When market interest rates are ruling high, it makes sense for investors to lock into long-duration debt options for their 10-year plus goals. But for Indian investors, the choices are pretty limited. Popular options like the PPF or NPS lock in your money for 15 years plus and don’t allow exit at a time of your choice. If you directly buy government securities (g-secs) on the RBI Retail Direct platform, you only get regular income, the interest is taxed at your slab rate and liquidity is poor if you seek exit before maturity.

Long-duration debt funds such as Nippon India Nivesh Lakshya help investors with 10-year plus goals to lock into high yields, while enjoying anytime liquidity and better taxation.

Features

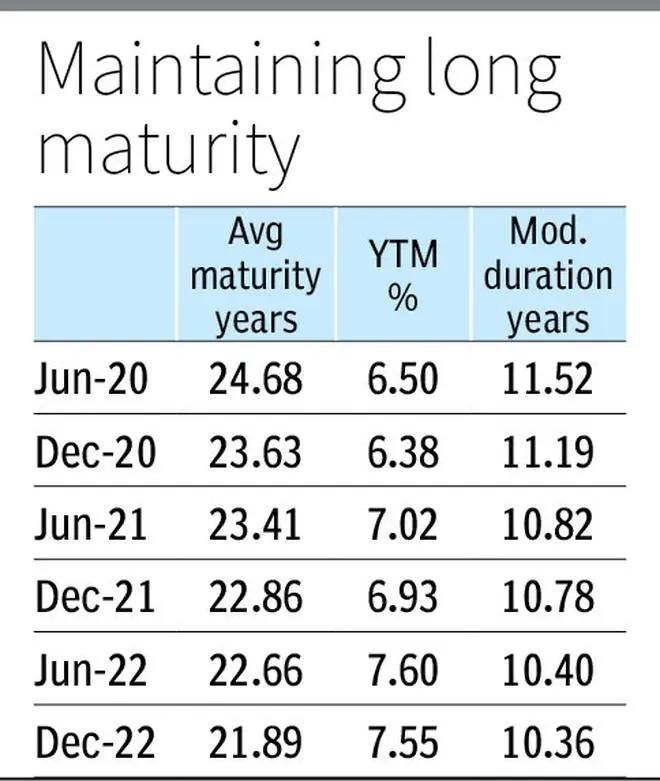

Nippon India Nivesh Lakshya is an open-end debt fund that invests only in long-dated central g-secs, such that its Macaulay duration is always seven years and above. In practice, the fund has consistently held a portfolio of g-secs with a 20-year to 25-year average maturity.

The fund doesn’t actively manage duration. It charges economical expense ratios, lower than actively managed gilt funds. The current TER (total expense ratio) of the regular plan is 0.53 per cent and direct plan 0.16 per cent.

Despite its portfolio of long-dated g-secs, this is an open-end fund, allowing investors to redeem units at any time in case of need. In the first three years though, investors are allowed to redeem 20 per cent of their units without any load and an exit load of 1 per cent is imposed on exceeding this cap. After the three-year holding, you are free to redeem any or all of your units without an exit load. These conditions are perhaps in place to discourage short-term trading in units given that long-dated g-secs are quite illiquid in the secondary market. As an investor, you should avoid before a three-year period, as you forego tax benefits and pay an exit load.

Why buy

Past rate cycles in India have topped out at 8-8.5 per cent (10-year g-sec yield) and bottomed out at 5-5.5 per cent. With current yields at about 7.4 per cent, we are closer to the top than the bottom of the present rate cycle. Generally, high points in the rate cycle are good times to invest in long-dated g-secs because you get the twin benefits of higher interest accruals throughout your holding period, along with the possibility of capital gains if rates fall in future. Given that it is quite difficult to catch the absolute top of a rate cycle, this appears a fairly good time to make lump-sum investments in long-duration debt funds. For investors who do not have lumpsums or are wary of wrong timing, SIPs can be considered too.

Also read: How the active versus passive scorecard looks for PSU equity funds

The current tax regime for debt funds allows investors to claim inflation indexation benefits on holdings beyond three years. This means that when you finally withdraw your proceeds from this fund to meet your goals, only returns over and above official inflation rates will be subject to capital gains tax.

Returns on long-duration debt funds such as Nivesh Lakshya for the last one and three years do not look appealing. But past returns are a poor guide to investing in this category, as short-term returns are highly sensitive to rate moves. Interest rate increases lead to short-term NAV losses in debt funds. Funds with extra-long durations of 20-25 years such as Nivesh Lakshya tend to suffer the highest NAV erosion during rising rates.

The 10-year gilt yield, after falling from 8 per cent in September 2018 to about 5.8 per cent in July 2020, has recovered to 7.4 per cent now. This has led to Nivesh Lakshya delivering modest returns of 4.3 per cent return in the last one year and 6 per cent over three years. Investors in fund have suffered a bumpy ride too. In its worst quarter in March-June 2022, the fund lost 4.4 per cent of its NAV and in its worst year (June 2021 to June 2022), it lost 2.9 per cent. But NAV losses and gains from rate movements impact returns only in the short run. Over holding periods of eight years or more, which are recommended for this fund, interest inflows will smooth out returns delivering CAGRs close to its YTM.

This fund is not suitable for fixed income investors who wish to avoid volatility or those with investing horizons of less than eight years.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.