The Government’s increased focus on infrastructure and affordable housing can be seen as a positive cue for the cement sector. The demand for cement is estimated to grow 8 to 10 per cent in the current fiscal (as per CRISIL data). However, despite this growing demand, cement companies are finding it tough to improve their margins. Cost inflation is the culprit, which has led to an increase in the input prices even as companies are not able to hike prices due to competition. This has resulted in pressure on cement stocks this year, and long-term investment opportunities are likely to gradually open up as these factors play out.

Ramco cement is an old and consistent player with its turf being South India markets and now it is penetrating the eastern markets. The stock has corrected around 37 per cent from its all-time high in November 2021. The stock is trading at a one-year forward PE of 24.3x while its 5-year average is 24.3x (Bloomberg consensus). The one-year forward EV/EBITDA of the company is 13.5 x while its 5-year average is 13.8x. Although the stock is trading at its historical average, its long-term prospects merit attention and possible inclusion in your portfolio. Investors may accumulate this stock on 10 per cent dips.

Business prospects

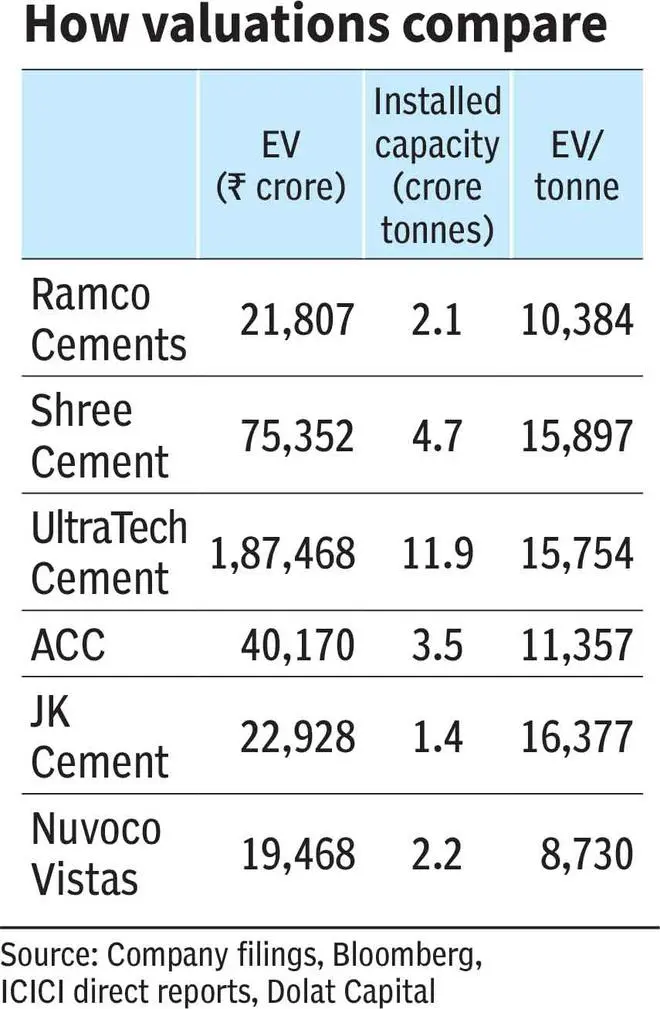

Ramco Cements is considered a major player in the southern region and is now increasing prescence in the lucrative Eastern markets as well. It has a total installed capacity of 21 million tonnes with its newly commissioned plant at Kurnool. . According to industry data from CRISIL, in FY22, Southern and Eastern markets accounted for 26 per cent of total demand each, adding up to half of total demand. For Ramco Cements, in Q1 FY23, the revenue share from Eastern markets was 30 per cent while in Q4 FY22 it used to be 18-20 per cent.

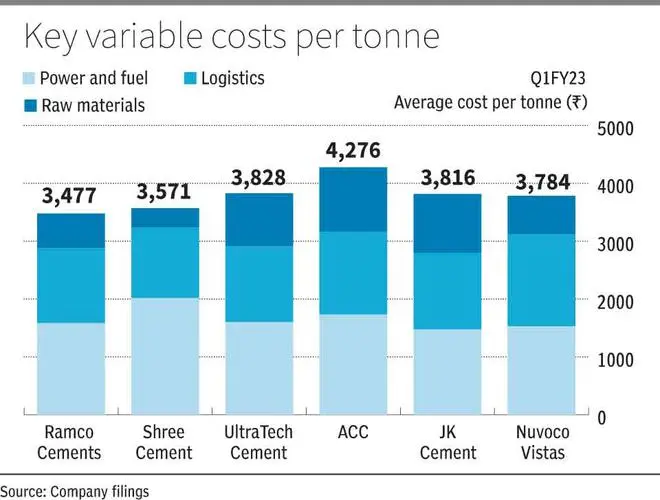

In Q1FY23, the major variable costs of the company were at the lower end as compared to industry range because pet coke forms a major part of its fuel mix at 54 per cent, 30 per cent being coal and the remaining, alternative fuels. Pet coke prices have further softened in recent times with domestic pet coke costing ₹16,000-₹18,000 per tonne in September 2022 while imported pet coke cost $180 per tonne (as per an Emkay report) while in June 2022 quarter the price was above ₹20,000.

The EBITDA margin of Ramco cement for Q1FY23 was 17.3 per cent, while peers of similar size like Nuvoco Vistas reported 14.1 per cent, and JK cement 18.5 per cent.

The company fulfils its 64 per cent of power requirements from Thermal, 19 per cent from Wind power and remaining from grid. It currently consumes part of its wind power and sells some to grid. It plans to use entire wind power which will help reduce the overall power cost. According to the company, it costs around ₹ 1 to manufacture one unit of power from wind and ₹ 7 per unit to manufacture from thermal.

According to the company management, at present, a price hike of ₹10-₹15 per bag will be enough for covering cost inflation while another ₹30-₹35 hike is required for the EBITDA growth. The next year (FY24) being penultimate year of election year there might be increased public spending and the required price hike may be possible. According to ICICI Securities data, in the month of October 2022, cement prices have seen a hike of ₹35 per bag in South and ₹15 in the East. If this trend sustains, and with gradual cooling of raw material prices, the company can improve its EBITDA growth along with revenue growth.

Recent financials

The sales volume of the company grew 55 per cent in Q1 FY23 to 3.31 million tonnes over Q1 FY22 when it was 2.14 million tonnes. Realisations contracted by 6.8 per cent. As a net result, revenue was up by 44 per cent at ₹1,785.64 crore. Due to impact of high input costs, operating expenses grew 70 per cent to ₹1,476.2 crore over Q1 FY22. EBITDA declined 17 per cent Y-o-Y to ₹309.34 crore, while net profit declined by 33 per cent to ₹113.27. The impact of higher costs and degrowth in earnings appear to be reflected to some extent with the over 30 per cent correction in the stock price ytd.

.

The company seems to be a bit higher on leverage side with its Net debt/EBITDA being 3x, but this is within comfort zone. .

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.