The revival in economic growth post the pandemic, the booming e-commerce activity, as well as the roll-out of the National Logistics policy has put the spotlight on logistics stocks in recent times. Transport Corporation of India, a player in this segment, has been on a climb, gaining 152 per cent since May 2021. Good business outlook for the more profitable supply chain and shipping divisions are a positive. Efforts to increase share of LTL share in the freight segment too bode well for margins. However, considering the run-up in the stock and the mature business segments it operates in, the upside potential from hereon could be limited. The valuation too is in line with long-term historical averages. The stock now trades at a 12-month forward P/E of 13.9x vs. 5-year average of 14x. Existing investors can continue to hold the stock.

Business divisions and performance

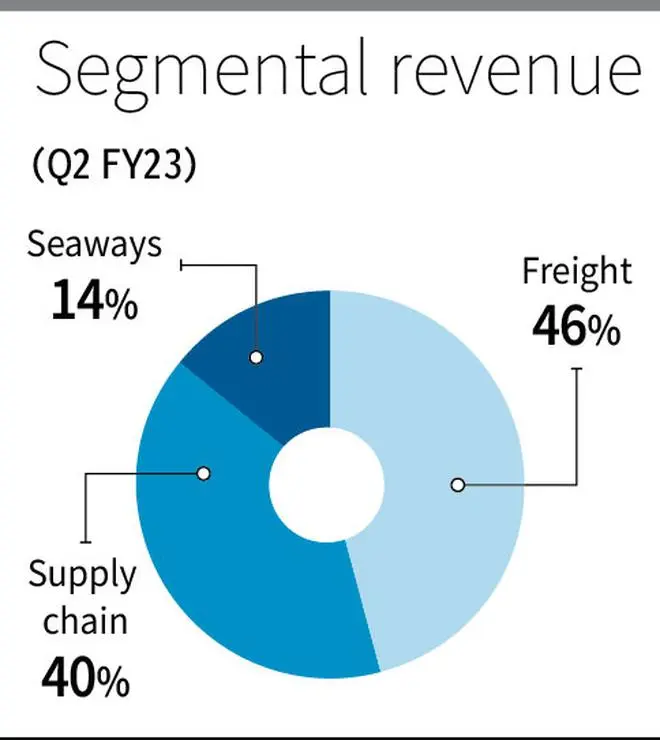

Transport Corporation of India basically has three business segments — freight, supply chain services and seaways services.

In the freight division, TCI provides both Full Truckload services (FTL), less than truckload (LTL) services and customised solutions for its clients. This is the traditional form of transport and contributes to 40-42 per cent of the total revenue for TCI. However, freight service is a low-margin high-volume business and hence the EBITA margin in this segment is only 4-5 per cent. In this segment LTL consignments are 35 per cent and the remaining is FTL.

LTL consignments consume less space and therefore the amount is charged for the space used ; But since the delivery will require more planning, halts, unloading operations, the per unit and per mile cost will be higher than FTL. Net-net, LTL provides scope for higher margins. The management believes that by the end of 2022-2023 LTL share will move up to 40 per cent.

The supply chain division, unlike freight services, provides end-to-end service such as warehousing, distribution centres, cross docking, yards, inbound and outbound logistics. The company has 13 million square feet storage area under management in FY22 and 250-acre yard area under management. The company mainly serves automobile, healthcare, chemical, retail and consumer products companies. This division contributes 40-42 per cent of the total revenue. Considering the end-to-end service provided, its profitability is higher, with EBITDA margins of 10-11 per cent.

The supply chain services saw a 27 per cent rise in revenue in Q2 FY23 YoY and around 15 per cent rise in EBITDA mainly due to pick-up in the automobile sector, which is being transported in trains.. To further cash in on this segment, the company plans to invest in a hub-and-spoke model for the finished goods where the bulk movement will happen by rail and then the spoke movement will happen by road. Since transportation by rail is cheaper than road, this system is expected to help manage costs better.

TCI is a dominant domestic cargo carrier, it has six domestic coastal ships with deadweight tonnage of 77,597 and it serves 7 out of 13 ports of India and owns more than 8,000 multipurpose containers. This division contributes 12-14 per cent of the total revenue and has EBITDA margins in the range of 30-40 per cent.

The company is looking to add a new ship of around 30,000-35,000 tonnage, which it plans to acquire by 2024.. The management stated that it is currently receiving orders beyond capacity and therefore demand will not be a problem even after adding capacity.

Financials

Revenues grew in Q2 FY22 by 13.45 per cent year on year to ₹939.46 crore. Cost pressures led by fuel expenses impacted operating profits and margins., despite the company being able to pass on some of the costs. The EBITDA margin of the company in September 2022 was 11 per cent, about 2 percentage points lower than the September 2021 quarter. Net profits fell by 4 per cent YoY to ₹73.02 crore in September 2022.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.