The IPO of TVS Supply Chain Solutions (TVS SCS) opens today - August 10, 2023 - and closes on August 14. The issue size is around ₹880 crore which comprises ₹600 crore of fresh issue and ₹280 crore worth offer for sale. Most of the proceeds of the fresh issue will be used for repayment of certain borrowings (₹525 crore) of its UK subsidiary - TVS LI UK - and rest, for general corporate purposes.

The company is differentiated from the regular 3PL (Third Party Logistics) service providers in the industry and offers end-to-end solutions to clients, including regular transport / warehousing management and customised services such as Sourcing & Procurement and in-plant logistics management.

At the upper end of the price band of 187-₹197, the market capitalisation of the company will be around ₹8,746 crore. The enterprise value of the company including cash from fresh issue would be ₹10,297 crore; the EV/EBITDA of the company post issue (EBITDA at the end of FY23) will be 14.5 times.

At 14.5 times trailing EV/EBITDA, the valuation is at the upper end of the industry range (excluding Delhivery which was unprofitable in FY23) and may not be inexpensive. At the same time, the pricing is not expensive given the growth prospects, rich management experience and strong portfolio of strategic acquisitions. The good track record of TVS Group companies in managing businesses and in corporate governance can also justify some of the valuation premium. Given these factors, long-term investors can subscribe to the issue.

Business and Prospects:

TVS Supply Chain Solutions is a part of the TVS Mobility group. The company is around 16 years old and has managed large and complex supply chains across multiple industries in India and select global markets through customised tech-enabled solutions.

The logistics market in India was valued at $435 billion in fiscal 2022 and is projected to grow to $541 billion by fiscal 2027 at a CAGR of 6 per cent. The supply chain solutions market is at a nascent stage in India, valued at $10.5-$10.7 billion in 2022 and is expected to grow at a CAGR of 22-25 per cent to $29-$30 billion by fiscal 2027. This offers good opportunity for organised and tech-driven players like TVS SCS to gain market share.

The services of the company can be divided into two broad segments - Integrated supply chain solutions (ISCS) and Network solutions (NS). The services under the ISCS segment include sourcing and procurement where it forecasts and procures inventory for the client, integrated transportation where they plan the shipping and optimise costs.

It also offers logistics operation centres where TVS SCS will provide production support and in-house logistics, finished goods, aftermarket fulfilment and supply chain consulting. The NS segment include global forwarding solutions, which involves managing end-to-end freight forwarding and distribution across ocean, air and land, warehousing and at port storage.

The key differentiator of TVS Supply Chain Solutions is the use of technology to provide solutions to its client’s supply chain process. It offers solutions like demand forecasting, inventory planning and production, procurement management, network optimization, visibility, and supply chain agility to handle evolving needs.

The average length of relationship with its top 10 customers is 10.9 years for ISCS and 10.5 years for NS. The clientele of the company includes big names like Daimler, Sony, Panasonic, Hyundai Motor (India) ltd, Hero Motocorp, TVS Motors, Ashok Leyland.

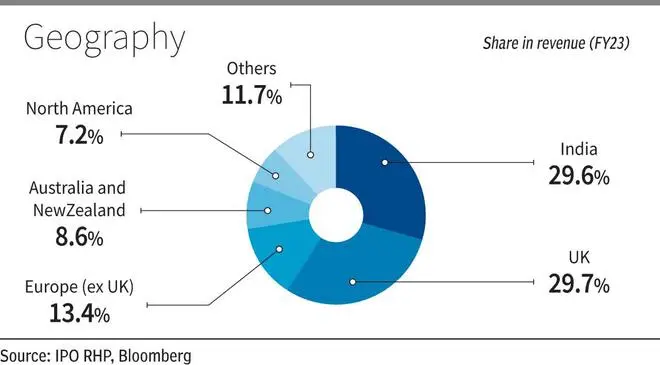

TVS Supply Chain Solutions has a global footprint, 29.57 per cent of revenue in FY23 came from India, 29.67 per cent from UK,13.37 per cent from Europe, 8.59 per cent from Australia and New Zealand, 7.15 per cent from North America and rest from other geographies.

The company’s customer base is quite diversified and is expected to guard it against cyclicality in any sector. 35.35 per cent of the revenue for the company comes from Industrial clients, 23.17 per cent from clients in automobile sector, 11.99 per cent from tech and tech infra, 11.74 per cent from consumer goods, 5.77 per cent from rail and rail utilities clients, 1.7 per cent from healthcare segment and the remaining, from other industries.

Financials:

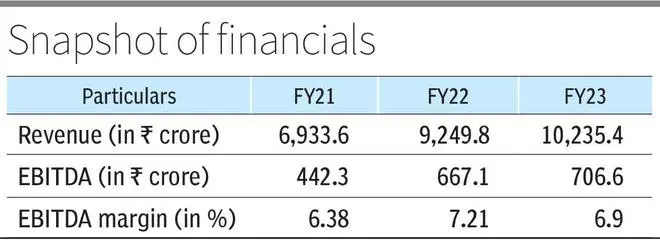

The company clocked revenue CAGR of 21.5 per cent (FY21-FY23) whereas the EBITDA of the company grew at a CAGR of 26.4 per cent for the same period. The revenue of the company in FY23 was ₹10,235.4 crore while EBITDA was ₹706.6 crore, which is 6 per cent higher YoY. The EBITDA margin of the company is 6.9 per cent which is marginally lower by 31 basis points YoY. The net profit of the company in FY23 was ₹41.76 crore whereas in the previous period company was making losses.

This article has been corrected for market capitalisation data which was earlier mentioned as ₹7,769 crore. Consequently the EV/EBITDA has also been corrected to 14.5 from 13.2.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.