 crore (net profit margin of 5.8 per cent). During FY20-22, revenue and profits grew at a CAGR of 38 and 111 per cent respectively. Profitability improved from a combination of operating leverage as well as lower interest costs. As compared to peers Kaynes has better profitability. As per its presentation, while it reported EBITDA margins of 13.3 per cent in FY22, the same for some of its key peers is in the range of 2.7 to 11 per cent.

For June Q 2023, Kaynes reported revenue from operations of ₹199 crore (28 per cent of FY22 revenue) and net profit of ₹10 crore (24 per cent of FY 22 profits). At the end of the quarter, the company had a stronger order book of ₹2,266 crore (3x FY22 revenue).

In the absence of any global shocks, the company’s growth can continue to trend well but its valuation at 82 times FY22 earnings makes the offering unattractive. Peer SGS Syrma, which came out with its IPO recently in August, is trading at 67 times FY22 earnings. While peers also trade expensive, they don’t appear to factor business risks adequately.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.