When considering a term insurance, the purchase decision generally centres on the size of the cover, the add-ons to spruce up the offering and the right insurance/platform to buy the product from. Prospective policyholders also ponder over return of premium option or whole life term insurance (coverage up to 99 years), but these options may likely dilute the benefits of term insurance. But for a niche audience, duration of cover, especially a short term cover, can sometimes be a relevant consideration compared to the standard template (cover up to 65 years of age).

There are a host of insurers that include coverage for five years at a stretch in their term insurance policies and Aditya Birla’s Anmol Suraksha Kawach is the latest offering in the segment. The term insurance product, specifically designed for short term, is available for two years minimum to five years maximum coverage, for people aged between 25 and 55 years. The term cover ranges from ₹50 lakh to ₹2 crore in steps of ₹25 lakh for Anmol Suraksha Kawach. The product is priced at ₹8,300 per annum for ₹1 crore policy.

We evaluate a few possible circumstances under which a short term cover can be useful and the pricing difference compared to a regular cover.

Use-case scenarios

The normal term cover is expected to replace the earnings potential of an individual in case of an unfortunate event so as to cover family obligations and/or personal liabilities. Hence the cover is chosen to extend up to 65 years for a working professional.

For policyholders nearing retirementin the next five years, with no life cover or a sub-optimal one, and with important milestones yet to be met, a short term cover may be useful. In the natural progression of personal income, one may end up accumulating 80 per cent of personal wealth in the last five years before retirement. And if the life cover taken very early in life is deemed insufficient to that stage of earnings, a short term cover can be considered, equivalent to value of the pending life goals.

Dependants are the main reason why term insurance is considered. Policyholders with an insufficient life cover while financing the crucial stage of a child’s education, most likely overseas or higher studies, should consider this short term cover. The dependant’s needs may have been supported without a comprehensive safety net until then, but at such a juncture a term insurance to protect the dependant’s quality of life is crucial. At the other end of the dependant spectrum, dependants over the age of 80, supported by a single income of the policyholder, may consider a short term insurance.

An unhedged liability which is outstanding and due to be cleared in the next few years can be a situation when short term insurance can be useful. A home loan is a good example. Home loan tenures can range up to 20 years, but most loans are cleared within eight years. For an outstanding home loan that is expected to be cleared in the next few years from personal income, a short term insurance equivalent to the loan value can be a good short-term hedge.

A long term life cover can be discontinued if added as an extra layer of protection, as and when risks de-escalate. But by choosing a short term cover, the costs would be lower, and is the main reason for considering a short-term term insurance.

Pricing differences

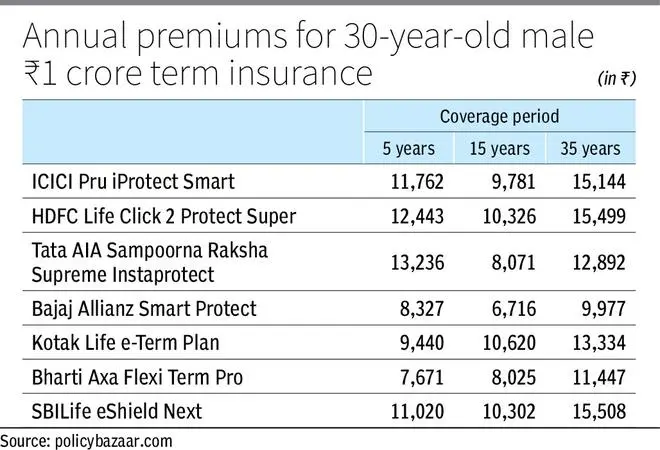

Most insurers offer term insurance starting from five years. For comparison, we have considered a male, a 30-year-old non-smoker salaried graduate in a metro city, for a ₹1-crore term insurance. The comparison yields some interesting insights.

The annual premium for a five-year term insurance with coverage up to the age of 35 years (in a range of ₹7,671 to ₹13,236) is, on an average, 25 per cent cheaper when compared to annual premium of a 35-year term policy with coverage up to 65 years (in a range of ₹9,977 to ₹15,508), all else remaining constant. But at the same time, a 15-year term insurance with coverage up to 45 years (in a range of ₹6,716 to ₹10,620) is average 10 per cent cheaper compared to even the five-year annual premium cost.

Overall, on an annual premium cost basis, there are savings offered by choosing a lower tenure of coverage. The features, including waiver of premium on accident, terminal illness or add-ons, are nearly identical across coverage tenures. But the cost of add-ons for critical illness, extra payout of accidental death and others, might increase as coverage tenure increases.

For policyholders with a requirement of limited period of protection, a short term insurance might be useful. Also, a shorter term insurance may include easier underwriting standards encompassing medical records, income profile and others compared to a longer term insurance period. But this has to be confirmed at the issuer level. For instance Anmol Suraksha, follows “No-Prick” issuance process where medical evaluation is done digitally via Video call for all standard cases.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.