Investors with a two-to-three-year investment horizon can consider investment in the stock of KRBL Ltd, which is India’s largest basmati rice exporter. The company’s flagship brand, India Gate, is the largest brand not just in India but also dominates in several markets — such as GCC region (Gulf Cooperation Council which includes Bahrain, Kuwait, Saudi Arabia, Oman, Qatar, United Arab Emirates), Australasia and other regions. Strong brand franchise and new product additions such as brown rice variants and pesticide-free variants should help the company sustain healthy growth over the next two years. The company operates on a contract farming model for sourcing rice and has established an extensive global distribution network. At the current price, the stock trades about 16 times its trailing twelve-month earnings of ₹23.9. We recommend the stock for investors with a moderate risk appetite and a holding period of two-to-three years.

We believe KRBL to be an interesting investment opportunity for five reasons.

First, KRBL is the largest exporter of Basmati rice in India, with strong presence in the home market too. With its flagship brand India Gate, which is the premium brand, the company has presence in over 90 countries. With the world’s largest milling capacity of 195 tonnes per hour, KRBL’s products are sold through over 5 lakh retail outlets across cities and towns in the country. KRBL, with a 32 per cent volume market share, is the leader in the traditional trade in the home market. In the modern trade, the company stands second with a 32 per cent share next to LT Foods.

In India, the unbranded market is significant and is also fragmented. The company’s distribution network is among the largest with over 500 distributors. It is further working to have a direct distribution in markets with population of over 1 lakh people. It is also using technology to streamline and strengthen its distribution and supply chain. The company is also scaling its digital presence.

On the exports front, KRBL is the leader in the GCC market, which accounts for almost 80 per cent of India’s export market. Of this, KRBL alone accounts for 56 per cent, which demonstrates its leadership here. Also, the company, with its mid-segment brand Unity, is targeting the unbranded market, which will aid market share gains in the medium term.

Second, KRBL is scaling presence in other markets such as Europe with the new pesticide-free variant, which should help the company achieve higher revenue from Europe. Likewise, it is strengthening presence in the Americas, which is an interesting and attractive market from realisation and profitability point of view. KRBL market share in Americas is currently at 9 per cent, implying that there is immense room for growth in the near to medium term. The company is present in dominant channels of trade and in the past year it has been consolidating its channel in key export markets and has onboarded seven new distributors for its international business.

Third, capacity expansion at its mills will help the company’s medium-term growth. KRBL is expanding capacity at three of its locations – Gujarat, Karnataka, and Madhya Pradesh. Gujarat facility is under construction, while in Madhya Pradesh land acquisition formalities are under process and in Karnataka, land purchase is in process. The plants in Gujarat and Karnataka are expected to go on stream in FY24, while the Madhya Pradesh one is expected to come on stream in FY25. With this, the company’s milling capacity should increase to 215 tonnes per hour from 195 tonnes an hour.

Four, the company’s focus on newer products with a health benefit narrative, such as brown rice, chia seeds, flax seeds and quinoa, coupled with focus on pesticide-free variants, will drive both its export and domestic business. The recently introduced 1886 and 1667 seed varieties are expected to bolster KRBL’s performance over the medium term, with the seeds expected to be handed over to farmers in FY23 sowing season. These seeds offer higher resistance to disease and pest, which will help KRBL produce chemical residue-free basmati rice — crucial to scale in markets such as Europe, the US, and the Middle East.

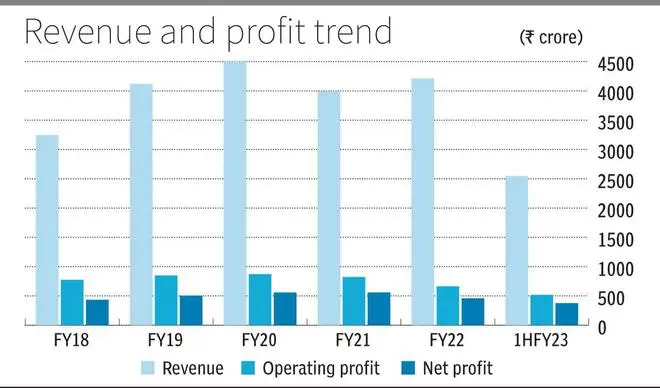

Finally, the strong balance sheet and higher profitability and reasonable valuation, relative to competition, add to the attractiveness of KRBL’s stock. KRBL’s operating profit margin is back to healthy 20 per cent-plus levels in 1HFY23, compared to 13 per cent in 2HFY22, thanks to resolution of issues in Saudi Arabia, appointment of new distributors, and the sharp increase in the realisation by 30-40 per cent, which compensated for the higher logistics and other costs. In 1HFY23, KRBL’s revenue grew 23 per cent to ₹2,547 crore while net profit grew 36 per cent year-on-year to Rs ₹377 crore.

The company’s margins are higher than the 2-3 per cent operating profit margin for Adani Wilmar (product basket includes other products such as oil, other cereals) and 10 per cent for LT Foods, which owns Dawaat Brand. Also, the company has minuscule debt at about 0.03 times its equity, while Adani’s debt equity ratio is about 0.4 times and the same for LT Foods was 0.6 times as of September 2022. Despite superior profitability and balance sheet, while KRBL trades about 16 times trailing twelve-month earnings, Adani Wilmar trades 119 times trailing earnings. LT Foods trades about 10 times its trailing twelve-month earnings.

Risks

Rising crude oil prices and resultant increase in logistics costs can have a negative impact on the profitability. Inflationary pressure in the economy and resultant shift to unbranded basmati also remains a risk, although the company is trying to garner share of the unbranded market through its Unity brand.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.